August 14, 2023

August 2023 Commentary Blueprint Chesapeake Multi-Asset Trend ETF

Home » Strategies » Exchange Traded Funds » Blueprint Chesapeake Multi-Asset Trend » TFPN Commentary

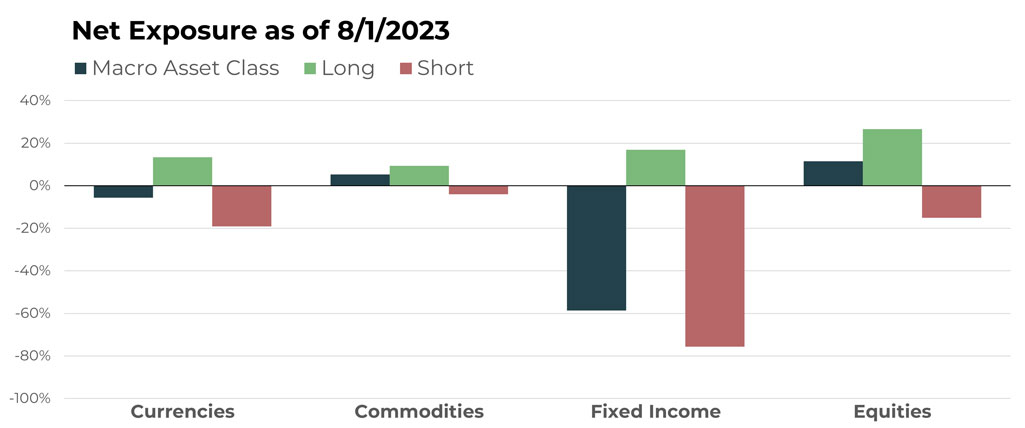

Portfolio Exposure At A Glance

Notable Holdings By Macro Asset Class

| CURRENCIES | |

|---|---|

| Name | Long/Short |

| Euro/British Pound Future | Short |

| Euro/Swiss Franc Future | Short |

| British Pound/Swiss Franc Future | Long |

| U.S. Dollar/Chinese Yuan Future | Long |

| U.S. Dollar Future | Long |

| COMMODITIES | |

|---|---|

| Name | Long/Short |

| Cattle Feeder Future | Long |

| Live Cattle Future | Long |

| Cocoa Future | Long |

| London Cocoa Future | Long |

| White Sugar Future | Long |

| FIXED INCOME | |

|---|---|

| Name | Long/Short |

| 3-Month Euribor Future | Short |

| Canadian Banker’s Acceptance Future | Short |

| 3-Month SONIA Future | Short |

| 3-Month Secured Overnight Financing Rate Future | Short |

| 90-Day Australian Bank Bill Future | Short |

| EQUITIES | |

|---|---|

| Name | Long/Short |

| elf Beauty Inc | Long |

| Hormel Foods Corp | Short |

| General Dynamics Corp | Short |

| World Wrestling Entertainment, Inc. | Short |

| Keurig Dr Pepper Inc | Short |

ETF holdings and macro asset class allocations are subject to change.

Currencies

Overview

TFPN has several outright long positions in major currencies, such as the British Pound, Swiss Franc, and Canadian Dollar. The portfolio is short the Japanese Yen. The largest cross rate positions included long USD/CNH (short Chinese Yuan versus US Dollar) and GBP/Sfr (short Swiss Franc versus British Pound). The largest short cross-rate positions were in Euro/CHF (long Swiss Franc versus Euro) and Euro/GBP (long British Pound versus Euro).

Drivers

Currencies have been largely impacted by interest rates. As expected, the anticipation of peak rates has contributed to continued weakness in the U.S. Dollar and profitable trends, such as being long the Canadian Dollar, British Pound, and Mexican Peso.

Commodities

Overview

Long positions – including sugar, cocoa, and cattle – were offset somewhat by reversals for shorts in grains – such as wheat, soybeans, and sunflower seeds.

