February 14, 2025

February 2025 Commentary Blueprint Chesapeake Multi-Asset Trend ETF

Home » Strategies » Exchange Traded Funds » Blueprint Chesapeake Multi-Asset Trend » TFPN Commentary

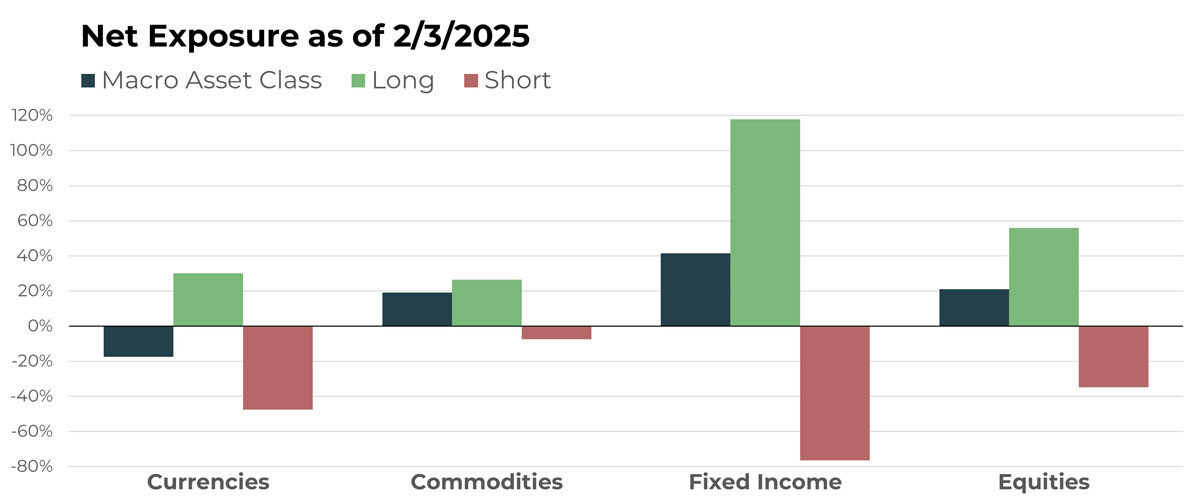

Portfolio Exposure At A Glance

Notable Holdings By Macro Asset Class

| CURRENCIES | |

|---|---|

| Name | Long/Short |

| Chinese Yuan/Canadian Dollar | Long |

| Chinese Yuan/Euro | Long |

| Polish Zloty/Euro | Long |

| Indonesian Rupiahs/U.S. Dollar | Short |

| Colombian Peso/U.S. Dollar | Short |

| COMMODITIES | |

|---|---|

| Name | Long/Short |

| Live Cattle Future | Long |

| Rough Rice Future | Short |

| White Sugar Future | Short |

| Yellow Maize Future | Long |

| Cocoa Future | Long |

| FIXED INCOME | |

|---|---|

| Name | Long/Short |

| U.S. 2-Year Note Future | Short |

| iShares Short-Term National Muni Bond ETF | Long |

| Australian 3-Year Bond Future | Short |

| Vanguard Short-Term Corp Bond ETF | Long |

| Japan 10-Year Bond Future | Short |

| EQUITIES | |

|---|---|

| Name | Long/Short |

| TKO Group Holdings Inc | Long |

| PepsiCo Inc | Short |

| MicroStrategy Inc | Long |

| Canadian National Railway Co | Short |

| AZZ Inc | Long |

ETF holdings and macro asset class allocations are subject to change.

Currencies

Overview

TFPN’s net short exposure to foreign currencies remains largely unchanged from the previous month. A strong U.S. economy, coupled with stable interest rates, continues to support the U.S. Dollar, keeping other currencies under pressure. The ongoing threat of tariffs — whether real or a negotiation tactic — has likely contributed to this trend.

Drivers

The dominant theme remains positioning against the U.S. Dollar, with a nearly 10-to-1 ratio of short foreign currencies versus the U.S. Dollar. Large short positions include the Singapore Dollar and Canadian Dollar, while a significant long position against the U.S. Dollar is the Israeli Shekel.

