April 16, 2024

April 2024 Commentary Blueprint Chesapeake Multi-Asset Trend ETF

Home » Strategies » Exchange Traded Funds » Blueprint Chesapeake Multi-Asset Trend » TFPN Commentary

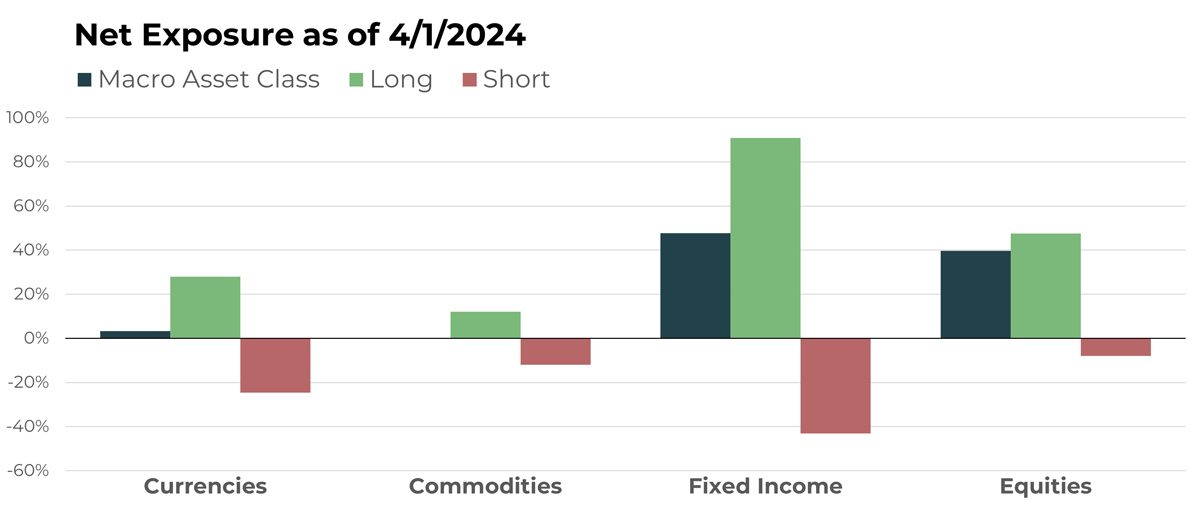

Portfolio Exposure At A Glance

Notable Holdings By Macro Asset Class

| CURRENCIES | |

|---|---|

| Name | Long/Short |

| Swedish Krona/Euro | Short |

| Singapore Dollar/U.S. Dollar | Long |

| Euro/Swiss Franc | Long |

| iShares Bitcoin Trust | Long |

| New Zealand Dollar/Australian Dollar | Short |

| COMMODITIES | |

|---|---|

| Name | Long/Short |

| Wheat Future | Short |

| Gold Future | Long |

| Soybean Future | Short |

| Copper Future | Long |

| Cocoa Future | Long |

| FIXED INCOME | |

|---|---|

| Name | Long/Short |

| Canadian 10-Year Bond Future | Short |

| iShares National Muni Bond ETF | Long |

| U.S. 10-Year Note Future | Short |

| Vanguard Short-Term Corporate Bond ETF | Long |

| Japan 10-Year Bond Future | Long |

| EQUITIES | |

|---|---|

| Name | Long/Short |

| elf Beauty Inc | Long |

| Hershey Co | Short |

| Commercial Metals Company | Long |

| MicroStrategy Inc | Long |

| Hormel Foods Corp | Short |

ETF holdings and macro asset class allocations are subject to change.

Currencies

Overview

As we move into the second quarter, TFPN’s currency portfolio continues to contain a vast array of long and short positions, including cross-rate exposures and digital currencies.

Perhaps the most noteworthy currency trend continues to be the long exposure to Bitcoin, via futures and the iShares Bitcoin Trust (IBIT), which followed its nearly 46% return in February by increasing another 14% in March. As we mentioned last month, this performance is indicative of the outlier trends our strategy aims to identify. It’s also an example of how TFPN seeks to offer financial advisors access to unique instruments for their client portfolios, ones that might otherwise be outside their comfort zones without a systematic investing approach.