Drivers

Many commodity markets witnessed a sharp reversal in July that negatively impacted short positions in soybeans and wheat, among others. The reversal was impacted by consumer reports remaining strong, as well as Russia abruptly exiting the grain deal that had been in place to ensure adequate supply to the world’s inventory.

Fortunately for TFPN, the reversal was offset by sustained uptrends in sugar, cocoa, and cattle.

Reversals are painful, but our risk management techniques are designed to trim or cut these positions at a manageable level while patiently staying on the winning side of the overall commodity trade.

Fixed Income

Overview

The ETF ended the month with short fixed income (long rates) as its largest exposure, both in the U.S. and abroad. The largest short positions included several on the short end of the yield curve via the 3-month Euribor, SONIA, and SOFR. The largest long positions were in Japanese 10-year government and short-term municipal bonds.

Drivers

Any update on the state of trends in the global markets should begin with what is arguably the most influential one right now: interest rates and their impact on fixed income prices.

TFPN’s most significant allocation has been and continues to be short positions in fixed income (long rates). In our opinion, the data indicates one of the best ways to benefit from inflation is to have the ability to short the asset most directly tied to it. While many liquid ETFs and mutual funds are limited in their ability to do this, TFPN is not because it is able to trade as many as 500 securities and financial instruments, including a global portfolio of bond markets, both up and down the yield curve.

Wall Street pundits have been forecasting an end to the rate-hiking cycle, with equities standing to benefit. However, the recent gross domestic product results in the U.S. indicate we may not be as close to the end of the cycle as previously believed, despite continued progress toward the Federal Reserve’s inflation target.

As a result, the trend of being long rates may have more time on the books. The next few months will be critical to determining that, but for now we remain positioned to benefit accordingly.

Equities

Overview

TFPN is long equities. A broad basket of longs were combined with shorts in larger, value-oriented names.

Drivers

The growth/value reversal from 2022 to 2023 has created a profitable trade of being long growth-oriented U.S. equities and short value equities. As the rally has broadened, TFPN’s net long exposure has increased, and the spread trade has decreased as the benefits of the spread have narrowed. Our trend-following systems will continue to drift toward the long side of the trade if equity trends continue as they have since the end of Q1 and early Q2.

Portfolio Managers’ Note

While new as an ETF, the systematic investing strategy powering TFPN has been consistently traded since 1994 and offered by Portfolio Manager Jerry Parker’s firm, Chesapeake, as a private fund and separately managed account. Of course, the origins of trend following as an investing philosophy dates back even further than that.

We believe launching an ETF that can trade as many as 500 securities, futures, and forward contracts — both long and short — represents a positive evolution for investors who seek more diversified and efficient portfolio options. We are humbled and excited for the opportunity to expand the accessibility of our trend-following discipline through an ETF vehicle.

We regard every investor as our partners. With that in mind, our intention is to communicate with you early and often, as well as in a direct and transparent manner.

As always, we remain obsessively focused on doing the things that many investors and asset managers find difficult: executing our systematic investing process with absolute discipline. Our ultimate goal is to use trend following to hunt for outliers.

Summing It Up

TFPN’s vast exposures, both in terms of possible assets (currencies, commodities, fixed income, and equities) and expression (long and short), creates a return profile that we believe is reliably non-correlated to traditional assets. In our opinion, this makes TFPN a valuable alternative allocation, as valuations continue to increase in U.S. equities. At these levels, a downside outlier event could have investors set for a rude awakening. But rather than fear outliers, our trend-following systems actively search them out in an attempt to exploit them, while managing risk tightly should the situation reverse.

Of course, we also believe that the ideal standalone or core investment should also have these important characteristics.

For either use case, we believe TFPN is positioned well for the current state. Most importantly, it is adaptive enough to be ready for what lies ahead.

Let's Talk

If you’d like to learn more about TFPN, a next-generation liquid alternative