October 14, 2024

October 2024 Commentary Blueprint Chesapeake Multi-Asset Trend ETF

Home » Strategies » Exchange Traded Funds » Blueprint Chesapeake Multi-Asset Trend » TFPN Commentary

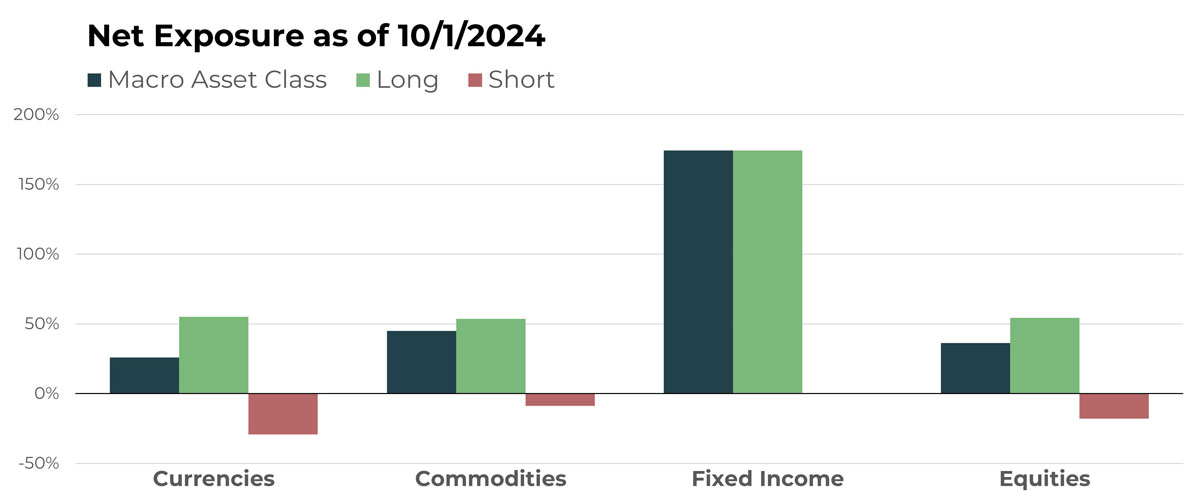

Portfolio Exposure At A Glance

Notable Holdings By Macro Asset Class

| CURRENCIES | |

|---|---|

| Name | Long/Short |

| Australian Dollar/Canadian Dollar | Long |

| Swiss Franc/Norwegian Kroner | Short |

| iShares Ethereum Trust ETF | Long |

| Danish Krone/U.S. Dollar | Long |

| Euro/U.S. Dollar | Long |

| COMMODITIES | |

|---|---|

| Name | Long/Short |

| Gold Future | Long |

| Lead Future | Short |

| Live Cattle Future | Long |

| Tin Future | Long |

| Cocoa Future | Long |

| FIXED INCOME | |

|---|---|

| Name | Long/Short |

| U.S. 10-Year Future | Long |

| SPDR Bloomberg High Yield Bond ETF | Long |

| U.S. 3-Year Note Future | Long |

| iShares Short-Term National Muni Bond ETF | Long |

| Canada 10-Year Bond Future | Long |

| EQUITIES | |

|---|---|

| Name | Long/Short |

| Corteva, Inc. | Long |

| Volkswagen AG | Short |

| Koninklijke Vopak N.V. | Long |

| Pilgrims Pride Corp | Long |

| UFP Technologies, Inc. | Long |

ETF holdings and macro asset class allocations are subject to change.

Currencies

Overview

After a flurry of currency-related activity in recent months, driven by the temporary unwinding of the Japanese Yen “carry trade,” the currency portfolio has somewhat stabilized. Despite the volatility, trend-based exposures did not change materially. The Australian/Canadian Dollar cross rate remains a key long position, continuing its positive trend with a gain of more than 5% for the year. Additionally, European currencies have taken on more prominence, with the U.S. Dollar weakening against both the Danish Krone and Euro, positioning TFPN to capitalize on these evolving opportunities.

Drivers

The Federal Reserve’s aggressive interest rate cuts in September have created a window for the U.S. Dollar to weaken against other global currencies. This can occur even against currencies that may also be depreciating due to their own central bank easing measures, particularly when those measures are less aggressive than those of the Fed. A similar effect is expected from central banks that tend to follow the U.S. closely, such as in Canada. These dynamics present a unique set of opportunities within the currency segment, offering multiple ways to express positions. TFPN’s strategy is designed to capitalize on these opportunities in a way we believe is distinct.

Commodities

Overview

While individual long commodity positions have been common in the portfolio, October marks the largest net long allocation since TFPN’s inception. For the first time, long positions significantly outweigh shorts, positioning commodities as the second most influential asset class behind fixed income.

