March 14, 2025

March 2025 Commentary Blueprint Chesapeake Multi-Asset Trend ETF

Home » Strategies » Exchange Traded Funds » Blueprint Chesapeake Multi-Asset Trend » TFPN Commentary

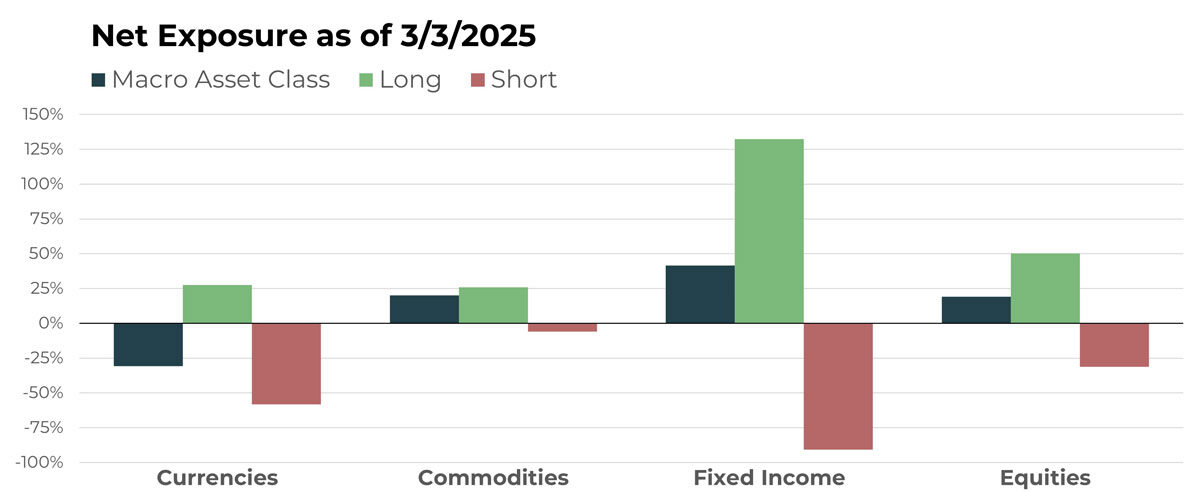

Portfolio Exposure At A Glance

Notable Holdings By Macro Asset Class

| CURRENCIES | |

|---|---|

| Name | Long/Short |

| Swedish Kronor/Japanese Yen | Long |

| British Pound/Swiss Franc | Long |

| Polish Zloty/Euro | Long |

| Brazilian Reais/U.S. Dollar | Short |

| Colombian Peso/U.S. Dollar | Short |

| COMMODITIES | |

|---|---|

| Name | Long/Short |

| Live Cattle Future | Long |

| Rough Rice Future | Short |

| Soybean Meal Future | Short |

| Gold Future | Long |

| Cocoa Future | Long |

| FIXED INCOME | |

|---|---|

| Name | Long/Short |

| iShares 0-5 Year High Yield Corp Bond ETF | Long |

| iShares Short-Term National Muni Bond ETF | Long |

| U.S. 10-Year Note | Short |

| SPDR Bloomberg High Yield Bond ETF | Long |

| Japan 10-Year Bond Future | Short |

| EQUITIES | |

|---|---|

| Name | Long/Short |

| TKO Group Holdings Inc | Long |

| Invitation Homes Inc | Short |

| Carpenter Technology Corp | Long |

| Canadian National Railway Co | Short |

| AZZ Inc | Long |

ETF holdings and macro asset class allocations are subject to change.

Currencies

Overview

Net short exposure to non-U.S. Dollar denominated currencies has increased.

From an overall asset perspective, currencies will now represent the most significant allocation except for long fixed income. Economic data in early March will likely test this position, as the U.S. Dollar pulls back from its most recent strength during late 2024 and early 2025.

Drivers

Against the U.S. Dollar, shorts of the Singapore Dollar and Canadian Dollar remain the largest and second largest positions, respectively. Unfortunately, both allocations moved countertrend in February and opened March similarly. Also moving counter to the prevailing U.S. Dollar trend are long positions to the Israeli Shekel and the Thai Baht.