Looking beyond the U.S. Dollar, key foreign currency cross-rates include long positions in the Chinese Yuan against both the Euro and Canadian Dollar, as well as a long Australian Dollar versus short New Zealand Dollar position.

Commodities

Overview

TFPN’s commodity allocations remain net long, with soft commodities representing the largest portion. Livestock futures hold a unanimously long bias, while grains, metals, and energy positions are mixed and currently less significant.

Drivers

Within the softs segment, cocoa and coffee continue to be dominant positions. Cocoa took a breather in January, but coffee surged more than 18%. Among livestock, cattle futures have been one of the strongest contributors, with all three major cattle contracts posting gains in January.

Gold remains another standout, continuing its positive trend and contributing meaningfully to returns.

Fixed Income

Overview

Last month, we highlighted that while fixed income allocations were sizably net long, a deeper look revealed a noticeably mixed picture. For February, shorts are now closer to matching longs, but that has done little to clear up the view on trends in this segment.

Government bonds of meaningful duration remain almost universally short, by more than a 4-to-1 ratio. This is offset by a heavy long tilt toward ultra-short-duration instruments, along with a material net long allocation to corporate and municipal bonds, which has remained mostly sideways during early 2025.

Drivers

Significant positions remain focused on Australia, where both the 3-year and 10-year Note futures hold large short allocations. U.S. Treasury futures also remain short across the curve, from the 2-year all the way to the 30-year — reinforcing the embedded sentiment that rates will stay higher for longer.

Among non-government bond instruments, short-duration municipals and TIPS are currently big drivers.

Equities

Overview

Stocks continue to hold a net long position, though the gap between longs and shorts has narrowed. The overall allocation to equities is now more in line with the other major asset classes.

Drivers

MicroStrategy remains a large long equity holding, followed by AZZ Inc. Newcomer TKO Group Holdings also made an impact, climbing more than 9% in January.

On the short side, Canadian National Railway continues to be a large position. Its 9% decline in December was followed by a 3% increase in January, which demonstrates the benefit of TFPN’s long/short equity approach.

Portfolio Managers’ Note

As always, it’s crucial to properly assess TFPN’s role within a broader portfolio and measure its performance accordingly.

In our view, for financial advisors with the independent spirit to ignore mainstream portfolio views and file financial news exactly where it belongs (in the waste bin), TFPN remains an excellent standalone investment or portfolio diversifier — one that prioritizes process over outcome with the long game in mind. The underlying strategy began trading in 1994 as a limited partnership, and the principles that propelled it to this time-tested longevity for decades continue to be followed religiously and executed without emotion.

This period of sideways movement is just that — a phase. Not the first, and certainly not the last. The real question shouldn’t be, “Why isn’t the fund working?” but rather one or all of these:

- Should we abandon part of trend following to benefit from this one specific market environment?

- Should we ignore risk and remove stop losses?

- Should we stop riding winners?

- Should we abandon systematic position sizing?

- Should we start predicting instead of reacting?

The answer to each question is: Of course not! These are essentially rhetorical questions.

For clients who are unwilling or unable to go against the status quo but want to gain measured exposure to diversification in their portfolios, the key is keeping the big picture in mind. One of the primary benefits of an unconstrained trend-following strategy is its non-correlation to traditional assets. It can perform well when stocks and bonds do — but it doesn’t have to. More importantly, when a market outlier event occurs, it provides a valuable hedge — the same way a well-structured insurance policy does.

Abandoning a time-tested process to chase a specific outcome is a terrible idea. Instead, we remain committed to the strategy, knowing that trends will return, and when they do, we think they will once again validate the timeless design of this approach.

In the meantime, we appreciate an environment that has been conducive to keeping traditional portfolios on track and allowing investors to reach their goals. The only question is: Will they have the discipline to stick with what works?

Let's Talk

If you’d like to learn more about TFPN, a next-generation liquid alternative