January 20, 2025

January 2025 Commentary Blueprint Chesapeake Multi-Asset Trend ETF

Home » Strategies » Exchange Traded Funds » Blueprint Chesapeake Multi-Asset Trend » TFPN Commentary

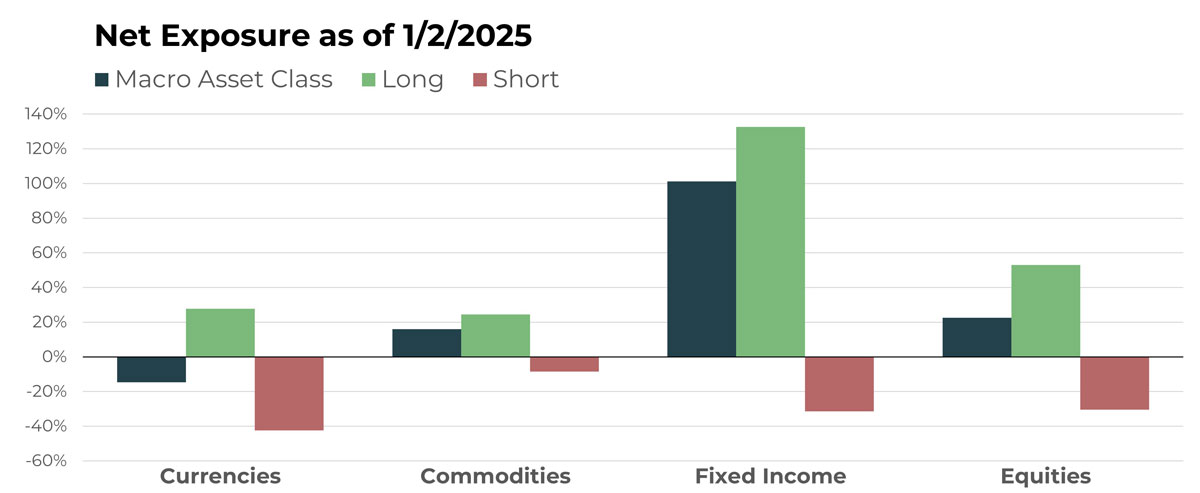

Portfolio Exposure At A Glance

Notable Holdings By Macro Asset Class

| CURRENCIES | |

|---|---|

| Name | Long/Short |

| Chinese Yuan/Canadian Dollar | Long |

| Chinese Yuan/Euro | Long |

| Phillippine Peso/U.S. Dollar | Short |

| British Pound/Swiss Franc | Long |

| British Pound/Japanese Yen | Long |

| COMMODITIES | |

|---|---|

| Name | Long/Short |

| Live Cattle Future | Long |

| Lead Future | Short |

| Gold Future | Long |

| Wheat Future | Short |

| Cocoa Future | Long |

| FIXED INCOME | |

|---|---|

| Name | Long/Short |

| U.S. 10-Year Note Future | Short |

| iShares Short-Term National Muni Bond ETF | Long |

| Australian 3-Year Bond Future | Short |

| SPDR High Yield Bond ETF | Long |

| Japan 10-Year Bond Future | Long |

| EQUITIES | |

|---|---|

| Name | Long/Short |

| TKO Group Holdings Inc | Long |

| Constellation Brands Inc | Short |

| Corteva Inc | Long |

| Shell plc | Short |

| Axon Enterprise Inc | Long |

ETF holdings and macro asset class allocations are subject to change.

Currencies

Overview

A strengthening U.S. Dollar has led to an increased net short currency position in the portfolio as the new year begins. At a high level, TFPN is approaching its highest net short exposure in currencies. Short positions in foreign currencies are among the most pronounced. This directional shift is both significant and widespread, encompassing a broad range of global currencies from developed and emerging economies alike, many of which are now experiencing downtrends.

