November 13, 2025

November 2025 Commentary Blueprint Chesapeake Multi-Asset Trend ETF

Home » Strategies » Exchange Traded Funds » Blueprint Chesapeake Multi-Asset Trend » TFPN Commentary

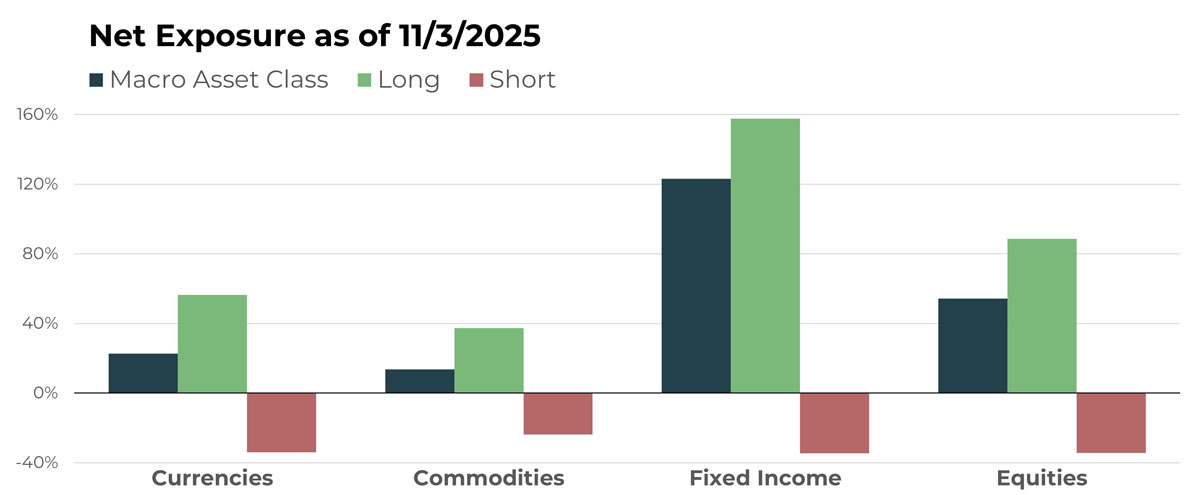

Portfolio Exposure At A Glance

Notable Holdings By Macro Asset Class

| CURRENCIES | |

|---|---|

| Name | Long/Short |

| Indonesian Rupiah/U.S. Dollar | Short |

| Australian Dollar/China Yuan | Long |

| Philippine Peso/U.S. Dollar | Short |

| British Pound Sterling/China Yuan | Long |

| Canadian Dollar/U.S. Dollar | Short |

| COMMODITIES | |

|---|---|

| Name | Long/Short |

| Live Cattle | Long |

| Wheat Future | Short |

| Sugar Future | Short |

| Silver Future | Long |

| Zinc Future | Long |

| FIXED INCOME | |

|---|---|

| Name | Long/Short |

| Japan 10-Year Treasury Bond | Short |

| U.S. 30-Year Treasury Bond | Short |

| U.S. 10-Year Treasury Bond | Long |

| High Yield Corporate Bond Index Future | Long |

| Australian 10-Year Bond | Long |

| EQUITIES | |

|---|---|

| Name | Long/Short |

| Axon Enterprise | Long |

| Waste Management | Short |

| Agnico Eagle Mines Ltd | Long |

| Kratos Defense | Long |

| Proctor & Gamble Co | Short |

ETF holdings and macro asset class allocations are subject to change.

Currencies

Overview

The early stages of a U.S. Dollar rally have done little to alter the portfolio’s foreign currency positioning. Allocations to international currencies remain net long by roughly a 3:1 margin, while cross-rate exposure has been largely stable since the prior update. Within crypto, exposure also remains net long and virtually unchanged from October.

Drivers

With the U.S. government shutdown limiting economic data releases, investor focus shifted toward persistent inflation concerns, which have nudged the U.S. Dollar modestly higher over the past one to two months. While this movement has yet to produce significant changes in the portfolio’s international currency exposure, it could prompt adjustments as the year draws to a close.