Gold is the most notable long position in this segment, continuing its longer-term upward trend. Live cattle futures are also noteworthy, having briefly been a short position before resuming their uptrend. Finally, we should mention cocoa futures, which continues as a notable long.

Drivers

Last month we noted the potential for falling interest rates to boost commodity prices. So far, this appears to be playing out, with commodities moving from a relatively hedged (longs vs. shorts) stance to a heavily long allocation. While markets don’t always align with expectations, the combination of a potential soft landing in the U.S. economy and easing monetary policy seems to have sparked positive trends across the commodity sector.

Fixed Income

Overview

Last month’s commentary highlighted that net long fixed income had become the portfolio’s largest allocation, anticipating the next rate-cutting cycle (i.e., price predicts news). In addition to the directional shift, there was a change in magnitude, with duration extending further along the scale and increasing interest rate sensitivity. That transition is now fully underway, with no material short exposure in TFPN’s fixed income positions.

Notable holdings include U.S. Treasuries, along with high yield, municipals, and international Treasuries.

Drivers

As anticipated, the Fed’s 50 basis point rate cut was the primary driver of the fixed income portfolio for September, and this focus continues into October. Attention now shifts to what comes next: Will we see one or two more cuts as 2024 concludes? Will they match September’s size or be smaller? Recent economic data has set the stage for further cuts, and market sentiment is aligned with this outlook. If that proves accurate, the portfolio is well-positioned to benefit, in our view.

Equities

Overview

Net long equity exposure will decrease slightly as Q4 begins, dropping to third among the most-impactful asset classes, behind fixed income and commodities.

Two agriculture-related enterprises are notable long holdings: Corteva and Pilgrims Pride Corp. Corteva is outperforming the broader market with a year-to-date return of around 30%, while Pilgrims Pride is significantly ahead, with a return of about 80%.

Another commodity-related company, Dutch oil storage and shipping firm Koninklijke Vopak NV, also stands out with a year-to-date return that is more than double that of the market at large.

UFP Technologies remains a notable holding in October, having hit another all-time high in September before experiencing a retracement. Despite the pullback, it is still up more than 80% in 2024.

The only notable short is Volkswagen. The German automaker hit new multi-year lows in September, followed by cuts to its sales and profit forecasts. The downtrend, which began as early as 2021, had long signaled these outcomes.

Drivers

With a contentious U.S. election cycle nearing its culmination, investors should not be surprised to see an uptick in volatility as markets price in the odds of different outcomes. Escalating tensions in the Middle East between Israel and Iran may also heighten anxiety for some market participants. Despite these risks, the environment for equities remains largely favorable. Coupled with the easing of monetary policy, key tailwinds remain in place.

One could argue that these tailwinds are particularly strong for many of the notable long positions in the portfolio.

As long commodity exposure has grown in TFPN, so has the influence of commodity-related equities. This underscores a unique attribute associated with TFPN’s broad portfolio — not only are allocations spread across asset classes, but the individual equity positions can also benefit from prevailing trends.

Portfolio Managers’ Note

In early September, Co-Founder of AQR Capital Management Cliff Asness published “In Praise of High-Volatility Alternatives.” If you haven’t read it, we highly recommend checking it out. His main point is to highlight the tremendous long-term benefits of incorporating assets into a portfolio that don’t move in sync with equities. He even challenges investors to consider increasingly volatile (yes, volatile) alternatives, and he provides compelling evidence for why this approach can work.

One of the biggest challenges Asness notes — and something we have repeatedly observed — is that both investors and financial advisors often focus on individual line items rather than the overall portfolio. This, combined with an inherent bias toward equities, creates an environment where optimal long-term returns may be sacrificed before they even have a chance to be realized. Certainly, many advisors incorporate other assets like fixed income, but any asset that underperforms stocks for a meaningful period is often removed — even if it is performing exactly as intended.

For us, TFPN and similar alternatives serve an invaluable and irreplaceable function. Their most important role is to be a non-correlated, non-dependent tool designed to benefit from outliers, which typically have a negative impact on traditional assets. In this regard, we’ve been very pleased with the performance of this asset class and wouldn’t change a thing. The only constraint we face — similar to that of other alt managers — is the hesitancy among retail investors and their financial advisors to maintain exposure to these valuable instruments.

Fortunately, there is growing recognition of the value of these types of assets. We continue to seek out true believers while expanding our audience by sharing powerful insights, from Asness and others. We also understand that what we offer may not be for everyone. With that said, we welcome the challenge and appreciate the opportunity for improvement that comes from defending our beliefs and investing processes against the status quo. We also understand that when everyone moves to one side of the boat, things can get precarious. One of the reasons we are confident in our edge is that there seems to always be skeptics.

Let's Talk

If you’d like to learn more about TFPN, a next-generation liquid alternative