Drivers

Among short currency positions, one of the largest is in the Singapore Dollar, which recently hit one-year lows and is approaching its lowest level since the fall of 2023. Another large short position is in the Canadian Dollar, influenced by recent news surrounding the resignation of Prime Minister Justin Trudeau. Meanwhile, cryptocurrencies remain notable long positions despite experiencing a slight pullback at the end of the year.

Commodities

Overview

Commodity exposure will remain slightly net long. Soft commodities, particularly cocoa, are by far the largest driver in this segment of the portfolio. Beyond softs, livestock represents the next most significant exposure, with a sizeable net long position. Meanwhile, grains, metals, and energies are more evenly balanced, with nearly equal long and short exposure.

Drivers

While a shift to rate cuts might be cause some to expect a spark in new commodity trends, the portfolio’s primary drivers remain steady. Soft commodities, led by cocoa, continue to dominate, while livestock holds a material long position. Energy and metals remain balanced, with competing forces like easing monetary policy and recession risks keeping trends muted. TFPN remains focused on the most consistent movers while staying patient for emerging opportunities in the commodity complex.

Fixed Income

Overview

Long fixed income remains the most significant position in the portfolio, though it has been reduced compared to previous months as we begin the year. Despite the sizable directional exposure, the sub-allocations are notably mixed. For example, U.S. government bonds are predominantly short, while European bonds maintain a net long exposure. This seemingly contradictory positioning seeks to provide effective hedging but highlights the choppy market behavior that has dampened profitable trends elsewhere in the portfolio.

Drivers

The largest allocation within TFPN’s fixed income universe is in ultra short-term duration instruments. Corporate, high-yield, and municipal ETFs also comprise a substantial portion of the long book. On the short side, the most significant positions remain focused on Australia, where both the 3-year and 10-year note futures hold large allocations.

Equities

Overview

Unsurprisingly, TFPN’s net long equity exposure decreased following December’s decline in stock prices, falling to roughly half the level from a month ago. While equities remain the second-most significant directional allocation after net long fixed income, the portfolio is now far more hedged than in recent months.

Drivers

In terms of individual exposures, MicroStrategy remains a significant single allocation within the equity portfolio. AZZ Inc continues to also hold a large long equity position in the portfolio. On the short side, Canadian National Railway represents a significant position. The stock fell over 9% in December, reaching its lowest level since 2020.

Portfolio Managers’ Note

A few years ago, one of TFPN’s sub-advisers wrote a white paper called “The 60/40 Problem” for two key reasons:

- To highlight the all-time highs in both equity and bond markets after years of easy monetary policy (i.e., declining and persistently low interest rates)

- To anticipate a potential correction of this phenomenon and explore its implications for investors relying on the traditional 60% equity and 40% bond portfolio

As fate would have it, 2022 turned the 60/40 problem into a 60/40 reality. Financial markets experienced a rare double blow, with simultaneous declines in equity and bond markets worldwide. Surging inflation and aggressive central bank rate hikes led investors to retreat toward short-term cash equivalents, such as Treasury bills. By the end of the year, every major asset class we track — domestic and international equities, global fixed income, and even gold — had finished in the red.

In periods of market crisis like this, systematic trend-following strategies often stand out. Designed to capitalize on outlier events, these strategies can thrive in conditions like the high downside correlation between equities and bonds seen in 2022. Many responded to these market dynamics by shorting both equities and bonds, generating positive performance in some cases. For investors whose traditional portfolios were broadly struggling, systematic trend-following strategies provided a valuable offset to those losses.

Fast forward to 2025, and we find ourselves referencing the 60/40 problem once again. Despite a decline in inflation and a resilient U.S. economy, the Federal Reserve has begun a rate-cutting cycle. Coupled with a potentially business-friendly U.S. presidential administration focused on deregulation, this environment could fuel another surge in economic activity — potentially reigniting inflation. Proposed tariffs may further stoke inflationary pressures.

If inflation rises again, we could see interest rates increase rather than decrease in 2025, reversing current expectations. In our view, such a shift has the potential to echo the asset performance patterns of 2022.

Let's Talk

If you’d like to learn more about TFPN, a next-generation liquid alternative