June 14, 2024

June 2024 Commentary Blueprint Chesapeake Multi-Asset Trend ETF

Home » Strategies » Exchange Traded Funds » Blueprint Chesapeake Multi-Asset Trend » TFPN Commentary

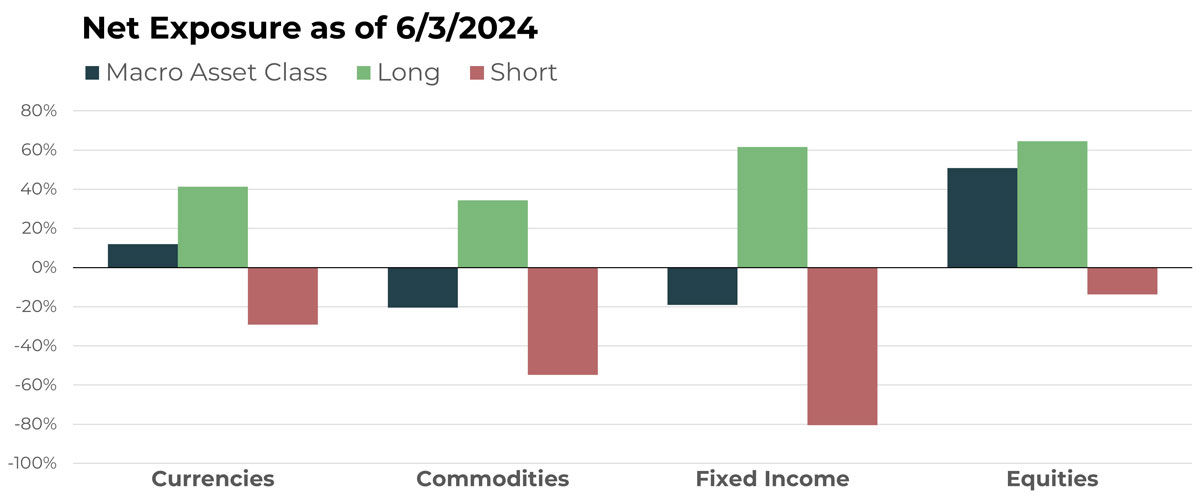

Portfolio Exposure At A Glance

Notable Holdings By Macro Asset Class

| CURRENCIES | |

|---|---|

| Name | Long/Short |

| Chinese Yuan/Singapore Dollar | Short |

| Australian Dollar/Japanese Yen | Long |

| Chinese Yuan/Japanese Yen | Long |

| Australian Dollar/New Zealand Dollar | Short |

| Euro/Swiss Franc | Long |

| COMMODITIES | |

|---|---|

| Name | Long/Short |

| Frozen Orange Juice Future | Long |

| Copper Future | Long |

| Platinum Future | Long |

| Lumber Future | Short |

| Cocoa Future | Long |

| FIXED INCOME | |

|---|---|

| Name | Long/Short |

| SPDR High Yield Bond ETF | Long |

| iShares Short-Term National Muni Bond ETF | Long |

| U.S. 2-Year Note Future | Short |

| Canadian 10-Year Bond Future | Short |

| Japan 10-Year Bond Future | Short |

| EQUITIES | |

|---|---|

| Name | Long/Short |

| Sonoco Products Co | Long |

| Schlumberger NV | Short |

| UFP Technologies Inc | Long |

| AZZ Inc | Long |

| Vital Farms, Inc. | Long |

ETF holdings and macro asset class allocations are subject to change.

Currencies

Overview

We often discuss why we think TFPN’s currency portfolio is unique. Specifically, we have highlighted our ability to compile a wide range of positions due to the options available. June’s opening allocations are a great example of this. Not many asset classes are diverse enough to allow you to be both long and short the same instrument in equal amounts without hedging yourself out. Yet, for TFPN’s positions, both the Chinese Yuan and Australian Dollar are both a notable long allocation and a notable short allocation. The key difference is the currency they are paired with to derive the underlying trend. On the short side, the Yuan is paired against the stronger Singapore Dollar, while on the long side it is paired against the weaker Japanese Yen. Likewise, the Australian Dollar is held long against the Yen and short against the currency of its neighbor across the Tasman Sea (New Zealand).

We believe a quick glance at the recent trends illustrates the power of such an approach.

Drivers

Asia-Pacific currencies dominate the notable holdings list as we enter June.

Despite experiencing its country’s first rate hike in 17 years in March, the Japanese Yen continues to be relatively weak as inflation remains in check. Its weakness makes it a prime target to be paired up with stronger currencies, such as the Chinese Yuan and Australian Dollar. The so-called “carry trade” of borrowing at low interest rates and investing in higher returning assets has been associated with Japan for many years now given its persistently low rates. We find it interesting to see trend following pick up on such market phenomenon without the burden of fundamental analysis or prediction.

