September 16, 2024

September 2024 Commentary Blueprint Chesapeake Multi-Asset Trend ETF

Home » Strategies » Exchange Traded Funds » Blueprint Chesapeake Multi-Asset Trend » TFPN Commentary

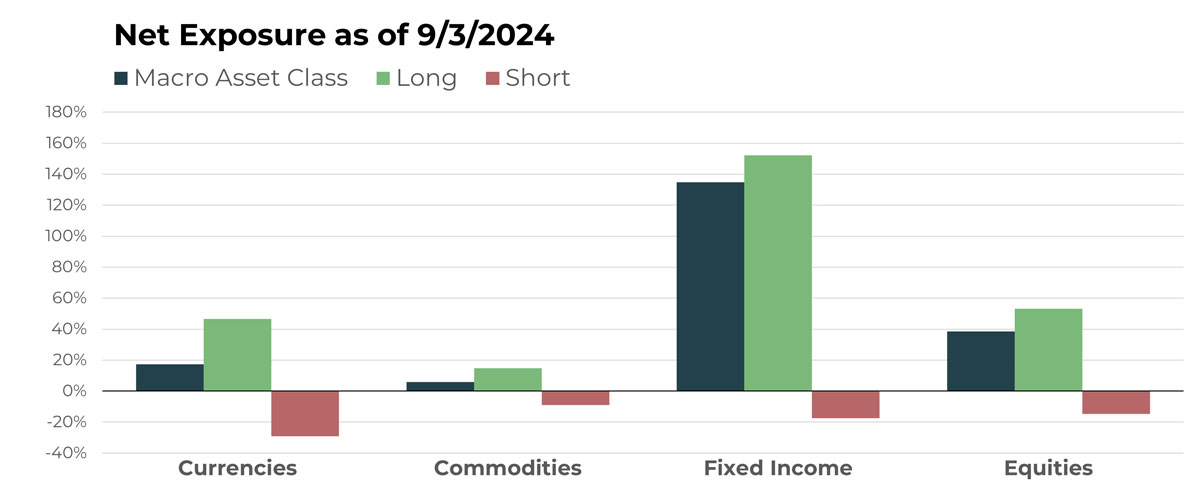

Portfolio Exposure At A Glance

Notable Holdings By Macro Asset Class

| CURRENCIES | |

|---|---|

| Name | Long/Short |

| Swiss Franc/Japanese Yen | Long |

| Indian Rupee/U.S. Dollar | Short |

| British Pound/Swiss Franc | Long |

| Philippine Pesos/U.S. Dollar | Short |

| Polish Zloty/Euro | Long |

| COMMODITIES | |

|---|---|

| Name | Long/Short |

| Frozen Orange Juice Future | Long |

| Cotton Future | Short |

| Gold Future | Long |

| Lean Hogs Future | Short |

| Cocoa Future | Long |

| FIXED INCOME | |

|---|---|

| Name | Long/Short |

| U.S. 10 Year Future | Short |

| Invesco Senior Loan ETF | Long |

| U.S. 3-Year Note Future | Short |

| iShares 0-5 Year High Yield Corp Bond ETF | Long |

| Japan 10-Year Bond Future | Short |

| EQUITIES | |

|---|---|

| Name | Long/Short |

| Carpenter Technology Corporation | Long |

| ConocoPhillips | Short |

| Ingredion Inc | Long |

| Lululemon Athletica Inc | Short |

| AZZ Inc | Long |

ETF holdings and macro asset class allocations are subject to change.

Currencies

Overview

It seems currency markets often go unnoticed in the financial advisory world until something major happens that impacts equity and bond markets. In August, the Yen’s hard reversal from its long-term trend was one such event. While we aren’t calling an end to the Yen’s downtrend or the carry trade, this high-volatility counter-trend move significantly affected global stocks and bonds. As long-term trend followers, this counter-trend rally did not materially impact our net exposures during the month, although it did impact the profit and loss of our short Yen position.

Beyond TFPN’s short Yen exposure, a key theme has been shorting emerging market currencies against the U.S. Dollar, with both the Philippine Peso and Indian Rupee trending lower.

The Swiss Franc has also played a prominent role, appearing on both the long side (versus the Japanese Yen) and the short side (versus the British Pound).

Another notable holding is the uptrend in the Polish Zloty versus the Euro. Despite Poland being a European Union member since 2004, as well as having one of its main political parties advocating for Euro adoption since 2012, it has yet to achieve the majority support needed to join the Eurozone.

Drivers

As mentioned above, the Japanese Yen grabbed headlines in July and August with its sharp reversal. The Japanese Yen has generally been able to hold those short-term gains versus other currencies, such as the U.S. Dollar.

Elsewhere, continued declines in inflation readings year over year are making the case for central banks to loosen monetary policy. The big question has changed – no longer IF or WHEN, but rather HOW MUCH – in terms of cuts. The policymakers that move fastest and most significantly could be the next drivers of trends within their respective currencies.

Commodities

Overview

Net exposure to commodities is virtually unchanged from August to September, remaining slightly tilted to the long side.