Among cross rates, the Swiss Franc, British Pound, Euro, and Nordic currencies continue to show relative strength.

Bitcoin’s recent pullback leaves it positioned for a potential reduction in exposure, though it currently remains the portfolio’s largest crypto allocation.

Commodities

Overview

Despite modest increases in metals exposure and a slight uptick in energy allocations, the portfolio’s overall commodity exposure is in decline. The shift reflects a substantial increase in net short positioning in grains, along with a pivot from net long to net short in soft commodities. Livestock, which was previously the largest long allocation within commodities, will again see its net long exposure reduced.

Drivers

Although gold retraced during the second half of October, it remains the portfolio’s largest single net long commodity position. Its allocation continues to rival the combined net long exposures in cattle and coffee, both of which remain meaningful. On the short side, wheat has become the largest position, followed by sugar.

Fixed Income

Overview

For the second consecutive month, perhaps the biggest story for TFPN is the increase in exposure to intermediate- and long-duration bonds. This adjustment is once again paired with a reduction in short-duration exposure. The result is a larger positioning toward declining interest rates, in both the U.S. but internationally.

Drivers

The U.S. government shutdown has influenced the trend in the U.S. dollar and is also likely contributing to uncertainty around the path of interest rates. Many have interpreted Fed Chair Jerome Powell’s recent comments as reinforcing that uncertainty. That said, after the latest rate cut, the trends appear clearer, and TFPN is positioned accordingly.

Equities

Overview

U.S. equities wobbled in early October but ultimately advanced to new all-time highs. This move led to another modest increase in net long exposure. Equities remain the portfolio’s second-largest net long allocation, behind only fixed income.

Drivers

Centrus Energy, Carpenter Technology, and Kratos Defense are overtaking recent mainstays Strategy and AZZ Inc. as the largest equity holdings. The prior leaders remain meaningful positions but will relinquish their top spots to these relative newcomers.

On the short side, Ingredion Inc. represents the largest position, followed by Procter & Gamble, Waste Connections, and Bristol-Myers Squibb.

Portfolio Managers’ Note

The continued follow through in stocks, combined with strengthening trends in fixed income, drove another positive month for TFPN in October — its sixth consecutive gain. Sustained trends have now pushed TFPN back into positive territory for the year and within roughly 2% of its all-time high since inception in July 2023.

As described above, the portfolio remains positioned to benefit from a relatively weaker U.S. Dollar and a more dovish monetary backdrop. A rising tide in equities may broadly lift markets, but TFPN remains intentionally noncorrelated to traditional stock exposures.

“You don’t make money when you buy stocks, and you don’t make money when you sell stocks. You make money by waiting. It’s waiting that helps you as an investor, and a lot of people just can’t stand to wait.” —Charlie Munger

While the recent run is encouraging after a stretch of unfavorable conditions in late 2024 and early 2025, it does not alter our commitment to the systematic investing process. The strategy underpinning TFPN is approaching its fifth decade in operation — and we can’t help but chuckle at the idea of abandoning the principles that have delivered such enduring results.

That’s not to say change doesn’t matter. Innovation is constant, but it resembles fine-tuning a recipe more than rewriting it. We often say the concepts are few, but the methods are many — meaning principles rarely change, even as tactics and ingredients evolve over time.

Those ingredients continue to shift within TFPN. Winners persist; losers are removed quickly. What began as a portfolio shaped by rising interest rates and rapid inflation has transitioned into one benefiting from falling rates and a blend of both rising and declining commodity prices. Equities have generally contributed, though not always — as demonstrated as recently as the spring. Regardless of what comes next, our objective remains the same: to provide investors with valuable noncorrelation alongside their traditional assets.

The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted.

For standardized performance please visit tfpnetf.com.

Let's Talk

If you’d like to learn more about TFPN, a next-generation liquid alternative