January 15, 2026

January 2026 Commentary Blueprint Chesapeake Multi-Asset Trend ETF

Home » Strategies » Exchange Traded Funds » Blueprint Chesapeake Multi-Asset Trend » TFPN Commentary

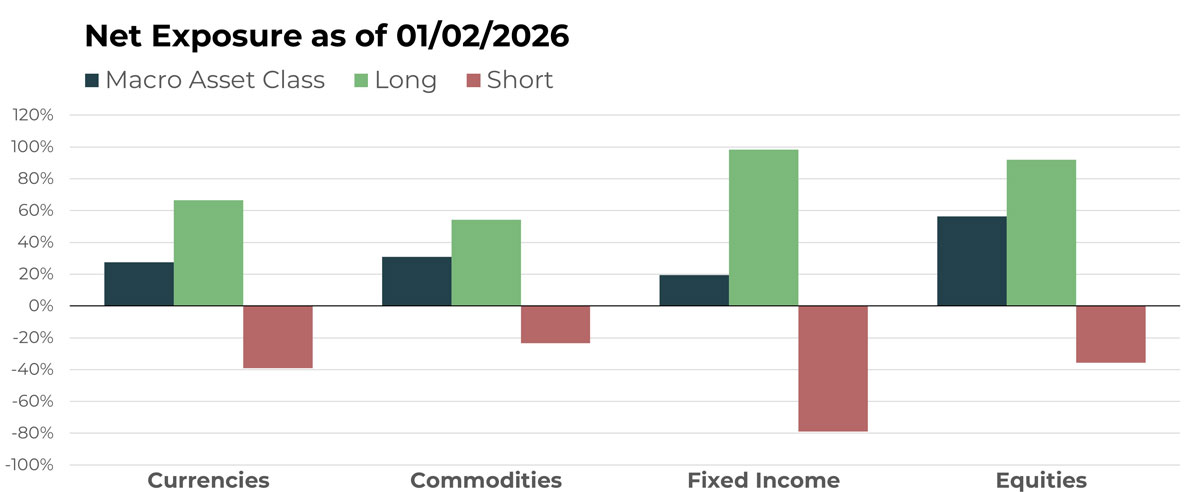

Portfolio Exposure At A Glance

Notable Holdings By Macro Asset Class

| CURRENCIES | |

|---|---|

| Name | Long/Short |

| Indian Rupee/U.S. Dollar | Short |

| Swiss Franc/Japanese Yen | Long |

| China Yuan/U.S. Dollar | Long |

| Euro/Czech Koruna | Short |

| Mexican Peso/U.S. Dollar | Long |

| COMMODITIES | |

|---|---|

| Name | Long/Short |

| Copper Future | Long |

| Wheat Future | Short |

| Sugar Future | Short |

| Silver Future | Long |

| Live Cattle Future | Long |

| FIXED INCOME | |

|---|---|

| Name | Long/Short |

| Japan 10-Year JGB Future | Short |

| U.S. 30-Year Treasury Bond Future | Short |

| U.S. 10-Year Treasury Bond Future | Long |

| iShares National Muni Bond ETF | Long |

| Australian 10-Year Bond Future | Short |

| EQUITIES | |

|---|---|

| Name | Long/Short |

| Arch Capital Group Ltd | Long |

| Comcast Corp | Short |

| Corteva Inc | Long |

| Bloom Energy Corp | Long |

| Motorola Solutions Inc | Short |

ETF holdings and macro asset class allocations are subject to change.

Currencies

Overview

A continued soft U.S. Dollar pushed international currencies higher last month, and the portfolio increased net long exposure to non-U.S. denominated currencies to the second-highest net position. In fact, allocations to international currencies have surpassed fixed income and now trail only U.S. equities in terms of influence over the portfolio.

Crypto exposure remained low after prices failed to rebound from the early-Q4 swoon.

Drivers

Despite lingering concerns around tariffs and foreign trade, falling oil and gasoline prices continue to ease inflationary pressures. As inflation stabilizes, it may become less of a dominant market driver, leaving greater room for relative growth, interest rate differentials, and country-specific factors to reassert themselves across global markets.

