January 16, 2024

January 2024 Commentary Blueprint Chesapeake Multi-Asset Trend ETF

Home » Strategies » Exchange Traded Funds » Blueprint Chesapeake Multi-Asset Trend » TFPN Commentary

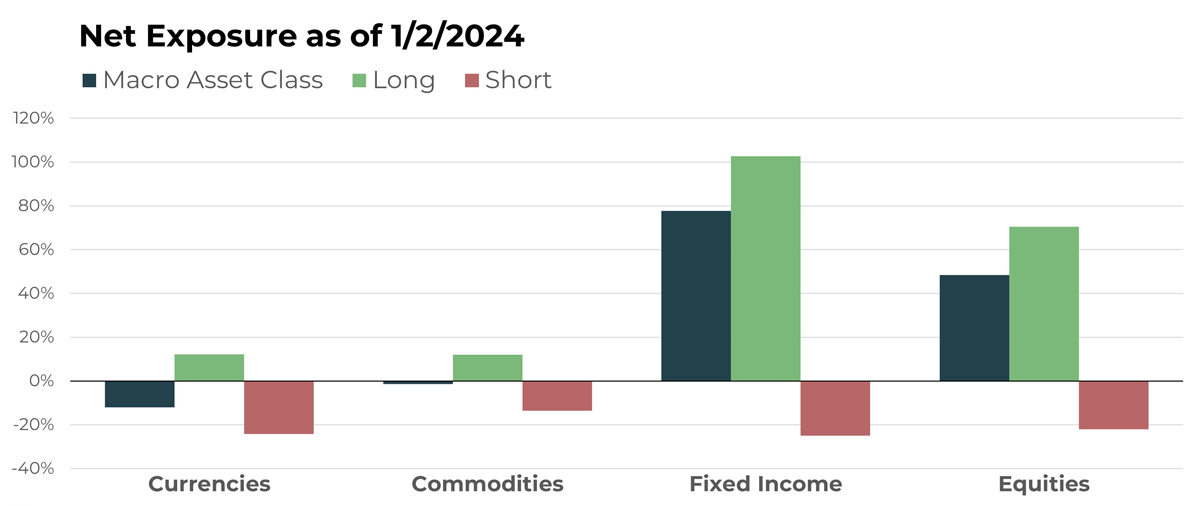

Portfolio Exposure At A Glance

Notable Holdings By Macro Asset Class

| CURRENCIES | |

|---|---|

| Name | Long/Short |

| Euro/British Pound | Short |

| U.S Dollar/South African Rand | Long |

| U.S. Dollar/Chinese Yuan | Long |

| Chinese Yuan/Japanese Yen | Short |

| Euro/Polish Zloty | Short |

| COMMODITIES | |

|---|---|

| Name | Long/Short |

| Wheat | Short |

| Frozen Orange Juice | Long |

| Sunflower Seed | Short |

| Cocoa | Long |

| Rough Rice | Long |

| FIXED INCOME | |

|---|---|

| Name | Long/Short |

| Australian Bank Bills | Short |

| iShares Short-Term National Muni Bond ETF | Long |

| U.S. 2-Year Note | Short |

| Vanguard Short-Term Corporate Bond ETF | Long |

| SPDR Portfolio High Yield Bond ETF | Long |

| EQUITIES | |

|---|---|

| Name | Long/Short |

| elf Beauty Inc | Long |

| Hormel Foods Corp | Short |

| Unilever | Short |

| AZZ Inc | Long |

| Coca-Cola Co | Short |

ETF holdings and macro asset class allocations are subject to change.

Currencies

Overview

The portfolio’s currency positions are approximately balanced between longs and shorts, with no major headline-worthy trends emerging currently.

The Euro/British Pound cross saw an upward retracement to its longer-term averages, which adversely affected the portfolio’s established short position in December.

Continuing as a holdover from previous months, the U.S. Dollar/Chinese Yuan cross remained relatively unchanged in December, thus failing to positively attribute to performance.

New additions to our notable currency holdings include long positions in the U.S. Dollar/South African Rand, as well as short positions in the Chinese Yuan/Japanese Yen and the Euro/Polish Zloty. The currency portfolio currently has significant exposure to the Chinese Yuan, as highlighted by the short Yuan/Yen position.

Additionally, the Euro/Polish Zloty position is particularly noteworthy, as it demonstrates the most dramatic trend among our holdings, making multi-year lows and falling approximately 7% in 2023.

