April 13, 2025

April 2025 Commentary Blueprint Chesapeake Multi-Asset Trend ETF

Home » Strategies » Exchange Traded Funds » Blueprint Chesapeake Multi-Asset Trend » TFPN Commentary

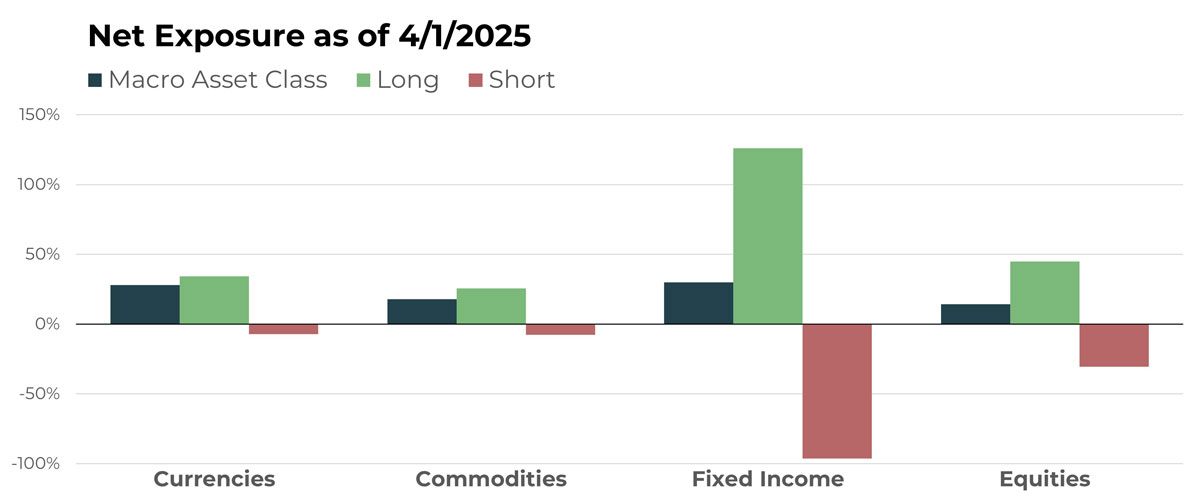

Portfolio Exposure At A Glance

Notable Holdings By Macro Asset Class

| CURRENCIES | |

|---|---|

| Name | Long/Short |

| Aussie Kiwi/New Zealand Dollar | Long |

| Chinese Yuan/Canadian Dollar | Long |

| Chinese Yuan/Singapore Dollar | Long |

| Canadian Dollar/U.S. Dollar | Short |

| Colombian Peso/U.S. Dollar | Short |

| COMMODITIES | |

|---|---|

| Name | Long/Short |

| Corn Future | Long |

| Rough Rice Future | Short |

| Cattle Future | Long |

| Silver Future | Long |

| Lead Future | Short |

| FIXED INCOME | |

|---|---|

| Name | Long/Short |

| Aussie 10-Year | Short |

| iShares Short-Term National Muni Bond ETF | Long |

| U.S. 10-Year Note | Short |

| iShares 0-5 Year TIPS Bond ETF | Long |

| U.S. 30-Year Note | Short |

| EQUITIES | |

|---|---|

| Name | Long/Short |

| L'Air Liquide S.A. | Long |

| Thermo Fisher Scientific | Short |

| Pepsico Inc | Short |

| Volatility Index Future | Long |

| Mccormick & Co Inc | Long |

ETF holdings and macro asset class allocations are subject to change.

Currencies

Overview

Exposure to non-U.S.-Dollar denominated currencies have flipped from net short to net long. Currencies will continue to represent the second-most-significant allocation, after fixed income, from an overall asset perspective.

Drivers

The change in direction is due to weakness in the U.S. Dollar and represents the first major trend change driven by uncertainty due to U.S. tariff policy. With renewed weakness in early April, the U.S. Dollar is in decline, giving back nearly all of its post-COVID-19 gains. In terms of direct plays on the U.S. Dollar, the ratio of longs to shorts is down to around 5:1, having favored long exposure near 10:1 about a month ago.

Commodities

Overview

The commodity sector of the portfolio remains net long at almost the same rate as in March. Food and fiber products repeat as notably large allocations. Livestock products again follows as the next-largest segment and remains unanimously long. Metals, led by gold, are closely behind livestock futures, with energy also being slightly long. Grains have flipped to net short.

Drivers

Over half the net long exposure to food products continues to be driven by cocoa futures. In fact, the allocation to cocoa is greater than the net allocation to energy, metals, and grains; it is almost as large as livestock by itself. Coffee also continues to represent a significant holding. Perhaps the best commodity trend in recent weeks has been gold, which remains a key and growing position.

Fixed Income

Overview

At a high level, the fixed income allocation remains net long. That said, the makeup is nuanced. For example:

- ETF holdings centered on corporates, municipals, and mortgage-backed instruments remain unanimously long

- Short-term interest rates, such as the Euribor and U.K. bonds, remain long but down from the two-to-one ratio of a month ago

- Futures positions making up the U.S. yield curve from the 2-year to the 30-year continue to be predominantly short

Drivers

Sweeping tariff action and signs of a cooling economy have for pushed yields lower and thus prices higher. This is the case across many segments of the fixed income universe but none more so than U.S. Treasuries. With that said, there has been just enough economic data supporting inflation to discourage any consensus about future rate cuts by the Federal Reserve. For now, the picture in fixed income remains muddled, which does little to help establish profitable trends.

Equities

Overview

TFPN’s overall equity allocation is roughly equally balanced among longs and shorts. While shorter- to intermediate-term trends are now moving into negative territory, long-term trends continue to be positive. A weak opening to April after large-scale tariffs has put further pressure on longs.

Drivers

Many of the same major positions we noted in past updates continue to be the most influential. The largest short position, Canadian National Railway, fell another 3.85% in March. A newcomer to the update is Pepsico, which is the second-largest short equity position. It fell 2.30% in March and continues to trade near its lowest level since 2021.

Portfolio Managers’ Note

U.S. Dollar dominance turning to weakness, a bond bear market shifting to a possible flight to safety, stagnating commodities, and a retracement in the U.S. stock market: these are the dynamics that trend-following systems seek to exploit like few other strategies as they become more persistent. However, when these moves are less persistent or lack follow-through, they present more of a wait-and-see environment. Unfortunately, as we enter the second quarter, it is still more of the latter than the former.

Last month we talked about the importance of timeframe selection when it comes to providing noncorrelation to a traditional portfolio of stocks and bonds. For TFPN, our chosen timeframe is on the longer side, meaning we are willing to endure short- to intermediate-term choppiness to exploit longer-lasting trends. The upside is clear when those trends persist, but the downside can be also obvious and painful.

Just like a good boxer or mixed martial arts fighter will often get bloodied from time to time without being knocked out, a good trend follower will take their lumps when markets reset or adjust to a new paradigm without going bust. For a strategy created to be “all weather” in nature, it is self-evident that sometimes the weather will be challenging. After several decades of experience executing trend-based strategies, we have seen plenty of fights and loads of bad weather – this is nothing new.

TFPN’s job is to hunt for outliers and execute the signals. We think judging through the lens of process over outcome shows our approach is as successful as ever. With that said, we realize that periods such as these are not fun. If we seem unaffected by these conditions it is only because experience has cemented our confidence in the power of trend following. We say this without meaning to belittle the anxiety investors can feel. We are grateful for our trend-following tribe’s patience, and we look forward to seeing how trends develop next (as they always seem to do).

Let's Talk

If you’d like to learn more about TFPN, a next-generation liquid alternative