March 18, 2024

March 2024 Commentary Blueprint Chesapeake Multi-Asset Trend ETF

Home » Strategies » Exchange Traded Funds » Blueprint Chesapeake Multi-Asset Trend » TFPN Commentary

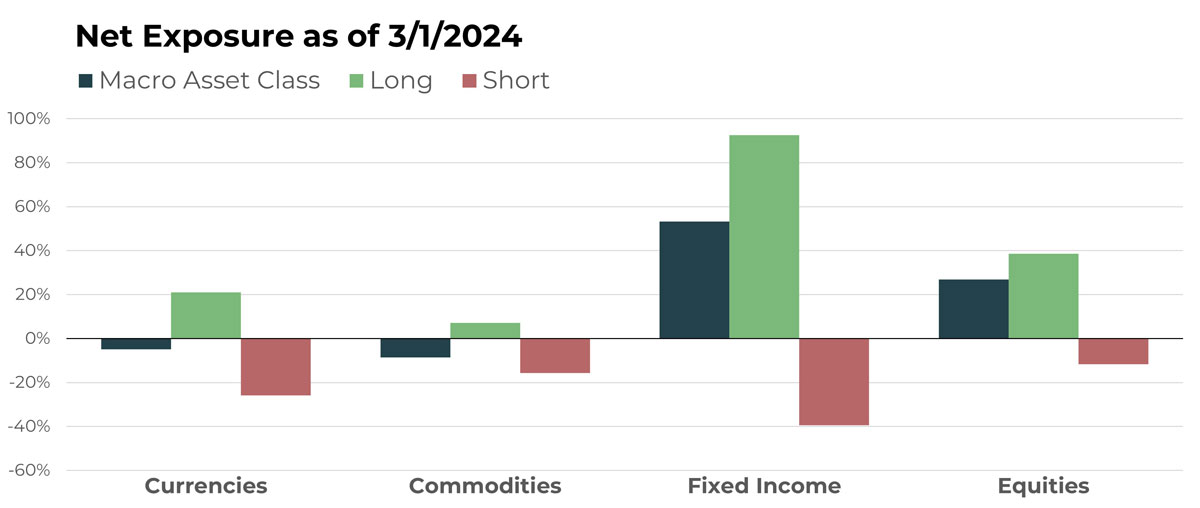

Portfolio Exposure At A Glance

Notable Holdings By Macro Asset Class

| CURRENCIES | |

|---|---|

| Name | Long/Short |

| Swedish Krona/Euro | Short |

| Canadian Dollar/Japanese Yen | Long |

| New Zealand Dollar/Australian Dollar | Long |

| iShares Bitcoin Trust | Long |

| Czech Krona/U.S. Dollar | Short |

| COMMODITIES | |

|---|---|

| Name | Long/Short |

| Sunflower Seed Future | Short |

| Frozen Orange Juice Future | Long |

| Cattle Future | Short |

| Rubber Future | Long |

| Cocoa Future | Long |

| FIXED INCOME | |

|---|---|

| Name | Long/Short |

| U.S. 5-Year Note Future | Short |

| iShares Short-Term National Muni Bond ETF | Long |

| U.S. 10-Year Note Future | Short |

| iShares 0-5 Year TIPS Bond ETF | Long |

| Japan 10-Year Bond Future | Long |

| EQUITIES | |

|---|---|

| Name | Long/Short |

| elf Beauty Inc | Long |

| PepsiCo Inc | Short |

| AZZ Inc | Long |

| UFP Technologies Inc | Long |

| Altria Group Inc | Short |

ETF holdings and macro asset class allocations are subject to change.

Currencies

Overview

TFPN’s currency portfolio showcases our dedication to diversification and the strategic avoidance of baskets or indexes when suitable. This portfolio includes cross-rate exposures and digital currencies, offering a broad spectrum of exposures and drivers.

