November 15, 2023

November 2023 Commentary Blueprint Chesapeake Multi-Asset Trend ETF

Home » Strategies » Exchange Traded Funds » Blueprint Chesapeake Multi-Asset Trend » TFPN Commentary

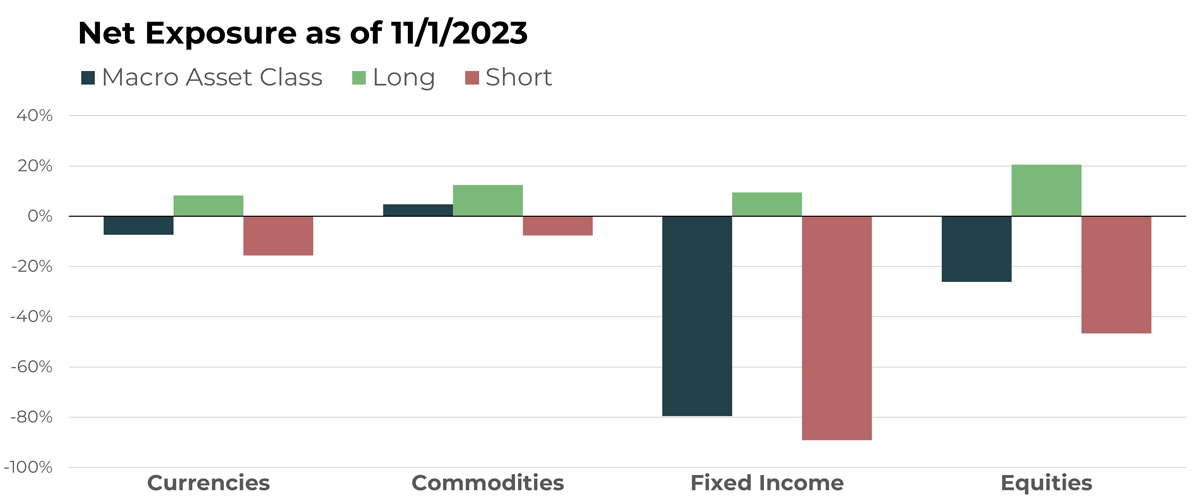

Portfolio Exposure At A Glance

Notable Holdings By Macro Asset Class

| CURRENCIES | |

|---|---|

| Name | Long/Short |

| Euro/British Pound Future | Short |

| U.S. Dollar/Chinese Yuan Future | Long |

| Euro/Swiss Franc Future | Short |

| Swedish Krona Future | Short |

| Euro/Japanese Yen Future | Long |

| COMMODITIES | |

|---|---|

| Name | Long/Short |

| Live Cattle Future | Long |

| WTI Crude Future | Long |

| Lumber Future | Short |

| LME Lead Future | Long |

| White Sugar Future | Long |

| FIXED INCOME | |

|---|---|

| Name | Long/Short |

| 3-Month Euribor Future | Short |

| iShares National Muni Bond ETF | Long |

| U.S. 5-Year Note Future | Short |

| SPDR Portfolio High Yield Bond ETF | Long |

| iShares TIPS Bond ETF | Short |

| EQUITIES | |

|---|---|

| Name | Long/Short |

| elf Beauty Inc | Long |

| Coca Cola | Short |

| AZZ Inc | Long |

| BWX Technologies Inc | Long |

| Keurig Dr Pepper Inc | Short |

ETF holdings and macro asset class allocations are subject to change.

Currencies

Overview

Short positions in the Euro against currencies like the British Pound and Swiss Franc have been a fixture of the currency portfolio in recent months. However, in October, the weakening Pound countered this prevailing trend, causing the Euro cross-trade against the portfolio to move unfavorably. The Euro-Swiss Franc pair performed better, as the Euro sank to new lows, though a reversal in the second half of October erased some of these gains.

Other notable currency positions that boosted the portfolio in October and continue in November are long the U.S. Dollar versus the Chinese Yuan, long the Euro versus the Japanese Yen, and short the Swedish Krona future.

Drivers

A month of speculation about upcoming monetary policy across central banks played a key role in volatile trading for currency markets in October. Several currencies and currency pairs reached new highs or lows, aligning with prevailing trends, before reversing course later in the month. Markets appear to be pricing in growing odds that the U.S. Federal Reserve and the European Central Bank, among others, are not only done raising rates, but may cut rates relatively quickly to keep pace with declining inflation. This shift in expectations is prompting a similar pivot in currency prices.

Commodities

Overview

Several long positions pulled back to their longer-term averages in October, including live cattle, WTI crude, and sugar futures. This resulted in declines for this macro asset class of the portfolio. These losses were partially offset by profitable short positions, like the lumber allocation. While the broader trends remain intact for now, a continuation of these countertrend movements could reverse the situation. Overall, the pullbacks in major long holdings weighed on performance last month, though shorts helped cushion the declines.

Drivers

Beliefs that inflation has peaked and interest rate hikes are likely over contributed to downward pressure on global commodity prices. Turning points in trends usually lead to short-term pain for trend-following systems, but turning points are also part of the process for realizing long-term gains. Sticking with winners means holding on longer than can feel comfortable, but a shift in economic indicators could swiftly validate the continuation of a trend, underscoring the value of maintaining exposures.

Fixed Income

Overview

After challenging or making new lows in October, both domestic and international bond instruments experienced a broad rally in the latter half of the month. These rallies have not yet resulted in long-term trend changes or material adjustments in exposure.

Looking forward, should a trend change occur, the disciplined, systematic process driving TFPN’s exposure will adjust, potentially setting the stage for opportunities on the long side if monetary policies shift.

Drivers

As has been the theme throughout this month’s update, the building consensus away from monetary tightening and toward easing has been the main exposure driver in October. Economic data appears to support the case that central banks are pausing rate increases, perhaps for the foreseeable future, and looking ahead to decreases in 2024. Given how far bonds of any duration have fallen, a retracement to the long-term average upwards could create substantial trends on which TFPN is ready to capitalize.

Equities

Overview

TFPN’s net short exposure to equities, which began in September, continues and in fact increased. Among the notable short positions are consumer beverage companies Coca Cola and Keurig Dr. Pepper. These are countered by longs in a wide range of industrial, technology, and consumer product companies.

With U.S. stock markets in decline in October, short positions benefitted. This highlights the potential benefits of TFPN’s diversified approach, as we saw some long positions (like BWX Technologies) make new all-time highs even as the larger market struggled.

Drivers

Despite a strong S&P 500 rally in the closing days of October, the benchmark index continues to experience a series of lower highs. Until that pattern is broken, a return to all-time highs is obviously off the table. The distinct change in tone and sentiment in terms of inflation, as well as interest rates, should theoretically bode well for stocks. That said, there are a multitude of factors that could create a downside surprise. TFPN’s broad, hedged exposure leaves the ETF well-positioned, in our opinion.

Let's Talk

If you’d like to learn more about TFPN, a next-generation liquid alternative