September 19, 2023

September 2023 Commentary Blueprint Chesapeake Multi-Asset Trend ETF

Home » Strategies » Exchange Traded Funds » Blueprint Chesapeake Multi-Asset Trend » TFPN Commentary

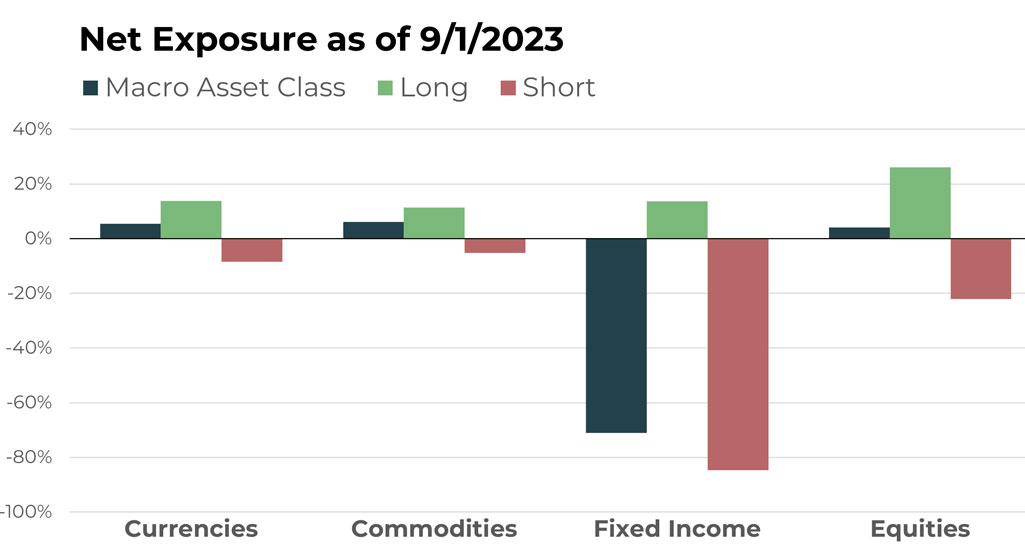

Portfolio Exposure At A Glance

Notable Holdings By Macro Asset Class

| CURRENCIES | |

|---|---|

| Name | Long/Short |

| Euro/Swiss Franc Future | Short |

| Euro/British Pound Future | Short |

| U.S. Dollar/Chinese Yuan Future | Long |

| British Pound/Swiss Franc Future | Long |

| Swiss Franc/Japanese Yen Future | Long |

| COMMODITIES | |

|---|---|

| Name | Long/Short |

| Cattle Feeder Future | Long |

| Live Cattle Future | Long |

| Cocoa Future | Long |

| London Cocoa Future | Long |

| White Sugar Future | Long |

| FIXED INCOME | |

|---|---|

| Name | Long/Short |

| 3-Month Euribor Future | Short |

| 3-Month SONIA Future | Short |

| Canadian Banker’s Acceptance Future | Short |

| 3-Month Secured Overnight Financing Rate Future | Short |

| 90-Day Australian Bank Bill Future | Short |

| EQUITIES | |

|---|---|

| Name | Long/Short |

| elf Beauty Inc | Long |

| General Dynamics Corp. | Short |

| Kraft Heinz Co. | Short |

| Hormel Foods Corp. | Short |

| WEC Energy Group Inc. | Short |

ETF holdings and macro asset class allocations are subject to change.

Currencies

Overview

The largest short positions are continuing to capitalize on the weakness of the Euro against stronger currencies, like the British Pound and the Swiss Franc.

Compared to last month, there is a slight decrease in the concentration of long positions in the U.S. Dollar; however, it remains high within the currency segment.

Swiss Franc pairs maintain significant exposure in the portfolio as well, most notably the British Pound against the Swiss Franc and the Swiss Franc against the Japanese Yen.

Drivers

Hawkish economic data and discussions about interest rate hikes in the U.S. continue to bolster the U.S. dollar against foreign currencies, such as the Chinese Yuan. Meanwhile, upward revisions to the UK’s GDP provided a boost to the British Pound, reinforcing the uptrends that have been in place since its October 2022 low.

Commodities

Overview

The top five holdings have seen little change since August, and the portfolio continues to maintain net long exposure as we enter September. Cattle futures remain the largest positions, followed by cocoa and sugar. Orange juice futures nearly joined the top five, building on a 16% return in July with a gain of just under 4% in the September 2023 contract.

Drivers

Except for a few commodities, like wheat, the sustained strength in the global consumer market has generally supported higher commodity prices over the past month. While one might expect higher interest rates to affect these assets, that has not been the case so far. In the U.S., emerging signs of a slowing employment rate, as well as rising credit usage, may impact commodity prices in the near future. For now, TFPN maintains its net long exposure in the sector.

Fixed Income

Overview

As indicated in the exposure chart above, the ETF’s most substantial sector exposure continues to be short fixed income, globally. This trend spans a variety of instruments, both domestically and internationally. Bond markets are arguably the most entrenched in downtrends across all asset categories. The latest economic reports advocating for higher and longer interest rates only add further pressure to bond prices.

Drivers

If one were to summarize the dominant themes in global financial markets during the past couple of years, inflation and central banks’ countermeasures via interest rate hikes would likely top the list.

While trends in currencies, commodities, and equities have contributed to the portfolio, fixed income stands out for its consistent direction over the entire period, making it the de facto headline trend for 2022 and 2023.

In a more traditional portfolio of stocks and bonds, expressing this kind of position is challenging. This is where we believe TFPN’s real strength lies. The lack of constraints to pursue what we believe are the best trades is what sets the ETF apart and makes it so valuable when used in traditional portfolios. The lack of constraints on the ETF’s portfolio and the ability to pursue trades across as 500 securities and financial instruments, in our view, makes TFPN a critical addition to traditional portfolios. The current positions and trends in fixed income are good illustrations of this.

Equities

Overview

Net long exposure contracted over the past month, with stocks experiencing a modest pullback in August, leading to an increase in short exposure throughout the month. Long positions continue to be diversified across a range of small- and mid-cap stocks, while short positions are mainly focused on value-oriented names.

Drivers

The gap between growth and value stocks widened in August, resuming a trend that had paused for about two months. Both segments experienced declines, but growth stock indexes generally outperformed, extending their lead for the year 2023. Although the S&P 500 Index has been performing above average — thanks largely to a few key stocks — it is worth noting that value- and dividend-oriented equity indexes are flat to negative for the year.

This landscape serves as a compelling case for the benefits of a trend-based strategy, which can systematically exploit both long and short opportunities. In typical market conditions, such trends can persist for extended periods, enabling the ETF to profit from diverging trends. However, during times of market volatility caused by an outlier event, correlations often converge, meaning all stocks may decline simultaneously. While this poses a risk to long positions, having concurrent short positions can mitigate some, if not all, of the potential downside within the sector.

Let's Talk

If you’d like to learn more about TFPN, a next-generation liquid alternative