July 15, 2024

July 2024 Commentary Blueprint Chesapeake Multi-Asset Trend ETF

Home » Strategies » Exchange Traded Funds » Blueprint Chesapeake Multi-Asset Trend » TFPN Commentary

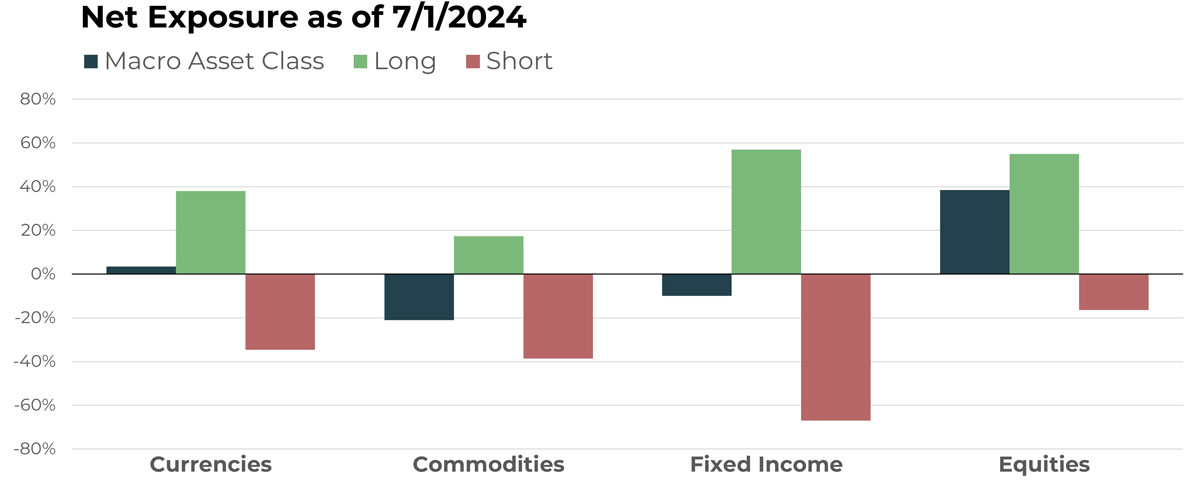

Portfolio Exposure At A Glance

Notable Holdings By Macro Asset Class

| CURRENCIES | |

|---|---|

| Name | Long/Short |

| Philippine Peso/U.S. Dollar | Short |

| iShares Bitcoin Trust ETF | Long |

| U.S. Dollar/South African Rand | Long |

| New Zealand Dollar/Canadian Dollar | Short |

| Australian Dollar/Euro | Long |

| COMMODITIES | |

|---|---|

| Name | Long/Short |

| Live Cattle Future | Long |

| Lean Hogs Future | Short |

| Gold Future | Long |

| Palladium Future | Short |

| Cocoa Future | Long |

| FIXED INCOME | |

|---|---|

| Name | Long/Short |

| U.S. 10-Year Note Future | Short |

| Vanguard Short-Term Corporate Bond ETF | Long |

| U.S. 5-Year Note Future | Short |

| SPDR Bloomberg High Yield Bond ETF | Long |

| Canadian 10-Year Bond Future | Short |

| EQUITIES | |

|---|---|

| Name | Long/Short |

| Minerals Technologies Inc | Long |

| Accenture Plc | Short |

| Joint Stock Company National Atomic | Long |

| McDonald's Corp | Short |

| Kaiser Aluminum Corp. | Long |

ETF holdings and macro asset class allocations are subject to change.

Currencies

Overview

In honor of July 4th, we begin the currency overview by highlighting two notable currency pairs involving the greenback. While one is a short position and another a long position, both are attempting to take advantage of the U.S. Dollar’s strength relative to an emerging market currency. The first instance is a short position in the Philippine Peso against the U.S. Dollar and the second is a long position in the U.S. Dollar versus the South African Rand.

Other notable holdings include a long in the Australian Dollar versus the Euro and a short of the New Zealand versus Canadian dollars. Both the Australian (long) and New Zealand (short) currencies have been experiencing persistent trends, and have been featured in recent updates, but in some cases with different currency pairs.

Drivers

Emerging markets tend to produce more volatility due to their inherently less stable condition in comparison to a developed economy like the U.S. This disparity can make them fertile ground for harvesting profitable trends. When combined with the flexibility of currency pairs and the overall broad choices available in the currency markets, these more obscure trends can offer our portfolio material incremental diversification. While we believe the ability to be both long and short is valuable for all asset segments in the portfolio, the currency portfolio stands apart in being hedged yet still capable of capitalizing on profitable trends.

For developed economies in the U.S. and Europe, the key drivers continue to be central bank planning meant to continue reducing inflation without causing recession. Recent data points have continued the trend toward lower inflation (i.e., disinflation) while important growth metrics like employment remain strong. The timing is unknown, which has caused some sideways movement in many of the portfolio’s major currency positions, but according to Fed funds futures, the next move in terms of interest rates still appears to be down.

Commodities

Overview

In terms of net exposure, TFPN’s commodity portfolio will be nearly unchanged in July, both in terms of direction (short) and magnitude.

Notable longs that should be familiar by now to frequent readers of this commentary include live cattle, gold, and cocoa futures contracts. Interestingly, we are now seeing downtrends (and hence short positions) in markets that tend to be at least loosely correlated with those longs just listed. For example, the long position in cattle is observed alongside a short position in another meat market: lean hogs. The long position in gold is balanced by a short in another metal: palladium. We believe this again highlights the benefits of maximizing diversification by not relying on proxy markets to represent sub-sector exposure.

