May 16, 2024

May 2024 Commentary Blueprint Chesapeake Multi-Asset Trend ETF

Home » Strategies » Exchange Traded Funds » Blueprint Chesapeake Multi-Asset Trend » TFPN Commentary

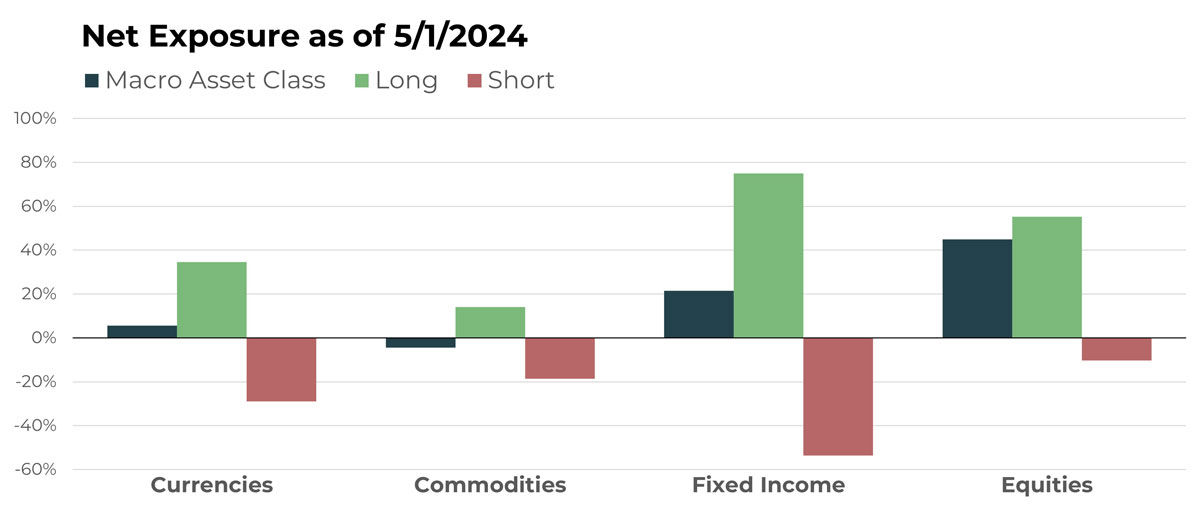

Portfolio Exposure At A Glance

Notable Holdings By Macro Asset Class

| CURRENCIES | |

|---|---|

| Name | Long/Short |

| Swedish Krona/Euro | Long |

| Korean Won/U.S. Dollar | Long |

| Chinese Renminbi/Japanese Yen | Long |

| Brazil Real/U.S. Dollar | Short |

| Swiss Franc/Canadian Dollar | Short |

| COMMODITIES | |

|---|---|

| Name | Long/Short |

| Lumber Future | Short |

| Gold Future | Long |

| Lead Future | Short |

| Aluminum Future | Long |

| Cocoa Future | Long |

| FIXED INCOME | |

|---|---|

| Name | Long/Short |

| U.S. 2-Year Note Future | Short |

| Invesco Senior Loan ETF | Long |

| U.S. 10-Year Note Future | Short |

| Canadian 10-Year Bond Future | Short |

| Japan 10-Year Bond Future | Long |

| EQUITIES | |

|---|---|

| Name | Long/Short |

| Silgan Holdings Inc | Long |

| Starbucks Corp | Short |

| UFP Technologies Inc | Long |

| Adobe Inc | Short |

| Verisk Analytics, Inc. | Short |

ETF holdings and macro asset class allocations are subject to change.

Currencies

Overview

Among the four major asset classes TFPN utilizes in its portfolio – currencies, commodities, fixed income, and equities – currencies are unique in varied possibilities for expressing diversified exposures. We believe TFPN’s ability to express currency trends in a wide variety of ways leads to exposure to trends that can provide meaningful non-correlation for the TFPN portfolio, as well as the remainder of an investor’s portfolio overall.

A quick glance at the notable holdings above illustrates this point well, in our view. Of the five listed above, three are shorts, two are longs, and all five are a combination of differentiated currency pairs. In April, the Korean Won/U.S. Dollar trade was the most profitable of those listed above.

Drivers

With so many ways to display trends in TFPN’s currency portfolio, it can be difficult to attribute performance to one or even a handful of drivers. Clearly, the global view on inflation and the impact on interest rates is currently the primary focus among global central banks and investors. The generally bullish view of the U.S. economy has kept the dollar strong relative to most international currencies, but U.S. Federal Reserve comments continue to keep in play the prospect of interest rate cuts this year. The tug of war between investor sentiment and Fed wordsmithing has led to short-term increases in volatility and choppy conditions.

