December 18, 2023

December 2023 Commentary Blueprint Chesapeake Multi-Asset Trend ETF

Home » Strategies » Exchange Traded Funds » Blueprint Chesapeake Multi-Asset Trend » TFPN Commentary

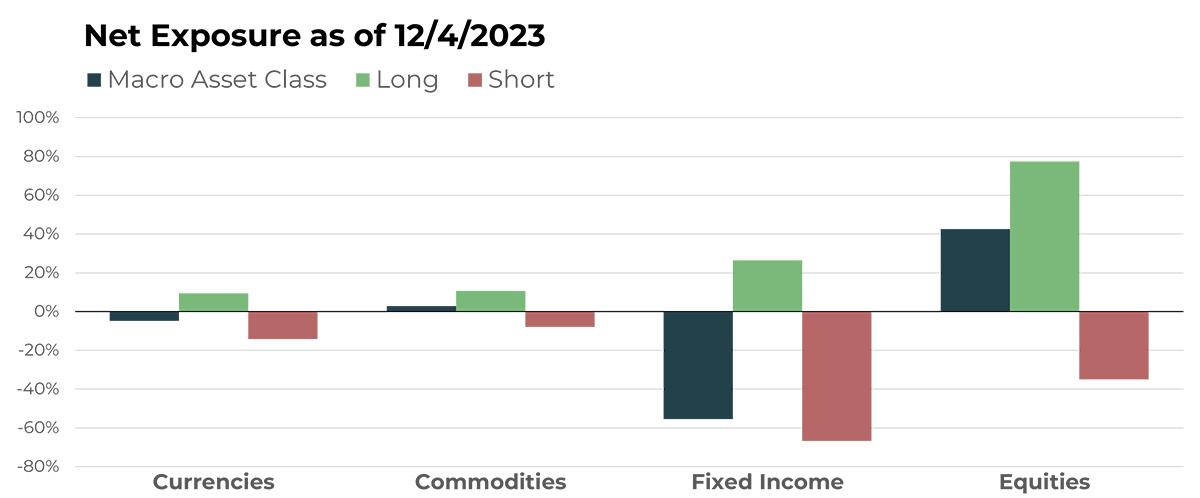

Portfolio Exposure At A Glance

Notable Holdings By Macro Asset Class

| CURRENCIES | |

|---|---|

| Name | Long/Short |

| Euro/British Pound Future | Short |

| U.S. Dollar/Chinese Yuan Future | Long |

| Euro/Swiss Franc Future | Short |

| Canadian Dollar Future | Short |

| Euro/Australian Dollar Future | Long |

| COMMODITIES | |

|---|---|

| Name | Long/Short |

| Wheat Future | Short |

| Frozen Orange Juice Future | Long |

| Copper Future | Short |

| Cocoa Future | Long |

| White Sugar Future | Long |

| FIXED INCOME | |

|---|---|

| Name | Long/Short |

| 3-Month Euribor Future | Short |

| iShares Short-Term National Muni Bond ETF | Long |

| U.S. 5-Year Note Future | Short |

| Vanguard Short-Term Corporate Bond Idx Fd ETF | Long |

| iShares TIPS Bond ETF | Long |

| EQUITIES | |

|---|---|

| Name | Long/Short |

| elf Beauty Inc | Long |

| Coca-Cola | Short |

| AZZ Inc | Long |

| Boise Cascade Co | Long |

| Johnson & Johnson | Short |

ETF holdings and macro asset class allocations are subject to change.

Currencies

Overview

In November, TFPN’s sustained short positions in the Euro/British Pound and the Euro/Swiss Franc crosses yielded positive portfolio attribution due to consistent declines throughout the month. Both positions continued their downward trend into December, now trading near their one-year lows.

The U.S. Dollar/Chinese Yuan cross, a longer-term strategy holding, performed less well in November and finished down 3.12% after three consecutive up months. It remained in the portfolio as we entered December.

A couple newcomers to the notable currency holdings list are the short of the Canadian Dollar and long of the Euro/Australian Dollar cross. The former broke out to the downside to close October but has since retraced more than 2%. It could be in line for a small loss in the portfolio, but this underscores TFPN’s deep commitment to responsible position sizing as it seeks outlier trades. The Euro/Australian Dollar pair has been climbing steadily during the last year and, despite a slight November pullback of just over 1%, continues its overall uptrend.

Drivers

The predominant driver of asset trends in November was the growing consensus shifting from monetary tightening to easing, a stance contrasted by U.S. Fed Chairman Jerome Powell’s recent comments. He emphasized maintaining higher interest rates until inflation is well-controlled. This reminder of central banks’ dedication to price stability led to a moderation in some long-standing trends. The portfolio’s diverse mix of long and short positions in currencies provides a hedged stance amidst these evolving trends until the timing and direction of the next interest rate movement is clearer.

Commodities

Overview

TFPN’s commodity portfolio saw significant changes but maintained a slightly net long position. Frozen orange juice, cocoa, and sugar have replaced live cattle and oil as key long positions. Wheat and copper have emerged as notable short positions, taking the place of commodities like lumber. After producing some of the best trends over the last few years while riding the inflation wave upwards, commodities are naturally facing an inflection point. Some are beginning to decline and others are holding on to established trends, for now.

Drivers

Last month we highlighted how the perceived end of a trend can be complicated by a quick re-establishment of the status quo. November’s price action based on U.S. Fed’s comments is an example of that. Some of the previously upward-trending markets clearly changed course, like live cattle, with the December contract falling more than 7% in the last two months. Others, like orange juice, made new intra-month highs before closing the month down 4%.

Fixed Income

Overview

Bond prices have been pummeled so severely during the last few years that the word rally seems premature, but certainly these markets have emerged from lows for the time being. The natural result is that TFPN’s enduring short stance is softening a bit, with a substantial reduction as we race toward the end of the year.

Shorts in fixed income remain the largest single portfolio segment. Notable holdings, like the Euribor, remaining near lows. However, as trends build in an upward direction, this will continue to change.

At some point, uptrends in bonds may be a great trade, but patience is warranted until the direction becomes more apparent.

Drivers

The key for bond trends will be whether the consensus that central banks are done raising rates is correct. The next question is when rate cuts will begin. If the market prematurely discounts on a cut, then prices could fluctuate dramatically. However, if policymakers confirm the suspicions of investors, we could see a wave of long trades taking the portfolio exposure to a place it hasn’t been since the ETF’s launch.

Equities

Overview

Perhaps not surprisingly, November’s equity rally was enough to take TFPN’s portfolio from net short to net long as the month closed. The changes leave the portfolio still hedged, but positioned to take advantage of a continuation of the uptrend.

The ETF’s most notable long equity position continues to be elf Beauty, which produced a 27.5% return in November. Other longs like, AZZ Inc and Boise Cascade, also performed well, returning more than 4% and 16%, respectively.

In our view, November’s equity exposure, driven by single stocks, set TFPN apart from similar funds over the course of the month.

Drivers

As time goes on, it seems like the holidays come earlier and earlier in the U.S. It’s possible that was the case in the markets for 2023 as well. What is normally considered a Santa Claus rally might have come in the form of a Thanksgiving rally this year. We expect the portfolio to shift in favor of these trends should they occur, but we require proof before making a change. The easiest way to miss out on “the meat” of market moves is to react prematurely. We have seen this lesson play out many times during our decades of investing experience, but TFPN uses a process that will continue to play the long game, which we feel is best for financial advisors and their clients.

Let's Talk

If you’d like to learn more about TFPN, a next-generation liquid alternative