Commodities

Overview

Of the four major asset classes utilized by TFPN, commodities is currently the most hedged. Net longs in metals are nearly offset by net shorts in grains. Energies are emerging as a significant net long allocation as well. Livestock and other food products are mostly cancelling each other out after long running trends in 2024 and 2025.

Drivers

Wheat continues to trade near multi-year lows, with TFPN benefiting from its net short exposure, which remains the strategy’s largest commodity position.

The second-largest net position is in gold (long), which continues to enjoy a well-publicized run. Silver and copper remain strong in established uptrends as well.

Fixed Income

Overview

The biggest change in the portfolio lately is the leadership shift that has resulted in net long fixed income going from the most-influential asset class to number three of four. This change is mostly driven by a large increase in short positions among intermediate- to long-duration bond futures. Net long allocations to short-term interest rates also fell in December, further narrowing the portfolio’s net long bond exposure.

Drivers

Investors are closely watching signals from the Federal Reserve and its global peers, as markets debate the timing and pace of potential rate cuts. Softer inflation data in parts of Europe and slowing global growth have supported demand for bonds, while persistent fiscal deficits and heavy sovereign issuance are keeping upward pressure on yields in select markets. At the same time, policy divergence — particularly between the European Central Bank, which is viewed as closer to easing, and the Bank of Japan, which is gradually exiting ultra-easy policy — is driving currency-adjusted bond returns and cross-border capital flows. The result is a bond market environment shaped less by a single macro narrative and more by relative value, volatility, and shifting expectations.

Equities

Overview

U.S. equity exposure slightly increased in December, but due to large changes in fixed income it now represents by far the most influential portion of the portfolio. Continued strong consumer and employment indicators have fostered a favorable environment. Short positions still exist, even in this decidedly long-tilted portfolio, to buffer against sharp declines. However, the most beneficial scenario for TFPN would be a continuation of the current bull market.

Drivers

AZZ Inc. continues to hold a top spot for largest long equity position in the portfolio after rising 1.67% in December. Lumentum Holdings, a leading designer and manufacturer of optical components used in data centers, now occupies a top spot as well. Carpenter Technology and Western Digital also continue as large, long positions. On the short side, Motorola and Comcast have surpassed Canadian National Railway as the largest holding.

Portfolio Managers’ Note

TFPN closed the year with positive performance in seven of the final eight months, ending near its all-time high. The portfolio provided valuable non-correlation in a month when both bonds and stocks fell: the U.S. Aggregate Bond iShares Core ETF, which mirrors the performance of the Agg Index fell by almost 1%, and the S&P 500 Index declined 0.05%.

As 2026 begins, TFPN has already shown how its approach to outlier-hunting can help it benefit from difficult-to-forecast events, such as those occurring in Venezuela. On the day when markets reacted to the news of Nicolás Maduro’s arrest, the Volatility Index rose almost 3%, symbolizing investors nervously assimilating this new information. TFPN also rose, making new all-time highs and nearly matching the VIX’s daily return.

We often talk about trend following’s ability to benefit from things that have never happened before. While regime changes are not unprecedented, they are not exactly a common occurrence either. Research shows that few strategies can hold a candle to trend following when it comes to weathering such scenarios.

Taking a holistic view of TFPN, the portfolio is currently aligned with an environment characterized by constructive equity trends and a more accommodative monetary policy backdrop. Those conditions have also contributed to steadier-to-weaker U.S. dollar dynamics, creating a more constructive environment for international currencies. Commodities continue to display a wide range of behaviors, with strength in metals and weakness in grains. In our view, the portfolio is able to express these divergent trends in ways few other instruments can.

In our opinion, a diversified trend following vehicle like TFPN is due for a solid run after the trendless period of 2024 and early 2025. As Portfolio Managers, this is exciting. Regardless of where specific performance numbers fall in the month ahead, we are confident in TFPN’s ability to continue providing valuable non-correlation.

The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted.

For standardized performance please visit tfpnetf.com.

Let's Talk

If you’d like to learn more about TFPN, a next-generation liquid alternative