August 19, 2024

August 2024 Commentary Blueprint Chesapeake Multi-Asset Trend ETF

Home » Strategies » Exchange Traded Funds » Blueprint Chesapeake Multi-Asset Trend » TFPN Commentary

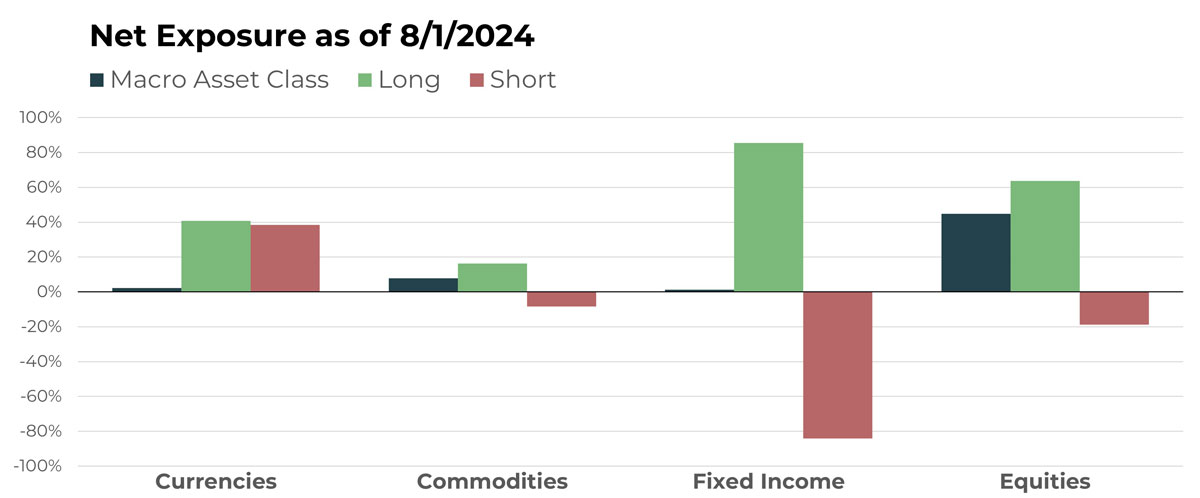

Portfolio Exposure At A Glance

Notable Holdings By Macro Asset Class

| CURRENCIES | |

|---|---|

| Name | Long/Short |

| Swiss Franc/Swedish Kronor | Long |

| iShares Bitcoin Trust ETF | Long |

| British Pound/Swedish Kronor | Long |

| Singapore Dollar/Chinese Yuan | Long |

| Brazilian Real/U.S. Dollar | Short |

| COMMODITIES | |

|---|---|

| Name | Long/Short |

| Copper Future | Long |

| Lead Future | Short |

| Gold Future | Long |

| Cotton Future | Short |

| Cocoa Future | Long |

| FIXED INCOME | |

|---|---|

| Name | Long/Short |

| SPDR Bloomberg High Yield Bond ETF | Long |

| Vanguard Short-Term Corporate Bond ETF | Long |

| U.S. 2-Year Note Future | Short |

| iShares National Muni Bond ETF | Long |

| Japan 10-Year Bond Future | Short |

| EQUITIES | |

|---|---|

| Name | Long/Short |

| Valmont Industries, Inc. | Long |

| Cisco Systems Inc | Short |

| UFP Technologies Inc | Long |

| Comcast Corp | Short |

| Saputo Inc | Long |

ETF holdings and macro asset class allocations are subject to change.

Currencies

Overview

Currency trends in the portfolio remain muted. As a result, exposure continues to be limited both on an absolute and net basis.

Among notable positions in this segment, the Swedish Krona features prominently as the weaker holding in two different currency pairs: versus the Swiss Franc as well as the British Pound. Two other positions that have continued profitable trends are the Singapore Dollar versus the Chinese Yuan (long) and the Brazilian Real versus the U.S. Dollar (short).

Drivers

After failing to generate much in the way of headlines in recent months, currencies started taking center stage in the opening days of August. The so-called Yen carry trade, whereby Yen denominated assets are sold for stronger assets denominated in other currencies, has unwound sharply and resulted in a break from the multi-year downtrend in the Yen. Believe it or not, the long-term downtrend remains intact but has generated significant short-term volatility for those participating in this trend.