Drivers

When trends are exploding in markets like cocoa, the appeal of trend following is obvious. In our opinion, it is difficult to conceive of a more effective method for installing a position and then hanging on long enough to capture an outlier uptrend like the one seen in 2023 and 2024. A typical question when we show people these types of positions and trends is, “So why doesn’t everyone do this?” We think the answer lies in how emotionally difficult it can sometimes be to follow the investing rules religiously.

The current behavior in cocoa since late April is a great example of why trend following is hard to do sometimes and why everyone doesn’t do it. After peaking April 19, the July contract has fallen approximately 30% without a trend change. Investors should not overlook the discipline required to give back that kind of profit. And yet despite the recent decline, cocoa has still increased around 135% during the last year.

This example speaks to the inherent nature of trend following, in our view. Being systematic sometimes means entering at a point that feels too late and exiting at point that also feels too late. In the case of cocoa, recency bias may extract a heavy emotional toll on an investor, with a near-term decrease in profits. However, taking the whole position since the trend’s inception reveals a very profitable trade that has contributed positively to client portfolios. Perhaps most importantly, the decision-making was done in a way that is consistent and repeatable, which makes it lasting for many generations.

Fixed Income

Overview

While still net short, TFPN’s exposure narrowed a bit heading into July. At a high level, the higher the duration, the more likely it is that we maintain short exposure, while long positions can be seen in the shorter-duration instruments.

Specifically, notable shorts continue in both the U.S. and Canadian 10-year bonds, with the portfolio also short the 5-year U.S. bond. With an effective duration under 3 years, the Vanguard Short-Term Corporate Bond ETF is also a notable long. Another notable long is the SPDR Bloomberg High Yield Bond ETF, which has an effective duration of just over 3 years, remains priced with uptrends at the moment, and has a current yield of just over 7.5%.

Drivers

Arguably no underlying catalyst impacting markets is under the same level of scrutiny as the path of interest rates. Almost every data point is being analyzed through the lens of what it might do to influence either the path or timing. This is the primary reason we continue to focus on rates in this commentary each month. For now, the most recent information continues to point to central banks achieving their goal of lowering inflation while keeping economic growth stable. This seemingly continues to set a stage for stable interest rates, at a minimum, with the next move likely being a cut at some point.

A factor we enjoy highlighting as a strength of trend following is that the portfolio has continued to represent the prevailing direction of interest rates without expressly incorporating any of this data into its ruleset. We are able to accomplish this because of our belief that market price reflects this information better than we ever could. Thus, by building our strategy centered on price, we believe we can most effectively and seamlessly react to what is happening.

Equities

Overview

Since April, the most prominent allocation for TFPN in terms of net exposure has been long equities. This continues to be the case in July – though the magnitude of exposure on the long side will decrease slightly.

At a high level, a major driver of TFPN’s positioning in equities can be summed up in the disparity between growth and value, which is at some of its highest levels in decades. Longs in a litany of smaller companies with very focused strategies are hedged by shorts in established player like Accenture and McDonald’s. None of these notable holdings produced eye-popping returns in June, but trends remain in place, and as a result, TFPN will continue to stay the course until things change.

Drivers

Since our last update, nothing has changed in terms of the favorability of this environment for equity returns. The most dominant trends can be found in this asset category, so it should be expected that TFPN would have its largest exposure here.

The U.S. election, the outcome of war in the Middle East and eastern Europe, and the path of global interest rates all figure to be big influences in all assets, including equities, as we move into the second half of 2024. Among these drivers, none have been able to alter uptrends observed in equities since the latter stages of 2022. Of course, it remains to be seen whether they will going forward, but TFPN will adapt accordingly.

Remember, at its inception, TFPN was net short equities and within months adapted to changing conditions to become net long equities. It is for this reason that we do not fear changes in market conditions, but rather embrace them.

Portfolio Managers’ Note

Members of our team recently read an article by performance coach Dr. Julie Gurner called, “The Life-Changing Benefits of Being Boring.” In this essay, Gurner explains that it is rarely the flashy moves that generate success but rather the steady grind of doing the small things. We’d like to believe this also represents trend following generally and specifically TFPN.

You won’t find us making bold predictions or oversized bets on any given market. You won’t catch us shouting on CNBC or another media outlet. Instead, what you will hopefully discover if you observe the team of TFPN is that our heads are down to steadily execute our system while looking for ways to enhance performance on an absolute and risk-adjusted basis.

Gurner goes on to say that, “Right now, there is an Olympic athlete somewhere in the world getting up to train. They’re putting in another lap, lifting another weight, or running another mile. They go to bed early and train even when they aren’t feeling motivated, but they just keep putting themselves forward to do the work. Making sacrifices.” She concludes this section by asking, “I wonder what that looks like to you when it comes to what you want. What’s the next lap you need to put in, even when you don’t feel like it?”

In other words, achieving greatness is a relatively simple process, but it’s very hard for humans to do it consistently.

We are all human, even us trend followers. Humans have emotions that influence behavior. Our team embraces emotion but recognizes it must be controlled or harnessed in a positive direction. For us, we build rules that allow us to avoid the pitfalls of emotion in trading and then use it to serve our clients better.

So, as folks enjoy their summer, we will hard at work putting in laps and executing our system, ready for the next challenge.

Let's Talk

If you’d like to learn more about TFPN, a next-generation liquid alternative