June 16, 2025

June 2025 Commentary Blueprint Chesapeake Multi-Asset Trend ETF

Home » Strategies » Exchange Traded Funds » Blueprint Chesapeake Multi-Asset Trend » TFPN Commentary

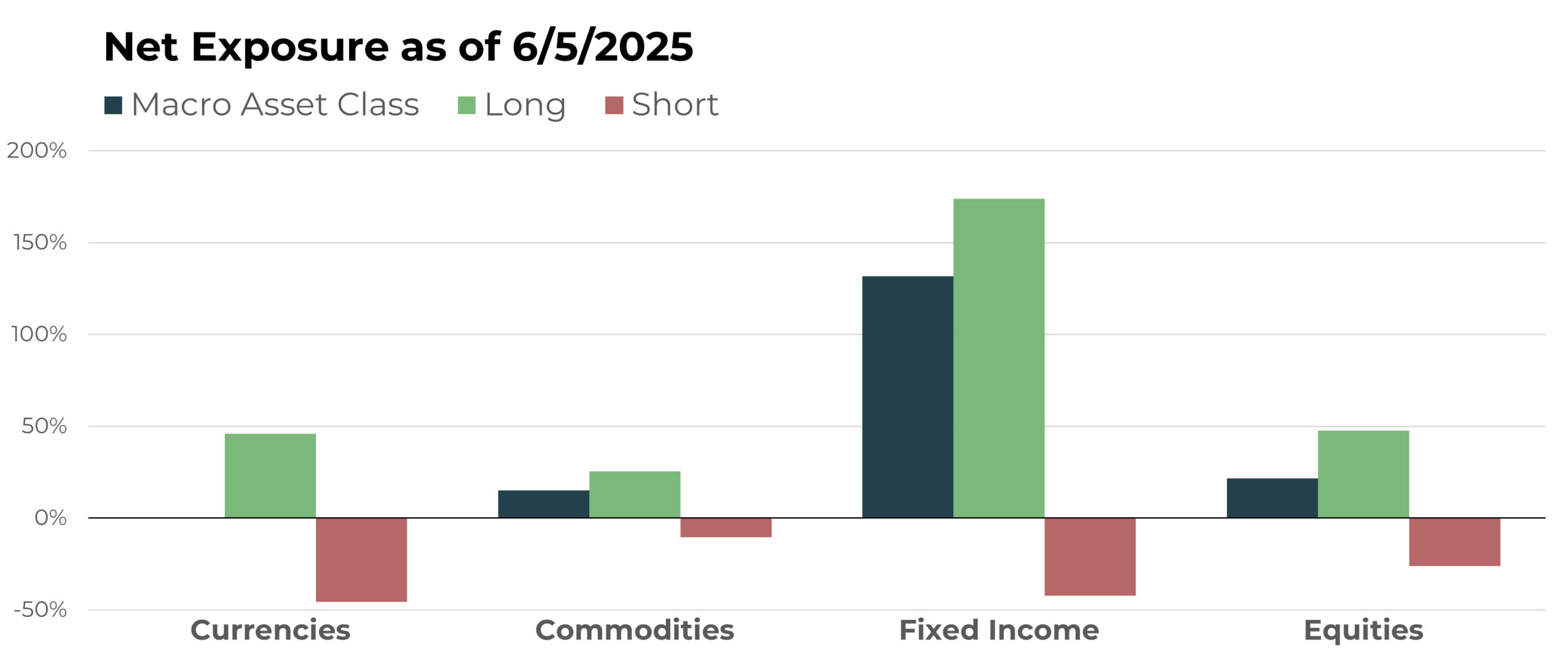

Portfolio Exposure At A Glance

Notable Holdings By Macro Asset Class

| CURRENCIES | |

|---|---|

| Name | Long/Short |

| iShares Bitcoin Trust ETF | Long |

| Philippine Peso/U.S. Dollar | Long |

| Indonesian Rupiah/U.S. Dollar | Short |

| Canadian Dollar/U.S. Dollar | Short |

| Euro/Czech Koruna | Short |

| COMMODITIES | |

|---|---|

| Name | Long/Short |

| Cocoa Future | Long |

| Lumber Future | Short |

| Cattle Future | Long |

| Gold Future | Long |

| Zinc Future | Short |

| FIXED INCOME | |

|---|---|

| Name | Long/Short |

| iShares National Muni Bond ETF | Short |

| iShares Short Term National Muni Bond ETF | Long |

| U.S. 30-Year Treasury Bond | Short |

| iShares 0-5 Year TIPS Bond ETF | Long |

| Australian 10-Year Bond | Short |

| EQUITIES | |

|---|---|

| Name | Long/Short |

| Carpenter Technology Corporation | Long |

| Canadian National Railway | Short |

| Pepsico Inc | Short |

| AZZ Inc | Long |

| Microstrategy Class A | Long |

ETF holdings and macro asset class allocations are subject to change.

