February 16, 2024

February 2024 Commentary Blueprint Chesapeake Multi-Asset Trend ETF

Home » Strategies » Exchange Traded Funds » Blueprint Chesapeake Multi-Asset Trend » TFPN Commentary

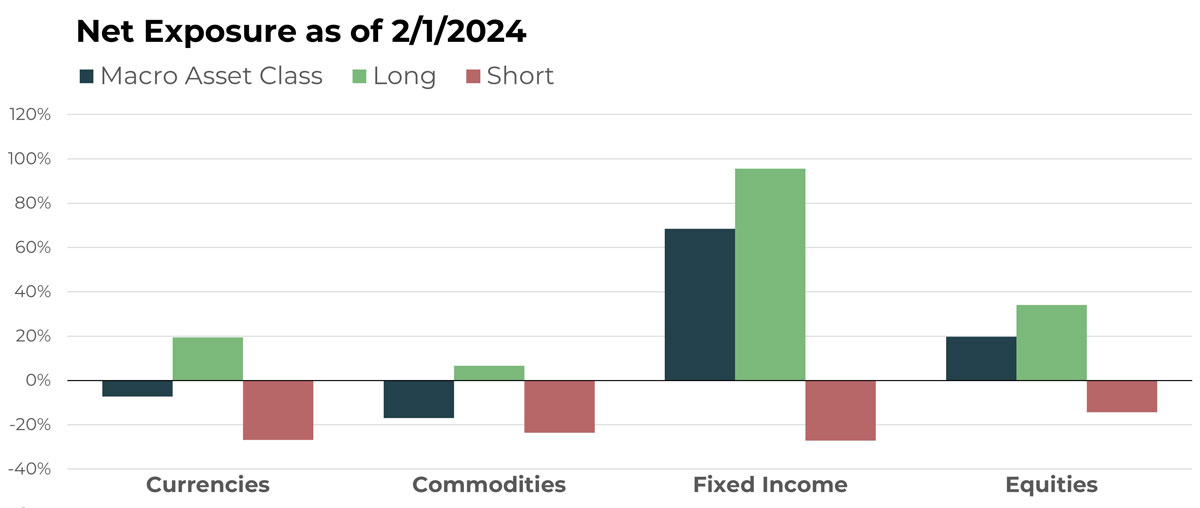

Portfolio Exposure At A Glance

Notable Holdings By Macro Asset Class

| CURRENCIES | |

|---|---|

| Name | Long/Short |

| Euro/British Pound | Short |

| Chilean Peso/U.S. Dollar | Long |

| U.S. Dollar/Chinese Yuan | Long |

| Canadian Dollar/New Zealand Dollar | Long |

| Euro/Swiss Franc | Short |

| COMMODITIES | |

|---|---|

| Name | Long/Short |

| Wheat Future | Short |

| Frozen Orange Juice Future | Long |

| Copper Future | Short |

| Crude Oil Future | Long |

| Cocoa Future | Long |

| FIXED INCOME | |

|---|---|

| Name | Long/Short |

| U.S. 2-Year Note Future | Short |

| iShares Short-Term National Muni Bond ETF | Long |

| U.S. 10-Year Note Future | Short |

| iShares 0-5 Year TIPS Bond ETF | Long |

| Japan 10-Year Bond Future | Long |

| EQUITIES | |

|---|---|

| Name | Long/Short |

| elf Beauty Inc | Long |

| Exxon Mobil Corp | Short |

| Alpha Metallurgical Resources Inc | Long |

| Boise Cascade Co | Long |

| Keurig Dr Pepper Inc | Short |

ETF holdings and macro asset class allocations are subject to change.

Currencies

Overview

The currency portfolio inside TFPN is exemplary of our commitment to broad exposure and avoiding baskets or indexes when appropriate. As a result, the portfolio is comprised of cross-rate exposures and digital currencies that reflect a wide spectrum of exposures and drivers. For example, as of the end of January, the portfolio consisted of around 50 currency positions, long and short. Positions that demonstrate the broad range included long Bitcoin and Ethereum futures, short Australian Dollars against Canadian Dollars, and long U.S. Dollar against the Thai Baht.

Diving deeper, on the short side, two notable positions are the Euro versus the British Pound and the Euro versus the Swiss Franc. Attentive readers of this monthly commentary will recall that these two allocations have been discussed before. Certainly, the Euro’s weakness is much more pronounced in terms of the Swiss Franc, with a downtrend that easily stretches back to 2021. Versus the British Pound, the Euro’s decline is less pronounced, but still meaningful, as prices challenge their one-year low.