Cocoa future (September contract) surged in the first few months of the year, retraced, mostly traded sideways, then resumed an uptrend to climb almost 20% in August.

Orange juice futures also increased significantly in August, up 18%, and began September in a similar fashion.

Gold is another prominent long that continues to trend upward.

On the short side, the most notable position is cotton. While retracing in August from its declining trend, it has still fallen in three of the last four months.

Drivers

It is natural to assume a change in interest rate regimes from hiking to cutting would be a catalyst for commodity trends, and that may very well end up being the case. However, for the time being, the trends that have been in place (or not) appear to be unaffected by the potential inflection in interest rates. The notable trends described above have been in place for some time and have yet to be materially impacted. The contrasting effects of easy money, with the risk of declining demand due to recession, appear to have much of the commodity complex at a stalemate. While that is the trend, TFPN will focus on the primary movers and remain patient until trends emerge.

Fixed Income

Overview

Net long fixed income will now take over as the largest allocation within the portfolio, as consensus builds towards the next rate-cutting cycle. Duration exposure continues to be tilted short to intermediate, but this may change if trends continue building. Interestingly, this doesn’t mean that all increases in bond prices will necessarily help returns for the ETF. For example, one must remember that longer-duration bonds have been in long-term downtrends for an extended period – which is why the portfolio continues to hold some short positions in these bonds.

Drivers

For now, it appears that economic data is a key driver for fixed income. Inflation is still occurring, but at a rate more in line with long-term expectations for policymakers. This would seem to pave the way for interest rate cuts. On the other hand, employment and growth are still strong, which dampens the urgency a bit. The market is clearly betting on multiple and perhaps even extreme cuts to end 2024. While this seems unlikely to us, in the end it doesn’t matter, as we will follow our rules regardless. A failure for the Fed to live up to expectations could mean a retracement in the current upward rebound in bond prices. Cuts likely wouldn’t do much for prices, given where expectations are already set, but the surrounding rhetoric could be very important to drive prices higher.

Equities

Overview

Starting in September, equities will take a backseat (or perhaps slide into the passenger seat) to bonds in terms of most significant allocations. However, the portfolio remains rightfully net long given the preponderance of uptrends. Further, short exposure has not materially increased, even as volatility spiked in mid- to early-August. Rather, long positions have decreased as some segments that led overall in 2024, such as tech and growth, have been replaced in the very near term by value.

Notable long positions include:

- Carpenter Technology (CRS), which has returned almost 100% since late March through the first week of September, despite a sharp drop to open the month

- Ingredion (INGR), which has accelerated its uptrend in recent months after slowly climbing higher

Among notable shorts are:

- Lululemon (LULU), which has fallen five of the last six months

- ConocoPhillips (COP)

Drivers

Conditions continue to be mostly favorable for equities, as evidenced by the number of uptrends. This portion of the portfolio has positively attributed to performance in 2024 for TFPN, but as with any asset class, returns will ebb and flow in the very short term. The pivot from hawkish to dovish in monetary policy and the upcoming U.S. election will likely keep equity markets on edge as we finish out 2024. However, the fundamentals of trend following – cutting losses, riding winners, ample diversification, etc. – are always poised, in our opinion, to navigate these circumstances well.

Portfolio Managers’ Note

Generally, we almost always view the world – or attempt to anyway – through the lens of the financial advisor. We aim to help advisors improve the odds that they and their clients will reach their financial goals (and by extension, their life goals as well).

Most of the time, but not always, if an advisor has a strong relationship with their client, a firm grasp on how to execute a plan developed in collaboration with that client, and is able to put themselves in their clients’ shoes in order to provide some coaching along the way, success is attainable.

We take a similar approach when evaluating TFPN because we think about the ETF in the context of how an advisor would – or ideally should – view its role in the context of a larger client portfolio.

Last month we discussed the impact of market inflection points and how they can challenge trend-following strategies like the one used by TFPN in the short term. As asset managers with decades of market experience, we concluded that while these periods can be painful, they are an inevitable part of targeting long-term success over short-term gains. We believe each component of this long-term strategy is essential to the overall process.

The good news is that, after tracking market performance across various asset types for decades, we know that inflection points and their instability don’t last forever. Eventually trends either build or continue. Perhaps most importantly, the non-correlation inherent in strategies like the one used by TFPN means that when trend-following strategies face challenges, other assets in an advisor’s portfolio often perform well. This was evident in August, as equities and bonds generally performed well.

Looking ahead, it wouldn’t be surprising to see volatility remain high due to seasonal factors that often put pressure on equities, as well as potential rate cuts and the upcoming U.S. election. We frequently highlight how the market acts as a discounting machine, though it’s impossible to know when sentiment will shift from the current news cycle to what lies ahead.

As always, we’re grateful to have a systematic investing process that provides financial advisors with a tool that, in our view, will ultimately align with the lasting trends each asset establishes.

Let's Talk

If you’d like to learn more about TFPN, a next-generation liquid alternative