As February closed, the ratio of long U.S. Dollar to short U.S. dollar cross rates was near 10:1 in favor of long exposure.

Another important feature of TFPN’s currency portfolio are foreign currency pairs, which provide a valuable variance of exposures and allow the ETF to benefit from substantial trends when they materialize. In this portion of the currency book, the most sizable positions are currently the Euro (short) versus the Swedish Krona (long), followed by a couple of China-based pairs (long) versus the Euro and versus the Canadian Dollar (both short).

Commodities

Overview

Net long exposure will remains marginal and virtually unchanged from February. Food and fiber products once again make up the largest allocation but to a lesser degree than previous months. Livestock products are the next-largest segment and remain unanimously long. Metals, energy, and grains continue to be slightly long but currently are not major players.

Drivers

Both U.S. and London cocoa futures have been the stuff of legend on uptrends in recent years, but they suffered substantial pullbacks in February. They remain the largest commodity positions, but that may be short-lived if there are further declines to close the first quarter.

Cattle futures remain the largest livestock allocations and are among the largest in the commodity complex. However, like so many other positions in February, there was a reversal that resulted in losses for the month.

A bright spot in TFPN continues to be the long gold position, which completed its second consecutive positive month to open 2025.

Fixed Income

Overview

Overall, fixed income exposure will remain net long. However, as always, the story really is in the details.

Fixed income ETF holdings centered on corporates, municipals, and mortgage-backed instruments, to name a few, are unanimously long. Short-term interest rates, such as the Euribor and UK bonds, are now two-to-one long. Meanwhile, futures positions making up the U.S. yield curve from the 2-year to the 30-year are short. International bond futures are more mixed but predominantly short.

Drivers

The short positions across the U.S. yield curve, from the 2-year to the 30-year, generally worked against the portfolio in February. International bond futures are more mixed but predominantly short, with significant short positions in the Australian 3-year and 10-year Treasury bonds.

Among fixed-income ETFs, the largest allocation is the iShares National Muni Bond ETF (SUB), which produced its second consecutive positive monthly return.

Equities

Overview

The once-dominant long equity allocation within TFPN continues to dwindle as trends weaken. As the quarter heads to a close, it is now one of the smaller net allocations in the portfolio, with shorts coming within striking distance of matching longs.

Crypto and blockchain assets remain material but obviously less so as these trends retrace.

Drivers

Once the largest long equity allocation, MicroStrategy remains a large holding, but has taken a backseat to others, such as AZZ Inc. and TKO Group Holdings. Carpenter Technology Corp, a previously unmentioned long equity position, followed a 14% increase in January by rising another 7% in February. Another bright spot in February was Canadian National Railway, which continues to be the largest short equity position by a sizeable margin. It resumed its downtrend with a 3% decline in February.

Portfolio Managers’ Note

In last month’s commentary, we challenged readers to set aside mainstream views about portfolio construction and embrace the nontraditional approach TFPN utilizes, along with the noncorrelated (to traditional assets) benefits it provides. Little did we know that February would make that perspective so timely.

Reversals of major currency positions, commodities, fixed income, AND equities are nightmare fuel for trend followers.

On the one hand, with so many countertrend positions, it can feel like the whole market is against you. On the other hand, even with the overwhelming number of positions moving in contrast to the prevailing trend, it is comforting that the losses were not far greater and that the current drawdown is well within expectations. Fortunately, decades of faithfully executing trend-following strategies and reaping the benefits has left us desensitized to these periods of choppiness.

In portfolio construction, it pretty much all comes down to choices around timeframe and the main component the manager is attempting to solve for. In our case, we want to provide a tool that seeks to protect against, and may even benefits from, long-term declines in traditional assets. In that sense we are only in the very beginning of a potential shift in the market narratives that have dominated since 2022.

We were talking to one of our favorite financial advisors this week and laughingly when observing how you never really know. It is so easy to create a narrative that favors a resumption of those dominant uptrends since 2022, but it is also easy to develop a scenario where markets stay sideways for a while or even decline precipitously. In the end, we drew comfort that as trend followers it doesn’t matter either way, as our strategy is designed to eventually find its footing and benefit when trends emerge and persist.

Let's Talk

If you’d like to learn more about TFPN, a next-generation liquid alternative