Drivers

Among currencies, arguably the most noteworthy item is the economic status of China. GDP growth continues to be relatively subdued, which has been reflected in the performance of its benchmark stock indexes. The Shanghai Composite has retraced more than 20% from its recent 5-year high in 2021, and it is even further from its all-time high. Based on notable trends in the U.S. Dollar/Chinese Yuan (long) and Chinese Yuan/Japanese Yen (short), there appears to be a market sentiment in favor of Yuan weakness from multiple angles.

Commodities

Overview

In much the same way as the currency basket, TFPN’s commodity portfolio is currently balanced in terms of longs and shorts, with net exposure being almost zero.

Wheat continues to be a notable short position, despite its 10% increase in December. Even with the increase, it is still at lows not seen since the latter half of 2020 before the commodity rally of 2021 and 2022.

The portfolio’s long position in cocoa futures continues to produce positive results, as it closed 2023 up more than 60%. Trades like cocoa, and orange juice futures as another example, represent classic examples of the benefits of a trend-following process. While the rest of portfolio may experience a series of small losses and uneventful trades, moves like that of cocoa and orange juice can seemingly develop out of nowhere to produce positive results.

Drivers

With recent Federal Reserve announcements indicating an end to rate increases, attention among commodity market participants is likely to remain on the timing of potential rate cuts. Markets often quickly discount news, shifting focus to future developments. Therefore, it’s possible that some, if not much, of the pricing surrounding the anticipated first rate cuts has already been factored in. Should there be a delay in these cuts, it could prove challenging for those holding long positions in commodities and beneficial for short positions. As previously mentioned, our portfolio maintains a balanced stance, reflecting prevailing trends. We will commit to a dominant side, either long or short, only when market conditions and price movements clearly dictate such a decision.

Fixed Income

Overview

Since TFPN’s inception, no sector exposure has been as prominent in the portfolio as fixed income shorts. As recently as early December, the ETF was still well net short. Around then, the portfolio was beginning the transition to neutral. With central banks offering increasingly dovish rhetoric, TFPN is now net long fixed income, with increasing exposure to longer-duration instruments. In fact, the ETF’s largest absolute exposure now is to fixed income.

This illustrates the noncorrelative nature of TFPN. The ETF is able to take and hold short positions in a particular asset class, then fairly quickly pivot in a systematic, unemotional way. In this way, TFPN is much less susceptible to biases and risks that other strategies bear, in our opinion.

Drivers

Few assets are more closely tied to monetary policy than fixed income, and so the actions of central banks will almost always be the primary driver of fixed income prices. During certain periods, like now, this is particularly true and policy direction tends to persist once it is set. Likewise, once policy direction pivots, it tends to stick. In other words, historically policymakers don’t raise, lower, raise, and then lower interest rates. They instead will raise, raise, raise, and then cut, cut, cut…and so on. That said, the market doesn’t always march exactly to the beat of the monetary policy drum, so it is possible that trends could be inconsistent until sentiment becomes unified.

At this stage of the trend cycle, as we are taking on new long positions, any losses would be especially small since few long profits have been generated yet. When and if rate cuts commence, TFPN is now well-positioned to take advantage.

Equities

Overview

A visual of the portfolio right now would look like a barbell: burgeoning long fixed income trends on one side, a growing consensus of long stocks on the other side, and a generally hedged portfolio of commodities and currencies in between.

Not much has changed within the portfolio’s notable equity holdings, other than the increase in net exposure to the long side. Similar middle capitalization size and growth stocks continue to make up the largest long allocations, with more value-oriented names comprising the short book.

Obviously, the long side produced a better attribution in December and is positioned to do the same to start 2024. TFPN’s most notable long equity holding continues to be elf Beauty, which followed up its 27% November return by making another all-time high in December when it increased more than 22%. Another major long trade, AZZ Inc, produced an 18% return for December.

It is also important to note that notable shorts like Hormel and Unilever were relatively flat in December, doing little to offset TFPN’s long exposure but offering some protection against an end-of-year decline.

Drivers

With the holidays and Santa Claus rallies over, the key focus within equity markets will likely go back to earnings and economics. The same monetary policy pivot that boosted bonds has done so for equities as well. Descending inflation and continued steady employment should provide an environment for positive equity returns as long as individual business results do nothing contrary. Additionally, the presence of an election year could introduce volatility, but there is little in the historical record to cause an expectation of any outsized impact.

Let's Talk

If you’d like to learn more about TFPN, a next-generation liquid alternative