November 15, 2024

November 2024 Commentary Blueprint Chesapeake Multi-Asset Trend ETF

Home » Strategies » Exchange Traded Funds » Blueprint Chesapeake Multi-Asset Trend » TFPN Commentary

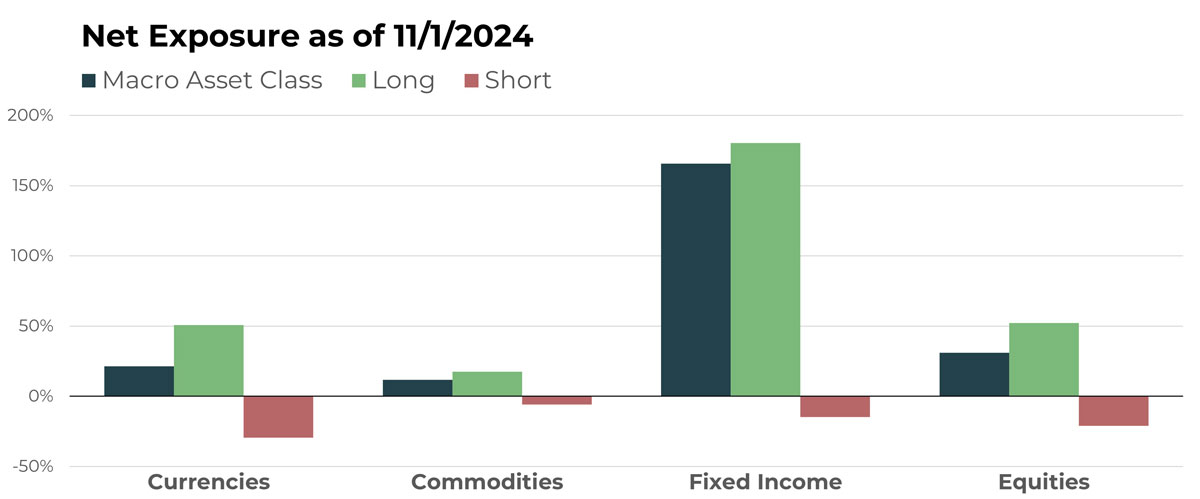

Portfolio Exposure At A Glance

Notable Holdings By Macro Asset Class

| CURRENCIES | |

|---|---|

| Name | Long/Short |

| Euro/Australian Dollar | Short |

| Indonesian Rupiah/U.S. Dollar | Long |

| Swiss Franc/Japanese Yen | Long |

| Chinese Yuan/U.S. Dollar | Long |

| iShares Ethereum Trust | Long |

| COMMODITIES | |

|---|---|

| Name | Long/Short |

| Silver Future | Long |

| Lumber Future | Short |

| Copper Future | Long |

| Lead Future | Short |

| Rubber Future | Long |

| FIXED INCOME | |

|---|---|

| Name | Long/Short |

| U.S. 2 Year Note Future | Short |

| SPDR Bloomberg Convertible Securities ETF | Long |

| U.S. 10-Year Note Future | Long |

| Vanguard Short-Term Corp Bond ETF | Long |

| Japan 10-Year Bond Future | Long |

| EQUITIES | |

|---|---|

| Name | Long/Short |

| Owens Corning | Long |

| Hess Corp | Short |

| Energizer Holdings Inc | Long |

| Nestle SA | Short |

| Lululemon Athletica Inc. | Short |

ETF holdings and macro asset class allocations are subject to change.

Currencies

Overview

Trends within TFPN’s currency portfolio remain muted, with many burgeoning movements but few standouts. The most noteworthy positions that have been additive to the portfolio are in the crypto currency space, such as the iShares Bitcoin Trust. The U.S. Dollar is generally strengthening, with a few Pacific-Asian currencies weakening versus it, including the Chinese Yuan and Indonesian Rupiah.

Drivers

The decisive U.S. election has paved the way for a rally in riskier assets, supporting returns in crypto and reducing legislative risk, as investors anticipate more stable policies. Strong economic data and the Republican Party’s “America First” policies have also contributed to a rally in the U.S. Dollar through October and into November. Despite the U.S. Dollar’s strength and favorable economic indicators, the Federal Reserve proceeded with a cautious 0.25% rate cut, balancing concerns about potential economic slowing with signs of resilience.

