May 19, 2025

May 2025 Commentary Blueprint Chesapeake Multi-Asset Trend ETF

Home » Strategies » Exchange Traded Funds » Blueprint Chesapeake Multi-Asset Trend » TFPN Commentary

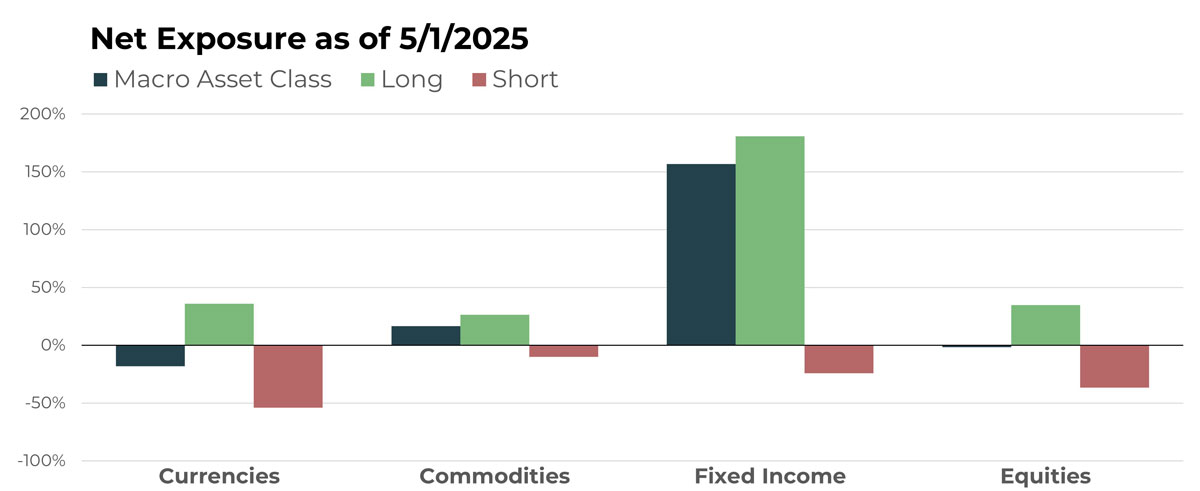

Portfolio Exposure At A Glance

Notable Holdings By Macro Asset Class

| CURRENCIES | |

|---|---|

| Name | Long/Short |

| iShares Bitcoin Trust ETF | Long |

| Euro/Australian Dollar | Long |

| Euro/Chinese Yuan Long | Long |

| Canadian Dollar/U.S. Dollar | Short |

| U.S. Dollar/South African Rand | Short |

| COMMODITIES | |

|---|---|

| Name | Long/Short |

| Cocoa Future | Long |

| Rough Rice Future | Short |

| Cattle Future | Long |

| Gold Future | Long |

| Cotton Future | Short |

| FIXED INCOME | |

|---|---|

| Name | Long/Short |

| Japan 10-Year Bond | Short |

| Invesco Senior Loan ETF | Long |

| U.S. 3-Year Note | Long |

| iShares 0-5 Year TIPS Bond ETF | Long |

| U.S. Long Bond | Short |

| EQUITIES | |

|---|---|

| Name | Long/Short |

| Agnico Eagle Mines Ltd | Long |

| Constellation Brands Inc | Short |

| Pepsico Inc | Short |

| AZZ Inc | Long |

| TKO Group Holdings Inc | Long |

ETF holdings and macro asset class allocations are subject to change.

Currencies

Overview

The U.S. Dollar continues to weaken, leading to a shift in the portfolio’s currency exposures. Where TFPN was once heavily tilted toward long U.S. Dollar positions, it’s now modestly skewed in favor of foreign currencies. While not a full reversal, the pace of this transition has been notable.

Within cross-currency trends, European currencies are showing more strength relative to their Asian counterparts — a dynamic that’s consistent with regional equity trends as well.

Drivers

Tariff uncertainty and the risk of stagflation remain central macro drivers. On the short side versus the U.S. Dollar, the most prominent positions are in the Canadian Dollar, Chinese Yuan, and Indonesian Rupiah. The Indian Rupee stands out on the long side, showing the strongest positive trend relative to the U.S. Dollar. Among cross-rate positions, the short Euro/long Czech Koruna exposure is currently one of the most influential in the portfolio.