Currencies

Overview

The U.S. Dollar started May with strength but peaked mid-month and ultimately finished only modestly higher. That failed rally continued the recent trend of declining exposure to the U.S. Dollar in favor of foreign currencies. At the start of May, TFPN was nearly hedged (1:1 exposure). By month-end, it was a roughly 1.4-to-1 tilt favoring foreign currencies.

Despite heightened rhetoric around tariffs potentially reigniting inflation, the data has yet to confirm those concerns. With inflation appearing stable — or even easing slightly — and growth softening, the potential for lower interest rates remains on the table. This combination continues to apply downward pressure on the U.S. Dollar and upward pressure on foreign counterparts.

Drivers

Taking a deeper look into TFPN’s portfolio reveals a fresh set of individual positions holding the highest exposure. After declining against the U.S. Dollar for the better part of a decade, the Philippine Peso has developed a bullish trend that has propelled it to a sizeable allocation versus the U.S. Dollar. Another notable long position is the Indian Rupee, which continued to strengthen and now represents one of TFPN’s more significant exposures.

Commodities

Overview

While the anticipated inflationary impact of tariffs has yet to materialize, commodity prices remained relatively muted in May. As a result, TFPN’s modest net long exposure remains largely unchanged. Energies, metals, and grains continue to be nearly hedged, while livestock and materials futures maintain a net long bias. That said, even these once-dominant segments have shown signs of softening, with new short positions emerging in lean hogs, cotton, and lumber.

Drivers

Though commodities had limited influence on overall fund performance this month, several key positions remain in place that can capitalize on any renewed trends.

TFPN has profitably reduced exposure to coffee futures, while cattle and cocoa continue to be meaningful allocations. Notably, cattle futures have now overtaken cocoa as the largest individual commodity position in the portfolio.

Fixed Income

Overview

After a meaningful increase in duration exposure heading into May, TFPN will pause on further allocations in this direction, as those positions generally failed to follow through. Uptrends in intermediate-term bonds remain intact — though increasingly fragile — while short-term bond trends continue to point upward. In contrast, long-term bond trends remain clearly down, and TFPN is keeping those exposures short.

Drivers

The most influential positions are concentrated in European bonds, particularly the Euro BTP, which now accounts for nearly half of TFPN’s long fixed income exposure among intermediate-duration instruments. Other notable allocations include a variety of international short-term bonds. A particularly interesting position is TFPN’s short in the September 30-day Fed Funds contract. While that trend direction implies expectations for lower interest rates, correlation doesn’t always imply causation — especially in today’s policy environment.

Equities

Overview

Over the past month or so, TFPN’s equity exposure shifted from nearly balanced to modestly net long. What was once the dominant asset allocation in 2024 remains relatively subdued as we approach the halfway point of 2025. In the absence of a clear directional trend, our trend following system’s focus continues to be identifying individual winners — both long and short — while allowing other asset classes to drive broader performance.

Drivers

The key holdings within the equity sleeve remain largely unchanged. Strategy Inc. (formerly MicroStrategy) declined in May but continues to be TFPN’s largest long allocation. It is followed by AZZ Inc., TKO Group Holdings, and Carpenter Technology. On the short side, Canadian National Railway remains the most significant position.

Portfolio Managers’ Note

Sometimes being a trend follower feels like the old farmer in the Chinese proverb, “We’ll see.” In other words, when others are hailing trend following’s genius or good fortune, we tend to stay even-keeled, knowing that tougher times may be ahead. Likewise, when those around us are expecting us to be discouraged, we remain steady; if anything, this is likely an opportunistic time.

In versions of the proverb we have read, it doesn’t go into detail about why the old farmer is stoic in the face of seemingly good and bad fortune. However, for us in the asset management context, the explanation is simple: After years of testing systematic strategies and then executing them across a wide range of market environments, our conviction is so high. Plus, the fit between our systems and our personalities so compatible. We can ignore all the noise and remain committed to executing our process.

People’s views about what is “good” and “bad” are often rooted in mainstream beliefs that only time will prove to be correct or incorrect. From an investment standpoint, what can seem like a great decision for a long time can ultimately prove to be devastating to performance. Likewise, what can seem idiotic to some can turn out to be the best strategy over the timeframes that count.

One of our favorite movies is, “The Big Short,” adapted from the book of the same name by Michael Lewis. One of the reasons we love it is the instant karma that takes place for those smugly pushing flawed strategies and ignoring the risks present before and during the Financial Crisis of 2007 to 2009. We vividly remember the pre-crisis doubters becoming post-crisis believers in the benefits of systematic investing.

Sadly, the memories of that time have all but faded, and we find ourselves once again in a period that is difficult for trend followers. Does that mean we are on the cusp of another great period for us? Is this the end of trend following?

We’ll see…

Let's Talk

If you’d like to learn more about TFPN, a next-generation liquid alternative