July 14, 2025

July 2025 Commentary Blueprint Chesapeake Multi-Asset Trend ETF

Home » Strategies » Exchange Traded Funds » Blueprint Chesapeake Multi-Asset Trend » TFPN Commentary

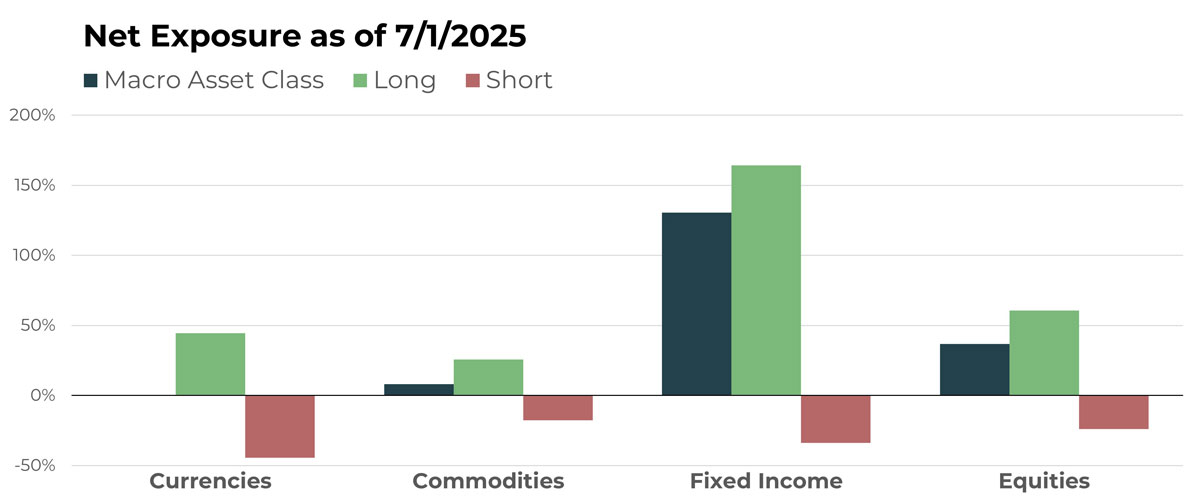

Portfolio Exposure At A Glance

Notable Holdings By Macro Asset Class

| CURRENCIES | |

|---|---|

| Name | Long/Short |

| iShares Bitcoin Trust ETF | Long |

| Indian Rupee/U.S. Dollar | Long |

| Indonesian Rupiah/U.S. Dollar | Short |

| Euro/Czech Koruna | Short |

| China Yuan/U.S. Dollar | Short |

| COMMODITIES | |

|---|---|

| Name | Long/Short |

| Silver Future | Long |

| Sugar Future | Short |

| Cocoa Future | Long |

| Gold Future | Long |

| Rough Rice | Short |

| FIXED INCOME | |

|---|---|

| Name | Long/Short |

| iShares National Muni Bond ETF | Short |

| iShares Short Term National Muni Bond ETF | Long |

| U.S. 30-Year Treasury Bond | Short |

| U.S. 3-Year Treasury Note | Long |

| Australian 10-Year Bond | Short |

| EQUITIES | |

|---|---|

| Name | Long/Short |

| TKO Group Holdings Inc | Long |

| Alimentation Couche-Tard Inc | Short |

| General Mills | Short |

| Ecolab Inc | Long |

| Corteva Inc | Long |

ETF holdings and macro asset class allocations are subject to change.

Currencies

Overview

The U.S. Dollar declined once again in June, reaching a new multi-year low. The continued slide meant that foreign currency exposure increased again as we headed into July. In terms of foreign cross rates, Asia-Pacific currencies remain the weakest, while Eastern European and Nordic countries are the strongest. Exposure to cryptocurrencies and blockchain also rose.

Drivers

Relative to the U.S. Dollar, the Mexican Peso was the largest foreign currency position as July began. The Israeli Shekel, Euro, and Thai Baht are also notable in terms of size. The U.S. Dollar is stronger against only a handful of currencies, most notably the Chinese Yuan and Indonesian Rupiah. Among cross rates, the Australian and Chinese currencies are the weakest, while the Swiss Franc, Swedish Krona, and Norwegian Krone are among the strongest.