Commodities

Overview

TFPN’s commodity portfolio continues to be net short, despite the list of notable longs above.

After declining more than 14% in April, lumber futures rose slightly in May. However, downtrends remain in place and the opening days of June saw this market trade lower again.

On the long side, repeat readers of this monthly update should recognize positions that have been prominent in past notes, such as orange juice, copper, and of course cocoa. OJ broke out from a tight range to climb over 14% in May. Similarly, copper and cocoa both enjoyed positive, though volatile, months as upward trends continue.

Drivers

Higher rates for longer has been a theme of the first half of 2024, which has had an impact on construction, a major factor in lumber demand. It is likely that this is one of, if not the primary, economic driver behind this downtrend.

As for the notable longs, a combination of political and weather factors likely have impacted the direction these commodity prices.

As a trend-following ETF, the economic backstory is irrelevant to decision-making, as price and underlying rules are all that matter. However, it is validating to see trends and subsequent portfolio allocations reflect economic realities on the ground.

Fixed Income

Overview

TFPN is coming up on its one-year anniversary of trading. Among its opening allocations was a bet against bond prices (short bonds) in the midst of a rate-raising cycle by many global central banks, including the U.S. Reductions in the rate of inflation, followed by official statements indicating an end to rate increases, gave way to a strong rally in bond prices as investors anticipated the beginning of rate cuts. TFPN’s portfolio reacted accordingly by adapting to the new environment and shifting from net short to net long within just a few months toward the end of 2023.

Sticky inflation and other strong economic data have kept rates high and caused a shift in investor sentiment. The result has been a gradual decline in bond prices and a reversal in TFPN’s portfolio from net long to once again net short as we enter the summer months.

Among notable long positions, short duration European bonds are prominent. Notable shorts include U.S. short-term interest rate futures contracts.

Drivers

It’s all about the path of interest rates for bond trends. The most recent economic reports have left the door open for cuts in 2024. Markets have reacted accordingly with both bonds and stocks rallying, the latter to another all-time high. It seems a decline in rates is inevitable, but the question is timing.

It would not be surprising to soon see another significant net long position for the bonds portfolio, but the markets have a way of doing the unexpected. The beauty of a trend-following process, in our opinion, is the ability to eventually be with the dominant trend without having to (or even attempting to) get the exact timing correct.

Equities

Overview

For the second consecutive month, TFPN’s largest net exposure will be long equities.

A notable position is Sonoco Products, which broke out from its range to increase 9.5% in May. Other solid-performing long positions and mainstays of the portfolios are UFP Technologies and AZZ, which both made new 20+ year highs in May. Vital Farms, another notable long, followed a string of 25% in February, 29% in March, and 15% in April by increasing a staggering 55% in May. It is our belief that it would be difficult to stick with and benefit from a trend like that without the discipline of a systematic process like trend following.

While long positions like those noted above are certainly headline grabbers, it is also important to keep TFPN’s short book in mind. Stocks like these can deviate substantially, but there is generally a positive correlation. Thus, adding shorts will usually reduce the overall portfolio’s risk by adding a bit of a hedge. One notable short is Schlumberger. Its presence in the portfolio reduced risk in May and added to the bottom line as it declined 3.4% for the month.

Drivers

Earnings and economic data continue to be generally positive for stocks. Combine this with a lingering belief in upcoming accommodative monetary policy and you have a solid recipe for increasing stock prices. Trends reflect this environment overall, and as a result we expect that TFPN’s portfolio will continue to carry substantial long exposure to stocks for the foreseeable future. As our bond commentary demonstrates, TFPN is always ready to adapt to changing conditions and could just as easily be net short stocks in future updates. For now, however, long is the direction that continues to benefit TFPN investors.

Portfolio Managers’ Note

“Strong beliefs, loosely held” is a philosophy of developing deep convictions but remaining openminded enough to change if the data and experience dictate it. The practice of executing a trend-following portfolio can be likened to this. Significant positions can be built up in one direction or another across a vast array of markets, but we never become attached to any position or direction. This allows us to benefit from dominant trends without losing our nimbleness or adaptability.

The current portfolio reflects this thinking and execution. A portfolio that was net short in stocks almost one year ago now has its largest exposure on the long side to stocks. The fixed income book has rotated from net short to net long and back to short again. Commodities and currencies have likewise run the gamut.

When it’s all said and done, TFPN continues to provide the same noncorrelation benefits for portfolios by being both long and short a range of markets and asset classes. The difference between TFPN and other non-correlated strategies has been its ability to do so without creating significant drag in an environment where stocks have done well. Ultimately, we believe this is why TFPN is a good fit for many portfolios.

With an election on the horizon, interest rate forecasts in flux, and wars continuing to rage, we continue to feel strongly that adaptability is priceless. This is the motivating factor behind the disciplined execution of our strategy.

Let's Talk

If you’d like to learn more about TFPN, a next-generation liquid alternative