October 17, 2023

October 2023 Commentary Blueprint Chesapeake Multi-Asset Trend ETF

Home » Strategies » Exchange Traded Funds » Blueprint Chesapeake Multi-Asset Trend » TFPN Commentary

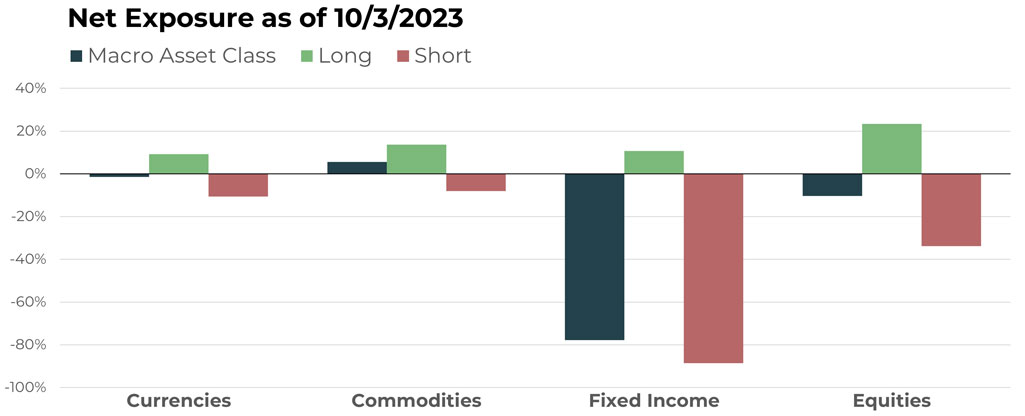

Portfolio Exposure At A Glance

Notable Holdings By Macro Asset Class

| CURRENCIES | |

|---|---|

| Name | Long/Short |

| Euro/British Pound Future | Short |

| Euro/Swiss Franc Future | Short |

| Mexican Peso Future | Long |

| U.S. Dollar/Chinese Yuan Future | Long |

| Japanese Yen Future | Short |

| COMMODITIES | |

|---|---|

| Name | Long/Short |

| Cattle Feeder Future | Long |

| Frozen Orange Juice Future | Long |

| Cocoa Future | Long |

| LME Lead Future | Long |

| Gold Future | Short |

| FIXED INCOME | |

|---|---|

| Name | Long/Short |

| 3-Month Euribor Future | Short |

| U.S. 5-Year Note Future | Short |

| U.S. 10-Year Note Future | Short |

| Australian 10-Year Bond Future | Short |

| iShares MBS ETF | Short |

| EQUITIES | |

|---|---|

| Name | Long/Short |

| elf Beauty Inc | Long |

| Hormel Foods Corp | Short |

| Target Corporation | Short |

| World Wrestling Entertainment Inc. | Long |

| The Coca-Cola Company | Short |

ETF holdings and macro asset class allocations are subject to change.

Currencies

Overview

The Japanese Yen declined further in September, a benefit to TFPN due to our short position.

Other top currency holdings displayed some counter-trend behavior. On the short side, the Euro against stronger currencies (such as the British Pound and Swiss Franc) experienced retracement in September. On the long side, the Mexican Peso and U.S. Dollar paired with the Chinese Yuan did not yield favorable returns.

Drivers

The increase in oil prices during September and its potential for negative economic consequences was a primary driver impacting currencies worldwide. As oil was increasing, the existing trends in the Euro reversed. Additionally, the U.S. Dollar’s continued march higher impacted prevailing trends in foreign currencies, such as the Mexican Peso. U.S. Dollar strength could be challenged this month by news of new currency conversions between China and South American countries, such as Brazil and Argentina, a potential continued “de-dollarization” of global currency transactions.

Commodities

Overview

After hot starts in September, top long positions in cattle feeder and cocoa futures gave back gains to close the month. That said, trends remain strong and, as a result, positions remain in place.

Unlike cattle feeder and cocoa, the November futures contract of frozen orange juice both started and ended the month strong, increasing almost 10% in September. It remains one of the largest commodity positions in the portfolio.

One interesting update is the change in positioning for gold. After opening September long, TFPN entered October with short exposure due to gold’s decline through key levels.

Drivers

Given all the press related to inflation, it is perhaps no surprise that many global commodities have benefitted in recent weeks. The interesting exception is gold, which highlights a key attribute of TFPN and its underlying strategy: even when paradoxical spreads emerge, the ETF is not constrained by the perceived historical norms of markets, but adapts to what is actually happening. The ability to adapt allows TFPN to potentially benefit from these outliers. Eventually we might expect the higher march of global interest rates to discourage further increases in commodities, but instead of making any prediction, the ETF will continue to ride the existing wave higher.

Fixed Income

Overview

Since TFPN’s inception, short allocations across a broad range of fixed income instruments have been the most prominent position in the portfolio. After September’s acceleration downward in bond prices, October will likely be no different in terms of allocations.

Recent economic reports underscore the prospect of higher rates for longer. This once again highlights the potential benefits of a trend-based investing process that eschews predictions. As an example, recall that the consensus forecast called for a series of rate CUTS by the end of 2023. As we enter the fourth quarter, the markets may be signaling otherwise.

Drivers

As trend followers, we often witness the interesting phenomenon of market participants reacting in unison (and surprise) to a news item or series of events that reinforces a prevailing trend. As we observed September’s price action in fixed income, we could not help but being left with a similar impression. Oil price increases, political chaos in the U.S Congress, and existing inflationary pressure seemed to cause a sudden consensus among investors that interest rate pauses are becoming less likely and higher rates are not out of the question.

Equities

Overview

TFPN decreased long exposure in August, and September’s equity market decreases pushed the ETF into net short territory. Overall, the equity allocation is well hedged with a mix of longs and shorts. The current long/short mix highlights a key attribute of the ETF: as a non-correlated asset, TFPN can help investors create a more optimal diversified portfolio when it is included as a meaningful allocation.

Drivers

Stocks, in our view, currently seem to be influenced by inflation, interest rates, and the ensuing prospect of a slowing global economy. Add to this the chaos in the U.S. Congress – specifically the vacating of the Speaker of the House position and its potential implications for a government shutdown later this year – and you have a recipe for increasing market volatility. The rules governing the portfolio, as well as the resulting exposure, remain objective and flexible in the face of the current fundamental landscape and the associated uncertainty.

Let's Talk

If you’d like to learn more about TFPN, a next-generation liquid alternative