Commodities

Overview

After moving into the second spot as the most influential sector of TFPN’s portfolio during October, commodities will again take a backseat to equities, currencies, and fixed income. The metal complex (e.g., silver and copper, to name a couple) remains a notable long allocation, as well as agricultural commodities, such as live cattle and corn. Overall, the portfolio is mostly hedged with a slight tilt toward rising global trends.

Drivers

After September’s 0.50% rate cut shocked some commodities into uptrends, subsequent economic reports showing the economy’s strength have dampened the party a bit, as skepticism has returned about the Fed’s ability to keep it up. With another, smaller cut in early November, the environment remains conducive to positive trends in the space. However, uncertainty about the impacts of government policies with the new presidential administration could keep the substantive breakouts on hold until 2025.

Fixed Income

Overview

Fixed income remains the most significant allocation in the portfolio. While long positions were reduced during October, TFPN remains net long global fixed income. Bond positions with historically higher correlation to equities are now taking up a larger portion of this segment. For example, two notable securities are the SPDR Bloomberg Convertible Securities ETF and the Vanguard Short-Term Corp Bond ETF, both of which tend to move more in line with stocks than their Treasury counterparts.

Drivers

Cumulative interest rate reductions by the Fed of 0.75% during the last few months have provided the foundation for a rally in bond prices. However, uncertainty about how the economy’s strength will impact inflation has caused longer-duration bonds to retrace from the peak of the recent rally. Coincidentally, the same data that has dampened the run in longer-duration bonds has boosted corporate fixed income. The portfolio has pivoted accordingly, enabling TFPN to offset, to some degree, the retracements in sovereign bonds.

Equities

Overview

As mentioned above, after taking a backseat to both bonds and commodities in October, equities increased in November, providing the ability for it to benefit from the decisive U.S. election and continued favorable economic environment. Long positions in the mid-cap space, such as Pilgrims Pride and BWX Technologies, helped lead the sector in October. Short equity positions remain an important feature of the portfolio, reducing TFPN’s overall risk by providing valuable hedging characteristics. For example, Nestle SA and Lululemon should generally benefit from a stronger, low volatility environment for equities but remain entrenched in long-term downtrends.

Drivers

While interest rates have increased over the last few years, most individuals and businesses remain locked in very low interest rate arrangements from before rates increased. As a result, the increase in rates has done little to impact their financial condition but have done just enough to decrease the rate of inflation, providing a kind of “Goldilocks scenario.” Equities have benefited accordingly and figure to continue to do so for the time being, which is positive for how the portfolio is positioned based on current trends.

Portfolio Managers’ Note

Diversification is often seen as a cornerstone of prudent investing. Many of us were first introduced to the art of investing through the classic advice of “not putting all your eggs in one basket,” emphasizing how asset performance can fluctuate year to year. Yet, for those who practice diversification, there’s a unique conundrum we like to call the diversifier’s dilemma.

So, what exactly is this diversifier’s dilemma? In our experience, the average investor’s perception of fund performance is heavily influenced by how the stock market – and particularly a few big names – performs. As asset managers, we are often evaluated against stock indexes, regardless of our actual strategy focus. This can lead to a year being judged as a failure if it doesn’t align with the stock market’s performance, even if our strategy aims to provide returns through other avenues. In years like 2024, when equities have largely outperformed, the mixed returns in currencies, commodities, and fixed income often go unnoticed by the typical investor.

Conversely, when stocks perform poorly, the expectation shifts, and asset managers are judged on capital preservation – something that’s increasingly difficult to achieve without true diversification. A manager aiming for absolute return, independent of stock market swings, can feel damned if they do and damned if they don’t, particularly over shorter timeframes.

This brings us to a crucial consideration: goals. Our focus is on aligning our strategy with financial advisors who are committed to helping their clients reach their financial goals rather than chase benchmarks or stock-linked returns. Arguably, the most valuable skill an advisor brings is guiding investors within a structured plan. In this context, the benefits of diversification and non-correlation become clear and impactful. This is why we value advisors so highly: without their partnership, much of our approach could be misunderstood or overlooked, but with their guidance, the path to achieving meaningful outcomes opens up.

Let's Talk

If you’d like to learn more about TFPN, a next-generation liquid alternative