Other notable trends include Swedish Krona versus Euro cross rate (short), the Euro versus Swiss Franc (long), and the New Zealand versus Australian Dollar (short). The latter two especially contributed to the portfolio’s overall positive performance in March.

Drivers

Bitcoin ascended to new all-time highs in March as investors continued to rush back in from the “crypto winter.” The favorable environment for technology stocks in general has also provided support.

The Swiss Franc has weakened, in part from an unexpectedly dovish stance taken by the Swiss National Bank (SNB). The SNB recently cut rates in a surprise move relative to expectations. This followed news that inflation continues to ease in global markets, which remains the primary driver for currencies in TFPN’s portfolio.

Commodities

Overview

Entering the second quarter, TFPN has shifted from being net short commodities to slightly net long.

While grains like wheat and soybeans continue to be entrenched in downtrends, resulting in short positions, metals like gold and copper are now generating significant uptrends.

The April gold futures contract rose almost 8% in March while the same contract in copper futures rose 4.5%.

No commodity position is more newsworthy, in our view, than cocoa. This outlier trend, after returning almost 15% in January and 35% in February, jumped another 50% in March (May contract). This remarkable climb has left it up about 100% year-to-date entering April.

Drivers

Continuing economic strength that has resulted in robust demand is helping support commodity uptrends. In addition, escalating tensions in the Middle East and the continued war in eastern Europe is likely influencing gold’s increase. Likewise, supply and demand considerations – particularly out of West Africa – are strongly affecting cocoa’s parabolic rise.

However, it is our view that relying solely on fundamental forecasts and factors will seldom, if ever, enable investors to consistently capitalize on trends that appear incomprehensible. The recent trends demonstrated by cocoa is an example.

Fixed Income

Overview

After rotating from net short to net long fixed income at the end of 2023, the portfolio is continuing a recent trend toward a more neutral stance, with long exposures decreasing. Long fixed income positions remain the largest segment of the overall portfolio, but total exposure is about half what it was at its peak earlier in the year. Investor sentiment anticipating a decrease in rates and subsequent increase in bond prices remains largely intact, but it has waned as the global pivot from hawkish to dovish has been delayed.

Drivers

Wait and see – that is the current motto of bond markets it appears. Rate cuts continue to be perceived as the next move, which was further bolstered with the aforementioned cuts by the SNB. Even in the U.S., where inflation remains arguably strongest among major economies, Fed Chairman Jerome Powell recently reiterated the expectation of rate cuts in 2024. However, the market seems to have lost a bit of its confidence as probabilities for cuts in the next Fed meeting have decreased.

Equities

Overview

The equity portion of the portfolio has continued to climb, now holding nearly the same net long exposure level as fixed income.

Elf Beauty Inc (ELF) finally experienced a down month in March after 22%, 10.5%, and 31% gains in December, January, and February. With ELF taking a breather, Microstrategy (MSTR), another prominent long position, picked up the slack by increasing a staggering 67% in March.

While long positions outweigh the shorts in the portfolio, there are still notable positions acting as hedges. Hershey (HSY) and Hormel (HRL) are notable examples. In March, Hormel experienced a decline of more than 1% amidst generally increasing equity prices.

Drivers

U.S. equities ended March virtually at an all-time high, showing the type of bull market behavior that trend following is designed to capture. The portfolio’s basket of single stocks, as opposed to indexes, has allowed it to capture outlier uptrends while keeping valuable short positions in place to hedge against sudden downturns. The goal of this combination is to provide a robust risk-adjusted return, making TFPN a powerful stand alone or diversifying segment in an investor’s portfolio.

Portfolio Managers’ Note

TFPN’s goal is to offer returns that are not reliant on positive equity market performance. We consider the first quarter of 2024 to be an excellent example of how the ETF can be an important component of a modern portfolio, potentially reducing the risk of painful drag often seen with traditional equity portfolios and other alternative strategies.

As we move further into the year, TFPN’s portfolio can best be summed up as:

- Meaningfully exposed to equities

- Hedged with some prominent short positions in large-cap stocks, which is intended to offset the portfolio’s otherwise significant long exposure

- Containing material long fixed income exposure (i.e., short interest rates)

- Broadly diversified in commodity and currency allocations, with a mix of longs and shorts

Let's Talk

If you’d like to learn more about TFPN, a next-generation liquid alternative