The U.S. Dollar also dropped on the prospect of the Fed acting quicker in cutting interest rates. No details have emerged to substantiate that this will occur, but the markets have begun to price in that possibility.

The next few weeks and months could generate substantial activity in the currency segment of the portfolio as sentiment converts to reality.

Commodities

Overview

Commodity exposure in the portfolio has evolved since last month, going from materially net short to net long as of early August. Many of the same notable long positions remain, such as copper, gold, and cocoa. However, there are fewer impactful short positions. One of those notable shorts is cotton, which continues to trend lower. It fell 2.6% in July (October futures contract) and began August on pace for its fifth consecutive monthly decline.

Drivers

We often talk about how markets are a discounting machine. This means that participants (i.e., investors) are constantly discarding old data and consuming new information in the hopes of anticipating the next move in asset prices. The current swing in exposure from net short to net long appears to reflect this principle. Higher interest rates attempted to put a damper on commodity prices, resulting in the previous short exposure. The rapid increase in sentiment toward cuts has likely played a role in reducing short positions, reinforcing existing longs, or creating new longs – all of which push the net allocation long.

Fixed Income

Overview

The largest exposure change at the asset class level heading into August will be on the fixed income front. In a span of two months, the portfolio has gone from net short to net long by a material margin. In fact, net long bonds will now be the second largest allocation behind equities. Within this asset class, high yield, short-term corporate and municipal bonds are the most notable long allocations.

Drivers

With apologies to the CrowdStrike glitch and the reversal in AI stocks, the most dominant single factor driving the markets, in our opinion, is the fixation on the Fed. Of course, nowhere is this impact felt more strongly than assets directly linked to interest rates. While generally always the most important driver to portfolio decisions in this segment, the path and velocity of price adjustments from interest rate changes is most volatile at inflection points, such as we are now.

Equities

Overview

While still the most significant allocation in the portfolio, net long exposure to equities has been decreasing. Shorts in lagging positions, such as Cisco System and Comcast, are acting as hedges against long positions in positive-trending issues, such as Valmont Industries and UFP Technologies. While stocks declined early in August, many of the long- and intermediate-term major index trends remain intact.

Drivers

While including equities as a component of TFPN can increase the portfolio’s correlation to a traditional portfolio slightly, all else equal, it also can provide an enormous arena for taking advantage of outlier trends. We believe a large measure of the correlation can be removed by TFPN’s willingness and ability to use short positions, and using shorts provides another avenue for capturing trends. The recent reversals bring to light the cost of including equities but do nothing to eliminate the long-term benefits, in our opinion. Our timeframes remain longer in duration, which we believe matches best with the goals of financial advisors and their clients.

Portfolio Managers’ Note

For the vast majority of active, long-term-oriented investment strategies, inflection points are not fun. Unless you are specifically seeking out these types of swings, which we believe is extremely difficult to do consistently, they mean a change from a period of relative stability and persistence to uncertainty. For trend followers, inflection points don’t always mean discomfort, but they certainly can. Early August is an example of that.

The question we often ask ourselves during moments where the portfolio value declines is, “What part of our strategy would we eliminate in an attempt to also remove these moments of decline?” When we run through the list of obvious follow up questions, we arrive at a consistent answer:

- Would we eliminate thoughtful position sizing that limits our loss? No.

- Would we eliminate predefined exit points? No.

- What about the ability to indefinitely profit from positive trends? No, not that either.

The conclusion is that we wouldn’t change a thing as we cannot determine a better long-term strategy for handling uncertainty than one that is completely adaptable. Like life, in investing there are tradeoffs. There will be costs to any strategy chosen, so if one can identify which costs they are willing to bear in favor of which benefits to maximize, then the focus should become systematizing rules to exploit those relationships consistently over long periods of time.

Looking ahead, there are plenty of catalysts for both continued trends and continued volatility. Though probably unnecessary to name any, just a few include: monetary policy, an impending election, and a potentially broadening military conflict in both the Middle East and Eastern Europe. Based on the years of trend-following experience among the Portfolio Management Team for TFPN, we are as excited as ever for what lies ahead.

Let's Talk

If you’d like to learn more about TFPN, a next-generation liquid alternative