December 16, 2025

December 2025 Commentary Blueprint Chesapeake Multi-Asset Trend ETF

Home » Strategies » Exchange Traded Funds » Blueprint Chesapeake Multi-Asset Trend » TFPN Commentary

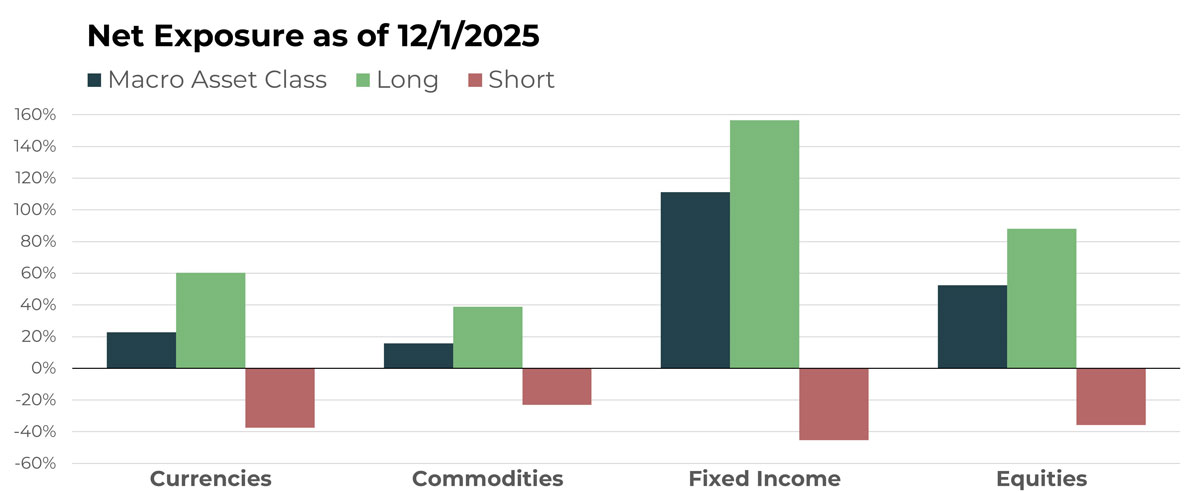

Portfolio Exposure At A Glance

Notable Holdings By Macro Asset Class

| CURRENCIES | |

|---|---|

| Name | Long/Short |

| Indian Rupee/U.S. Dollar | Short |

| Australian Dollar/U.S. Dollar | Long |

| China Renminbi/Euro | Short |

| Australian Dollar/Canadian Dollar | Long |

| Korean Won/U.S. Dollar | Short |

| COMMODITIES | |

|---|---|

| Name | Long/Short |

| Soybean Future | Long |

| Lead Future | Short |

| Oats Future | Short |

| Aluminum Future | Long |

| Coffee Future | Long |

| FIXED INCOME | |

|---|---|

| Name | Long/Short |

| Japan 10-Year JGB Future | Short |

| US 2-Year Treasury Note Future | Short |

| US 3-Year Treasury Note Future | Long |

| iShares MBS ETF | Long |

| Australian 10-Year Bond Future | Long |

| EQUITIES | |

|---|---|

| Name | Long/Short |

| Zscaler Inc | Long |

| Kimberly-Clark Corp | Short |

| Western Digital Corp | Long |

| Realty Income Corp | Long |

| Automatic Data Processing | Short |

ETF holdings and macro asset class allocations are subject to change.

Currencies

Overview

The U.S. Dollar continued its series of higher local lows in November as it recovered from its summer low. The rally was enough to nearly halve the net long position to international currencies.

Exposure to crypto assets also continued to decline as prices retreated. In fact, allocations to crypto are now about a tenth of what they were during the summer rally.

Drivers

The re-opening of the U.S. government did little to alter the recent trajectory of the U.S. Dollar, at least for the time being. Leading up to the December Fed meeting, consensus was building for another interest rate cut, but inflation concerns continued to muddy the waters and is keeping the USD generally higher.

Explanations vary for the recent crypto pullback, but in general sentiment has become negative. It will be interesting to see if this is a symptom of a bigger problem – and more declines to come – or represents a buying opportunity for those brave enough to catch the falling knife.