Commodities

Overview

After flipping from slightly net short to net long commodities heading into April, TFPN will return to being net short in May.

Prominent downtrends include lead and lumber, the latter of which fell more than 14% in April (May futures contract).

Despite the flip back to being net short, there are still plenty of impressive uptrends in place, resulting in significant long positions as well. Gold (May contract) followed up its near 8% increase in March by rising another 3.9% in April. Another metal that has been doing well is aluminum, which increased more than 12% in April (June contract) after a 5.4% return in March. Last but not least among notable longs is cocoa, which has been a fixture of this year’s updates. The staple managed to eke out another small increase of 3.8% in April, following up its historic Q1 return.

Drivers

Stable global economies, sticky inflation, and war historically result in strong demand for metals – and that continues to be the case in 2024. Gold, aluminum, and copper (to name a few) have enjoyed positive trends, and TFPN has capitalized accordingly. Cocoa has also benefitted from these ingredients, with other factors restricting supply further fueling its price surge.

That said, the prospect of a weaker global economy and rate cuts has and will continue to erode positive trends in the commodity space. Commodities, perhaps even more than other assets, can be very cyclical. After a strong run during these inflationary times, it is inevitable that persistent downtrends will eventually occur.

The beauty of TFPN, in our opinion, is its ability to adapt to an endless array of possibilities, whether they fit the historical norms or deviate from them.

Fixed Income

Overview

Another month, another reduction in TFPN’s net long stance toward fixed income.

Bullish trends that emerged in late 2023 in response to (over)confidence in upcoming interest rate cuts have continued to fade, with longer duration instruments beginning to move back into downtrend status. Domestic short positions, from the U.S. 10-Year Treasury future to the U.S. 2-Year Treasury future, are joined by international shorts, such as the Canadian 10-Year future.

Notable long positions include the Invesco Senior Loan ETF and Japanese 10-Year bonds.

Drivers

Looking at the TFPN fixed income portfolio syncs up well, in our opinion, with the current sentiment around interest rates. It seems the consensus belief is that global central banks will cut rates, which is of course bullish for bond prices. That said, the confidence in the exact timing has fallen precipitously. In times like these, a hedged stance with the ability to adapt quickly seems like an appropriate one. With strong trends elsewhere in the portfolio, it is best to let those take center stage.

Equities

Overview

For the first time since TFPN’s inception, the largest net exposure is now equities.

As will almost always be the case, the portfolio also continues to hold short positions. For the month of May, the most prominent of those are Starbucks, which has positively attributed to the portfolio by opening the month down double digits, after falling more than 3% in both March and April. Adobe and Verisk Analytics are also meaningful shorts that have experienced significant recent declines, though both opened strongly in May.

Noteworthy long positions for the portfolio include Silgan Holdings and UFP Technologies, both of which declined in April despite entrench uptrends that remain intact. Both also opened positively in May.

Drivers

Strong earnings in April and just enough economic data to keep the prospect of rate cuts intact have been the recipe to keep equities trending higher and TFPN’s long equity book expanding.

At a high level, volatility continues to be low, which is almost always favorable for positive trends in stocks. The growth segment remains the leader, but all segments have done relatively well. At this point, it is our belief that the market has priced in the idea of delayed rate cuts. In our opinion, this means that renewed confidence in the timing of these cuts will likely drive further increases in stock prices. However, it must be repeated that risks are ever present, and things can change quickly.

The presence of hedging shorts supports our steadfastness in our belief in TFPN as an essential component for financial advisors and their clients.

Portfolio Managers’ Note

Last month we summed up TFPN’s portfolio with the following:

- Meaningfully exposed to equities

- Hedged with some prominent short positions in large-cap stocks, which is intended to offset the portfolio’s otherwise significant long exposure

- Containing material long fixed income exposure (i.e., short interest rates)

- Broadly diversified in commodity and currency allocations, with a mix of longs and shorts

With the exception of bullet three, which is less material for May, this summarization is still appropriate.

One of the things we appreciate about being trend followers is that there is rarely a moment where our portfolio feels out of step with what is happening in real time. Even during moments where it does seem vulnerable, it generally does not persist due to the array of timeframes being used.

For these reasons, we do not fear change or outliers. Rather, extreme, diverging events have a way of generally benefiting our style of asset management, in our experience. The discipline required to live out this philosophy is just difficult enough that there is little risk of the herd embracing trend following. Also, people’s seeming need to make predictions is antithetical to rules-based, systematic trend following. Both of these factors are good for us because it means there will almost always be a need for what we are providing, and we believe firmly that the same edge trend followers have enjoyed historically will endure.

Let's Talk

If you’d like to learn more about TFPN, a next-generation liquid alternative