February saw the emergence of several notable currency trends. The Canadian Dollar/Japanese Yen cross-trade continued its rising trend and reached a new high above its 2022 peak. While not as persistent, the long position in the New Zealand Dollar/Australian Dollar and a short in the Czech Koruna/U.S. Dollar also yielded positive results. The most significant currency trend was the long exposure to Bitcoin, via futures and the iShares Bitcoin Trust (IBIT), which saw nearly a 46% return in February. This performance is indicative of the outlier trends our strategy aims to identify, as well as how TFPN seeks to offer financial advisors access to unique instruments for their client portfolios, ones that might otherwise be outside their comfort zones without a systematic investing approach.

Drivers

For the U.S. Dollar, the shift toward maintaining steady interest rates over cuts has provided support. Economic data remains robust, and despite a reduction, inflation remains slightly elevated for policymakers. Bitcoin’s continued recovery from the “crypto winter” and general bullish sentiment among technology assets are key factors behind its recent surge.

Commodities

Overview

The portfolio’s net short position on commodities saw little change as we entered March. Markets for sunflower seeds and cattle, which were previously in uptrends, reversed in February and led to short positions. Conversely, long positions in orange juice and cocoa continued, supported by their sustained uptrends, with cocoa experiencing a sharp 34% increase in February, building on a 15% rise in January.

Drivers

Fundamentals can influence market sentiment, but movements in markets like orange juice and cocoa can sometimes detach from supply and demand dynamics. This underscores the importance of systematic investing and trend following, which prioritize process over emotion in decision-making and facilitate quick adjustments between market positions.

Fixed Income

Overview

In March, the fixed income portfolio saw a slight reduction in its net long exposure. Noteworthy short positions persist or have reemerged in U.S. Treasuries, while new long opportunities have arisen in inflation-protected bonds and Japanese bonds of intermediate duration. Despite the overall decrease in long exposure, the long fixed income segment remains the portfolio’s largest as the first quarter of 2024 concludes.

Drivers

Fixed income markets generally stabilized in February. The stabilization followed their decline in January, which followed their 2023 rally from lows. It is impossible to say for sure, but the markets seem to be acclimating to a new expectation for steady, instead of falling, interest rates in 2024. The fact that uptrends have held could be perceived as a positive sign for these trends to continue. Fortunately, we do not have to spend much time pondering the outcomes either way, as TFPN’s process is ready to harvest losses if need be or change course decisively if trends dictate.

Equities

Overview

The portfolio’s long equity orientation has increased for March. A notable performer last month was elf Beauty Inc (ELF), with a 31% gain in February. Other names, like AZZ Inc and UFP Technologies Inc, benefited from the broader U.S. equity rally. Short positions in PepsiCo Inc and Altria Group Inc provided a hedge against potential equity market reversals.

Drivers

February ended with U.S. equities near another all-time high. In fact, the end-of-month close was the highest on record for the S&P 500 Index and the first monthly close above 5,000. Volatility also remains low. In our view, these are important data points and support a case for being net long. The U.S. economy remains strong, with just enough data sprinkled in to point to a stabilization or reduction in inflation. TFPN’s ability to include short positions in weaker equities acts as both a hedge and chance to profit during sideways or reversal periods.

Portfolio Managers’ Note

In February, TFPN enjoyed robust returns from its equity portfolio and select commodity and currency trades.

TFPN aims to offer returns independent of positive equity market performance, which we believe makes the ETF an important component of a modern portfolio. While this noncorrelated (to equities) performance is not necessarily unique in the liquid alternative space, what we believe IS unique is how TFPN aims to reduce portfolio drag during bull markets. The portfolio’s long/short flexibility allows it to benefit during times of strong equity returns. February is a great example.

Looking ahead, TFPN continues to have a long, yet hedged, equity position. If the current trends in equity markets continue, TFPN should benefit.

The prior fixed income rally has paused, but TFPN remains net long and in a position to benefit from a cut in rates if or when that occurs. If not, positions are early enough that a reversal to short should not materially impact performance and can allow TFPN to remain nimble in responding to monetary policy.

Commodity and currency bets are spread out with a mix of newcomer positions and established trends. As central bank consensus builds, it could produce an environment for some interesting movements on which the ETF is capable of capitalizing.

Let's Talk

If you’d like to learn more about TFPN, a next-generation liquid alternative