Commodities

Overview

For the third straight month, the portfolio’s commodity exposure remains largely unchanged and net long. Livestock has nearly matched food and fiber as the most significant subsector. Meanwhile, despite strength in gold, metals have joined grains in shifting to net short exposure. Energy markets continue to exhibit muted trends and remain a minor part of the portfolio.

Drivers

Cocoa. Coffee. Cattle. The “three Cs” have been staples of the portfolio’s long commodity exposure for much of TFPN’s life — and they remain the largest allocations. Each moved higher in April, with cocoa leading the pack at +15%. Gold also contributed meaningfully, rising another 5% and holding its place as a notable allocation despite the broader metals complex turning negative.

Fixed Income

Overview

The most notable shift in the portfolio from April to May is a further increase in net long exposure to fixed income. Already the largest asset class allocation, it has grown further due to intermediate-term government bonds strengthening and joining short-term bonds in trending higher. Long-duration instruments — such as 30-year U.S. Treasuries — remain the lone holdouts on the short side.

Drivers

Softening economic forecasts and weaker earnings expectations have accelerated the shift toward safety, pushing bond prices higher. While shorter-term Treasuries have shown consistent strength in recent months, it’s the recent momentum in intermediate-term bonds that has reinforced the broader risk-off tone. Interestingly, longer-duration bonds remain under pressure despite the strength elsewhere in fixed income — an atypical divergence that could signal markets are positioning for a rebound in risk assets once uncertainty clears. From a trend-following perspective, the portfolio’s defensive posture remains intact and may prove valuable if equities revisit or undercut the early-April lows.

Equities

Overview

TFPN’s equity exposure is nearly balanced, with long positions slightly outweighing shorts. While equity exposure has been gradually reduced since early 2025, that pace accelerated in April. If recent weakness continues, the portfolio is positioned to pivot quickly, with short exposure likely to overtake longs in the near term.

Drivers

Despite broad risk-off sentiment, Strategy Inc (formerly MicroStrategy) posted a 32% gain in April and maintained its spot as TFPN’s largest equity holding. Other notable long exposures include AZZ Inc, TKO Group Holdings, and Carpenter Technology. On the short side, the largest positions remain consistent, with Canadian National Railway and Pepsico among the most significant. As always, trend signals — not predictions — guide these allocations, allowing the portfolio to adapt as market conditions evolve.

Portfolio Managers’ Note

There are several bright spots across the portfolio — many of which are highlighted in the asset class overviews above. Still, April was a reminder that even a disciplined process can experience periods where trends are too few or too fleeting to drive positive performance. While our strategy doesn’t require all — or even most — markets to trend, it does need SOME sustained directional movement, and April didn’t deliver enough of it.

As we noted last month, these stretches are not only expected, they’re essential to how noncorrelated strategies behave. To truly benefit from diversification, one must accept that performance won’t always sync with conventional benchmarks. A focus on process over outcome is only meaningful if it holds through periods of discomfort. Nobody second-guesses too much when the outcome is positive — it’s how we respond to setbacks that reveals our conviction.

Not all trend following is a lifestyle choice, but the level of commitment reflected in TFPN certainly is. It’s like choosing to get healthy: at first it can feel foreign, even laughable. But over time, small steps add up. What starts as an experiment becomes second nature, and eventually anything else feels unnatural. That’s how we’ve come to view systematic investing. Trendless periods don’t shake us — they just reinforce how unthinkable it would be to approach markets any other way.

That said, we recognize this level of conviction isn’t universal. That’s why we encourage financial advisors to size trend following in a way their clients can stick with. For some, that means a meaningful allocation; for others, a smaller slice. The beauty of the discipline is that it scales. The long-term benefits will always reflect the level of commitment — but even a little is better than none, in our view.

Just when you think it won’t get better is often when it does. We can’t promise when that will be, but we can promise we’ll be ready. That’s been true in every prior trendless stretch — and when trends have returned, they’ve often done so with force.

Let's Talk

If you’d like to learn more about TFPN, a next-generation liquid alternative