Commodities

Overview

Livestock overtook cocoa as the top commodity allocation at the start of July. Net long exposure to metals and energy increased slightly but remains smaller than the livestock and cocoa allocations. Grains continue to be the only net short segment, though that position declined modestly.

Drivers

Cattle futures are now the dominant individual commodity position, followed by cocoa. Gold trends remain strong and round out the top three. As noted, grains are the only net short commodity segment, with rough rice, sunflower seeds, and soybeans leading the way.

Fixed Income

Overview

Intermediate- to long-term duration bonds remain weak, which means TFPN’s net short position increased as June ended and July began. Short-term bonds continue to make up the largest single segment of the portfolio, though the overall net long position declined slightly. Fixed income ETFs were the lone segment to experience an increase in net long allocation.

Drivers

Like their currency counterparts, Australian 10-year bonds are weak and make up the largest short position among medium- to long-duration instruments. The largest long positions can be found in the Eurozone. While not the largest allocation among short-term bonds, U.S. Fed Funds futures represent the largest short position — reflecting a trend toward expectations of higher benchmark rates. Among fixed income ETFs, short-term municipals and short-term inflation-protected securities are the two largest long allocations.

Equities

Overview

In a quick reversal that mirrored the overall equity markets, TFPN’s stock portfolio nearly doubled its long position, with both longs increasing and shorts decreasing throughout June. The change left this asset class firmly entrenched as the second-most influential, behind only fixed income. Due to the higher volatility typically seen in equities, one could argue stocks are currently the most influential on a volatility-adjusted basis.

Drivers

Due to entrenched trends, the largest individual holdings within the equity bucket remain mostly unchanged. Strategy Inc. (formerly MicroStrategy) was generally flat in June but continues to be TFPN’s largest long allocation. It is followed by AZZ Inc., TKO Group Holdings, and Carpenter Technology. On the short side, Canadian National Railway remains the most significant position.

Portfolio Managers’ Note

Although a period devoid of an abundance of trends pushed TFPN into a tough start for 2025, the fund quietly produced its second consecutive positive month in June — and single best month of the year. This remains a challenging environment for trend-based strategies using the timeframes we employ. However, a characteristic of trend following is that things can change quickly and without fanfare. As a result, disciplined practitioners tend to neither get too high about good times nor too low about tough times.

Instead of paying too much attention to short-term performance, we focus more on long-term behaviors and how TFPN fits into a traditional portfolio. While we believe a diversified trend-following strategy is arguably the best standalone investment one can make, we recognize that its uniqueness can be an obstacle for traditional investors. For this reason, we advocate an allocation within a more mainstream portfolio for most investors.

If one were to dive deeper into the four major asset classes of TFPN’s strategy (currencies, commodities, fixed income, and equities), a mainstream representation of each might be the U.S. dollar, gold, aggregate bonds, and the S&P 500 Index. In other words, when a typical investor thinks of these assets, these are the representations likely to come to mind. It is also not uncommon for these assets to show up in most portfolios, except perhaps for the U.S. Dollar.

The goal of TFPN — and, we would argue, of any good alternative investment — is to use available tools to build a noncorrelated strategy that can perform well during difficult periods for traditional investments, while not necessarily underperforming when they do well. The key word is noncorrelation. When performance can’t be judged in isolation, noncorrelation can often be judged instead.

In that context, TFPN continues to deliver as designed. During the last 12 months, it has been nearly uncorrelated with the U.S. Dollar, gold, and bonds while correlation to the S&P 500 Index has been mild. During the last 90 days, correlation to equities has ticked up slightly, but remains non-existent with the other assets. The point is: While relative performance has lagged, TFPN continues to operate within the design parameters that have guided the underlying strategy for decades.

No strategy has been declared “dead” more times than trend following — and yet it is still standing. Producing returns that are different requires being different — and, at times, being uncomfortable. It’s the same whether you’re a next-level athlete or designing investment strategies. We embrace the discomfort required to deliver prolonged performance.

Let's Talk

If you’d like to learn more about TFPN, a next-generation liquid alternative