Commodities

Overview

Within the commodities segment, metals were once again the biggest movers with its net long allocation increasing by more than 40% heading into December. Grains and food/fiber remain net short. Interestingly, the six energy futures positions are all long at the moment. However, the once large long position in livestock futures has now dwindled to a roughly neutral position, with shorts almost equaling longs. The overall result is an increase in the net long commodity position driven almost exclusively by the change in metals.

Drivers

Gold remains a large single position and tends to get all the headlines, but the combined long positions in aluminum and copper outweigh gold in the portfolio. The combined net long exposure to feeder and live cattle also represents a significant allocation. All of the above do not match TFPN’s largest commodity holding: wheat (short). This holding started December on a positive note after three down months in the last four.

Fixed Income

Overview

Overall net long exposure to fixed income decreased in November but remains the largest segment in the portfolio. Intermediate- and long-duration bond futures, which have seen their long allocations increase consistently in recent months, experienced a slight decline. Short-term bond futures continued their transition toward less long heavy. Fixed income ETFs, which comprise the portfolio’s exposure to instruments like municipals and corporate bonds, remain net long but with a small decrease in allocation.

Drivers

It is likely the same factors that have kept the U.S. Dollar moving higher have also influenced the pause in rising duration in the portfolio. The growing consensus in November and early December of an interest rate cut supported bond futures prices enough to keep most trends intact, but not enough to fend off something of a retracement. Overall, bond trends remain strong on the long side and as a result the portfolio continues to have significant exposure here.

Equities

Overview

Overall, U.S. equities experienced very little exposure change in November. It remains the second-largest asset class allocation, surpassing commodities and currencies combined. In fact, when adjusting for the volatility of the underlying holdings, one could easily argue that net long equities is the most-meaningful allocation in the portfolio. In other words, while fixed income has the most money allocated to it, it is unlikely to drive performance quite like equities or even perhaps commodities given the disparity in volatility between the individual holdings of each asset.

Drivers

After a brief fall from the top, AZZ Inc. regains its spot as the largest equity holding at the start of December. Carpenter Technology and Western Digital also continue as large long positions. Strategy Inc. will be noticeably absent, as its fall has generated sell signals in the portfolio.

On the short side, Canadian National Railway is once again the largest holding, with others also making up material allocations, such as Ingredion Inc., Procter & Gamble, and Waste.

Portfolio Managers’ Note

The increase in metals prices was not enough to offset the pause in fixed income and bonds, as TFPN experienced its first monthly decrease in seven months. Despite the slight decrease, it remains positive for the year and within striking distance of new all-time highs. Potential tailwinds for the current month include:

- December is historically an above-average period for stocks

- TFPN’s current positioning

- Any news reinforcing lower interest rates ahead

The case of recent crypto performance highlights an important facet of TFPN’s strategy and serves as a lesson for investors:

- There are almost always news headlines meant to explain an asset’s rise or fall, but in the case of this decline, a smoking gun has not yet emerged. And yet, just as quickly as Bitcoin fell more than 30% from its early-October high, it recovered a bit as December began – all without any straightforward explanation from pundits.

- TFPN’s systematic investing approach allows the portfolio to easily incorporate newer and/or riskier assets due to its emphasis on prudent position sizing and its use of stop losses. TFPN can participate in rises and exit during sustained declines. No explanation is needed for said rise or fall.

Sometimes waiting for an explanation to arise before acting can be devastating to the benefits of compounding, as assets tend to take a stairs-up, elevator-down pattern. This has been the case for many crypto instruments.

The beauty of being systematic is the ability to think clearly and act decisively – there’s no emotional attached. Mind you it’s not a perfect system 100% of the time, but the bet is that a series of consistent actions will beat sporadically great results. It’s the mantra, “Consistently good beats occasionally great.”

TFPN’s ability to add new instruments also helps fend off one of the questions and criticisms that a systematic, trend following program often receives. Namely, skeptics will worry about a strategy ceasing to work or no longer being relevant. Taking timeless principles such as position sizing, riding winners, and selling losses quickly – combined with utilizing a wide array of old and new assets – is a clever way to combat that concern, in our opinion.

So, as we conclude our final note of 2025, we thank our current financial advisor partners and look forward to serving you and others in 2026.

The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted.

For standardized performance please visit tfpnetf.com.

Let's Talk

If you’d like to learn more about TFPN, a next-generation liquid alternative