February 11, 2026

February 2026 Commentary Blueprint Chesapeake Multi-Asset Trend ETF

Home » Strategies » Exchange Traded Funds » Blueprint Chesapeake Multi-Asset Trend » TFPN Commentary

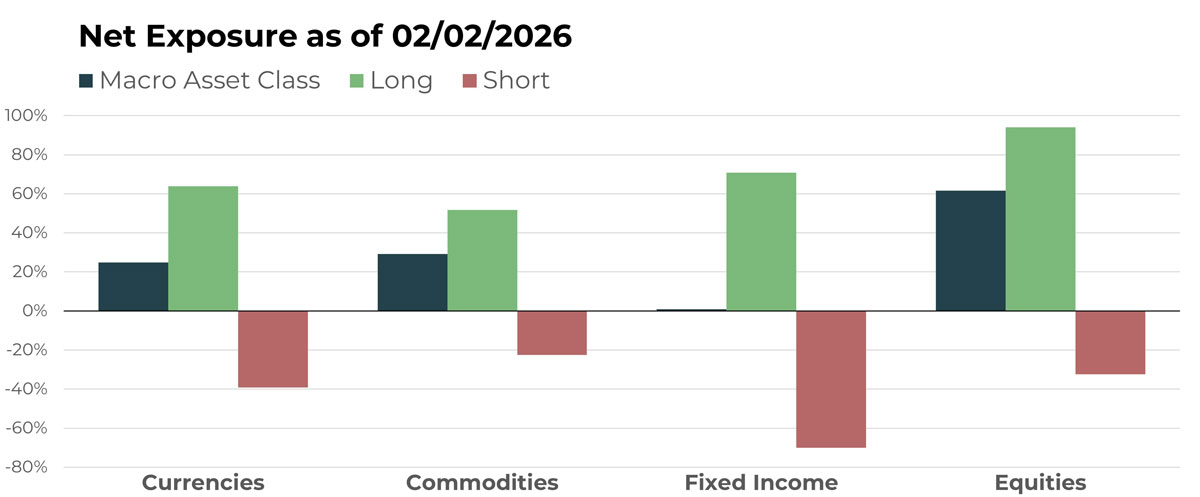

Portfolio Exposure At A Glance

Notable Holdings By Macro Asset Class

| CURRENCIES | |

|---|---|

| Name | Long/Short |

| Indian Rupee/U.S. Dollar | Short |

| Polish Zloty/Euro | Long |

| China Yuan/U.S. Dollar | Long |

| Euro/Australian Dollar | Short |

| Australian Dollar/U.S. Dollar | Long |

| COMMODITIES | |

|---|---|

| Name | Long/Short |

| Copper Future | Long |

| Cotton Future | Short |

| Lumber Future | Short |

| Silver Future | Long |

| Gold Future | Long |

| FIXED INCOME | |

|---|---|

| Name | Long/Short |

| Japan 10-Year JGB Future | Short |

| U.S. 30-Year Treasury Bond Future | Short |

| U.S. 10-Year Treasury Bond Future | Long |

| Canadian 2-Year Bond Future | Long |

| Australian 10-Year Bond Future | Short |

| EQUITIES | |

|---|---|

| Name | Long/Short |

| Bank of Nova Scotia | Long |

| Aptargroup Inc | Short |

| Kratos Defense | Long |

| Rio Tinto PLC | Long |

| Netflix Inc | Short |

ETF holdings and macro asset class allocations are subject to change.

Currencies

Overview

The U.S. Dollar reached a multi-year low in January, resulting in an increase in the portfolio’s exposure to international currencies. Of the nearly 30 foreign currency positions, all but a handful are net long versus the U.S. Dollar. Strength has been particularly evident across the Asia-Pacific region, as well as in Nordic and Eastern European currencies.

Crypto exposure continued to decline and is was nearly flat as February began.

Drivers

Several international currencies remain in established uptrends. The Chinese Yuan continues to strengthen following its April 2025 low, and the portfolio maintains multiple long positions versus different counterparts, including the U.S. Dollar. The Australian Dollar has also extended its advance and is trading near its highest level in more than three years. Elsewhere, the Czech Koruna and Norwegian Krone remain strong on a relative basis versus the U.S. Dollar. Taken together, these trends reflect persistent relative strength across select international currency markets.

Commodities

Overview

Net commodity exposure remained largely unchanged through January, with long positions in metals continuing to offset short positions in grains. While these positions reside within the same asset class, they are driven by distinct market forces and do not function as direct hedges against one another. This structure reflects the strategy’s emphasis on diversification and non-correlated return streams rather than directional bets within a single market.

Drivers

Gold and copper remain the largest long positions within commodities. Gold experienced notable volatility late in the month, declining sharply on the final trading day of January, yet still finished the month higher overall. Such price behavior is consistent with assets experiencing strong trends.

The cattle complex also regained momentum after a period of retracement in October and November.

On the short side, wheat continues as the largest commodity position, with the portfolio benefiting as March futures declined during January.

Corn represents the next-largest short position and also moved lower, in line with its prevailing trend.

Fixed Income

Overview

Fixed income exposure continued to decline in January, leaving the asset class close to net neutral, with long and short positions nearly balanced. Short-term bond exposure was reduced further as markets reassessed the near-term path of monetary policy. February began with a modest net long fixed income position, though overall exposure remains flexible.

Drivers

Global bond markets have remained uneven as investors respond to differing central bank policies. In the U.S., longer-duration Treasury prices have softened due to the evolution of policy normalization expectations. In Europe, bond prices have strengthened amid easing inflation pressures, while Japan continues to diverge as markets adjust to gradual policy changes. In the U.K., Gilt prices have fluctuated alongside incoming economic data. These cross currents continue to create a dynamic environment for relative fixed income positioning.

Equities

Overview

U.S. equities experienced modest weakness early in January before recovering and finishing the month higher. Equities remain the portfolio’s most influential asset class, supported by both long and short positions designed to capture sustained trends while managing downside risk.

Drivers

Western Digital, already a meaningful long position, became the portfolio’s largest equity holding following a strong January advance. AZZ Inc. also posted gains and remains a significant allocation. Lumentum Holdings continued its upward trend as well.

On the short side, Comcast detracted from broader equity strength, contributing positively to portfolio performance as its decline coincided with advances in several long holdings.

Portfolio Managers’ Note

TFPN opened 2026 by benefiting from well-established trends across several major positions, resulting in its strongest monthly return since inception, with performance exceeding 10% in January. The month reflected the strategy’s ability to participate across multiple, unrelated trends simultaneously, including:

- Long U.S. equities, including mid- and small-cap exposure

- Short U.S. Dollar exposure through long international currencies

- Long Asia-Pacific currencies

- Long metals

- Short grain markets

Individually, each of these trends could be difficult to capture using discretionary or forecast-driven approaches. Capturing several at once — without requiring advance knowledge of their timing or magnitude — is central to the design of the strategy. TFPN does not seek to anticipate market outcomes; instead, it responds to observable price behavior as trends emerge and persist.

This approach has been consistent over time. While the specific drivers of performance naturally change from month to month, the underlying investing process does not. As noted in last month’s update, we believed the portfolio was positioned to benefit if trends reasserted themselves following a prolonged, choppier period — and January provided an example of how that process can translate into results when multiple trends align.

As always, the focus remains on maintaining discipline and consistency rather than emphasizing any single outcome. TFPN’s strategy continues to be providing diversified, non-correlated exposure that adapts as market conditions evolve.

The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted.

For standardized performance please visit tfpnetf.com.

Let's Talk

If you’d like to learn more about TFPN, a next-generation liquid alternative