In terms of long positions, recent price movements have been less favorable. Notable holdings in the Chilean Peso versus the U.S. Dollar and the U.S. Dollar versus the Chinese Yuan failed to move higher during the last 30 days. However, the Canadian Dollar versus New Zealand Dollar produced a return of just under 2% in January, which helped offset losses in the other, aforementioned longs.

Drivers

Strong payroll data in the U.S. encouraged the Federal Reserve to temper expectations among investors for interest rate cuts and boosted the U.S. Dollar. While the U.S. central bank remains relatively balanced, it is dovish compared to recent comments by the Bank of England (BoE). In a recent meeting among the BoE monetary policymakers, rates were held steady, but the rhetoric was decidedly tilted toward continuing to combat inflation.

Commodities

Overview

The portfolio’s net short exposure increased as we moved into February, with wheat and copper being two notable positions. The former is trading at a one-year low while the latter continues to trade in a range since mid-November.

On the long side, orange juice bounced back to close January, finishing the month positive after rising almost 15% in the last several days of trading. Likewise, cocoa closed the month on a tear, increasing nearly 15% in the first month of 2024.

Drivers

Perhaps as expected, the delay in rate cut expectations has been bearish news for some commodity markets, resulting in TFPN shifting in a more negative direction with more shorts. However, even with this pressure, the force of trends – particularly among entrenched markets like OJ and cocoa – remains strong enough to overcome whatever the fundamental factors may say. This, among other reasons, is why we favor trends over news.

Fixed Income

Overview

The portfolio experienced a small reduction in its net long exposure as we moved into February. Short exposures were basically unchanged, but long exposure decreased slightly as markets retraced or moved sideways depending on duration. The result is a series of positions still primed to benefit from interest rate cuts, should they occur.

It is natural in the course of changing from net short to net long, as the portfolio has done recently, that the markets may experience choppy conditions. However, since TFPN is designed to take small losses and ride winners, these consolidations are expected to pose little threat, in our opinion.

Drivers

Fixed income markets displayed a wide variation in returns in January, as the markets reacted to the leveling of expectations related to future interest rate cuts. Shorter-duration bonds tended to trade higher, particularly at the close of January, while longer-duration bonds generally ended lower for the month. All of this was likely in reaction to the aforementioned central bank commentary and diluting of interest rate cut expectations. In the context of the larger interest rate cycle, we likely remain in the same place we have been for the last two months, and until the monetary policymakers commit, choppy conditions in fixed income markets could persist.

Equities

Overview

Equity exposure remains tilted toward the long side as we progress through February, but the tilt is less pronounced compared to our last update. Alpha Metallurgical Resource (AMR, +18% in Jan) and Boise Cascade Co (BCC, +5% in Jan) join elf Beauty (ELF, +11% in Jan) as notable long positions in the portfolio. Among shorts, Exxon Mobil (XOM,; +3% in Jan) joins longstanding position Keurig Dr Pepper (KDP, -6% in Jan).

Drivers

While the mood has been dampened a bit among investors due to the Fed’s tone on rates, performance among most U.S. segments remains positive to start the year, led once again by tech and growth. The notable domestic exceptions are mid and small caps, along with interest-rate-sensitive securities such as REITS, which finished lower in January. Continuing a theme from 2023, international stocks also underperformed, with both developed and emerging markets decreasing for the month.

Despite the uncertainty about rates, the economy remains strong by any objective stance. For the most part, earnings have also been positive, which helps create a solid foundation for positive equity market returns.

On the technical side, new highs in the S&P 500 Index typically provide a favorable environment. Given that it’s been a couple years since the last new high, it is easy for us to see the positive equity market trends continuing. The portfolio is positioned accordingly but ready to switch gears if needed.

Portfolio Managers’ Note

Like life, market trends are rarely straight in one direction. Rather, they ebb and flow from positive to negative in the short term toward an overall, long-term end.

The portfolio’s current high-level stance of short commodities, short rates (long bonds), and long stocks is, in our view, an appropriate reflection of what is happening in the markets at large. We believe the current positioning also illustrates how TFPN can complement a traditional portfolio.

TFPN has, thus far, successfully navigated the trend changes in fixed income and commodities, while benefiting from a generally long stance in equities. In our view, TFPN’s adaptability may benefit traditional portfolios that have long-only equity exposure and can, over time, positively attribute on both the risk and return sides.

Let's Talk

If you’d like to learn more about TFPN, a next-generation liquid alternative